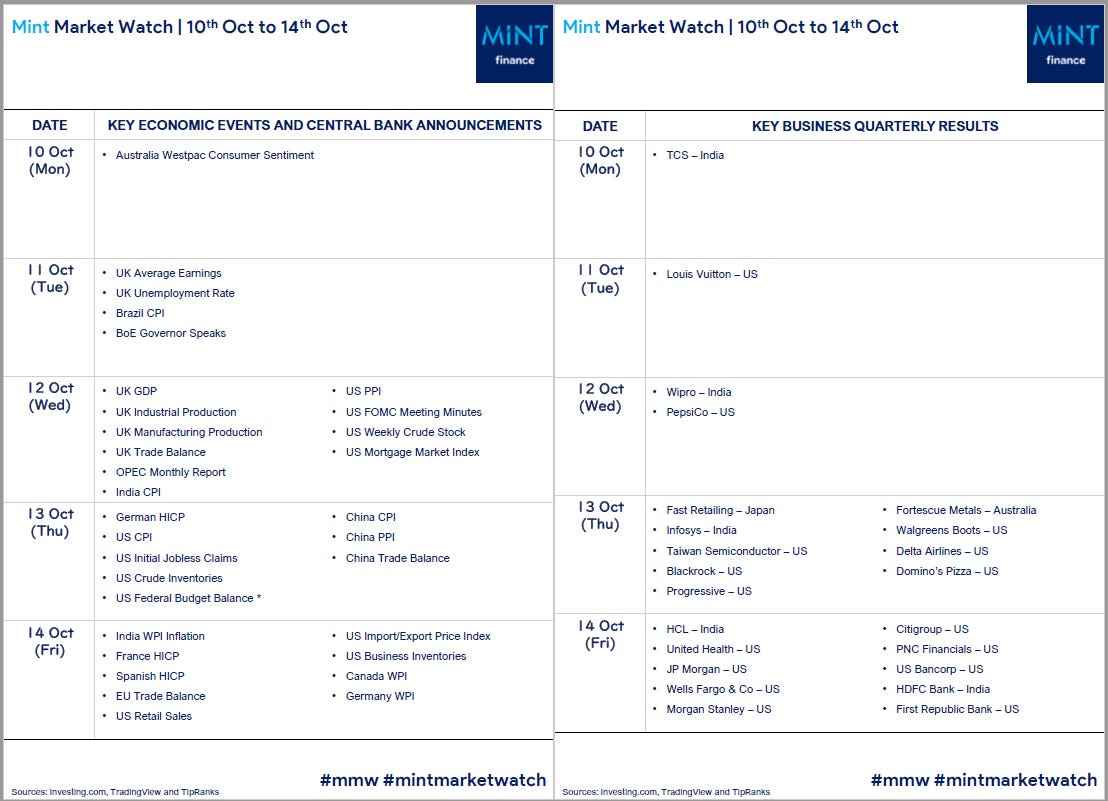

Mint Market Watch | 10/Oct to 14/Oct

Mint Market Watch | 10/Oct to 14/Oct

Quarterly earnings season kicks off with major bank earnings; CPI numbers from major economies incl. US, China and India; US FOMC Meeting Minutes to be published this week.

10th Oct 22 (Monday)

The Week Ahead in Markets. Second half this week will mark the commencement of the earnings season.

Top financial services giants including JP Morgan, Citi, Morgan Stanley, PNC Financials, Blackrock and HDFC Bank, will kick start quarterly announcements.

Among other key firms, PepsiCo, Wipro, TCS, TSMC, Louis Vuitton and Fortescue Metals Group announce results.

Meanwhile in economic announcements, US inflation is expected to climb still but a slightly slower pace in September relative to August. Reuters poll respondents expect the headline US CPI to come in at 8.1% in Sep YoY.

CPI data will be published a day after the rollout of minutes from the Federal Reserve’s September meeting. CPI data plus FOMC minutes will likely guide market expectations for the Fed’s meeting in November.

Presently, futures markets are pricing in a fourth consecutive 75 bps interest rate rise in Nov.

Across the Atlantic, UK economy is expected to have contracted slightly in August due in part to soaring prices hitting household demand and business activity. The government has frozen households’ energy bills and slashed taxes to boost growth. Some economists expect a deep recession in the UK as the “mini” Budget resulted in surging interest rate expectations.

TOP TEN ECONOMIC EVENTS THIS WEEK

US CPI

Germany HICP

China CPI

UK Average Earnings

UK Unemployment Rate

UK GDP

US FOMC Meeting Minutes

US Initial Jobless Claims

US Retail Sales

US Crude Inventories

TOP TEN EARNINGS RESULTS THIS WEEK

JP Morgan (Thursday)

Citi (Friday)

Fortescue Metals Group (Thursday)

Taiwan Semiconductors (Thursday)

Blackrock (Thursday)

PepsiCo (Wednesday)

Louis Vuitton (Tuesday)

Fast Retailing (Thursday)

United Health (Friday)

Wells Fargo (Friday)

11th Oct 22 (Tuesday)

BoE doubles bond buying to £10B/day; TCS books record profits of >INR 10K crores (USD 1.2B); Oil prices tank >2% on rising demand concerns.

Fears of gloomy earnings season took stocks down. Semiconductor index tanked 4% following new export controls.

BoE stepped up intervention in the bond market increasing emergency bond-buying operations from £5B to £10B a day from Tue until EOW.

TCS reported revenue of Rs. 55.3K Cr (55k Cr. E) clocking an 18% YoY. Net profit increased >8% YoY to Rs. 10.4K Cr. N.America led with >17% growth; Europe grew >14%, UK grew 14.8%, India grew 16.7% and Latin America up 19%.

Australian consumer sentiment drops 0.9% in Oct and analysts at Westpac noted that it could have been worse if RBA had hiked rates by 50 bps instead of 25 bps.

Brent fell $2.30, or 2.4%, to $93.89/barrel. U.S. WTI crude shed $2.12, or 2.3%, to $89.01. This comes after a 2% decline on Monday.

Australian consumer sentiment drops 0.9% in October

Westpac reported that Australian consumer sentiment worsened in early October, dropping 0.9% from 84.4 in September to 83.7. The index is trending at lows seen at the beginning of the pandemic and during the 2008 financial crisis.

Westpac noted that the reading would likely have been worse if the RBA had hiked interest rates by 50bps instead of the 25bps they went with. Rising interest rates have been a key concern of Australian consumers this year, given their adverse effect on the mortgage and housing market. (Investing)

TCS profits rise 8.38% crossing Rs. 10,000 Cr for the first time

TCS reported revenue of Rs. 55,309 Cr (55,000 Cr. expected). Representing a 18% YoY increase. Net profit increased 8.38% YoY to Rs. 10,431 Cr. PAT crossed the 10,000 Cr. mark for the first time. However, the company’s operating margin contracted 1.6% YoY to 24%. In constant currency terms, revenue grew 15.4% YoY. The growth has broad-based across verticals, led by retail and CMI segments. TCS's order book stood at $8.1 billion.

Among major markets, North America led with 17.6% growth; Continental Europe grew 14.1% and the UK grew 14.8%. In emerging markets, India grew 16.7%, Latin America grew 19.0%, Middle East & Africa grew 8.2% and the Asia Pacific grew 7.0%.

TCS added 9,840 employees during the quarter. The attrition rate in IT services was 21.5% on the last twelve months basis.

TCS has fixed October 18 as the record date and November 7 as the payment date for the second interim dividend of Rs 8 per share. (Economic Times)

BoE steps up intervention in Bond market with low investor interest.

The Bank of England stepped up intervention in the UK bond market as they announced that they would increase emergency bond-buying operations from £5B to £10B per day from Tuesday till the end of the week to bring the scheme to a smooth conclusion.

So far, investors haven’t taken up as much of the support as the BOE has offered. In the eight auctions to date, the BOE bought just £4.6 billion of bonds, about 12% of the £40 billion capacity of the program.

BoE also announced a Temporary Expanded Collateral Repo Facility, or TECRF, that will run beyond the end of this week until Nov. 10. Its purpose is to enable banks to ease pressures in LDI funds through liquidity insurance operations. “Under these operations, the Bank will accept collateral eligible under the Sterling Monetary Framework (SMF), including index linked gilts, and also a wider range of collateral than normally eligible under the SMF, such as corporate bond collateral,” the Bank said.

BoE also stated that it would be ready to use its regular Indexed Long Term Repo operations each Tuesday — which allow market participants to borrow BOE cash reserves for six months in exchange for less liquid assets — to further ease liquidity pressures on LDI funds.

The sharp sell-off in British government bonds after Finance Minister, Kwarteng's "mini-budget" sparked a scramble for cash by Britain's pension funds which had to post emergency collateral in LDIs. In a move aimed at calming investors' nerves, Kwarteng said on Monday he would bring forward his medium-term fiscal plan, including an explanation of how the tax cuts will be paid for, to Oct. 31 from Nov. 23, with independent budget forecasts to be published the same day. (CNBC, Reuters, Yahoo)

Oil price dips after rally last week as demand concerns persist

Brent crude fell $2.30, or 2.4%, to $93.89 a barrel by 1006 GMT. While, U.S. West Texas Intermediate crude dropped $2.12, or 2.3%, to $89.01. This comes after a 2% decline on Monday. The price decline saw last week’s gains on the back of OPEC+ supply cuts retrace almost entirely.

Concerns about the demand for oil persist as IMF director, David Malpass, warned of a growing risk of a global recession. Additionally, a spike in COVID cases in Shanghai raised further concerns of lowered demand in China. (Reuters)

12th Oct 22 (Wed)

HK equities trading at Oct 2011 levels; UK lowest unemployment rates unseen in 48 years; LVMH reports strong earnings pointing to resilience of luxury goods demand.

US equity markets edged higher in choppy trading. Investors are faced with near certain prospect of rates rising with evidence of still-hot economy and labour market. Hong Kong’s Hang Seng closed 2.2% down touching levels last seen in Oct 2011.

The unemployment rate in UK fell to 3.5%, the lowest in 48 years, led by quarter million people leaving workforce.

LVMH sales jump on strong dollar, up 19% YoY. Demand for luxury goods has so far proved resilient from inflationary pressures, with affluent consumers less impacted by a cost-of-living crisis.

Inflation in Brazil eases to 7% but still above BCB’s forecast of 5.8%.

UK Unemployment Rate falls to 3.5% on strong labor market, Average Earnings Index up 5.4% YoY

UK unemployment rate fell from to 3.5% in August. This is the lowest level since 1974. The drop in unemployment rate was led by a record 252k people leaving the labor market in the quarter up to August. These people are now neither in work nor looking for work, with the increase driven by long-term sickness among older workers and young people becoming students. This increased the inactivity rate by 0.6% to 21.7%

Job vacancies fell by 46k in the quarter to 1.246M but remain higher than pre-pandemic levels, while number of people in work declined 109k (155k E). Claimant count increased by 25.5k last month. the number of unemployed people per vacancy fell to 0.9.

Growth in average total pay (including bonuses) showed 6% YoY increase (5.9% E), but still remains far below inflation which was showed 9.9% increase in consumer prices meaning that adjusted for inflation, wages fell 3.9%. Wages excluding bonuses rose by an annual 5.4%. (Reuters, Bloomberg, ONS)

Brazil inflation cools to 7.17% in September

Brazil’s CPI eased to 7.17% YoY in September (7.1% E) from 8.73% in August. On a monthly basis, CPI declined by 0.29% MoM in September (-0.34% E). The drop-off in CPI over the past few months in Brazil was likely the result of steep rate hikes by the BCB which took the benchmark Selic rate up to 13.75%.

Inflation remains above BCB’s forecast of 5.8% for this year, which could be concerning as BCB decided to end their aggressive rate hiking cycle in September. (Investing)

LVMH sales jump on strong dollar, up 19% YoY

LVMH reported sales of 19.1B Euros ($18.6B) for the quarter, up 19% YoY (13% E) at constant currency. Sales in the group's core fashion and leather-goods business climbed 22% on year to EUR9.69 billion, leading growth among LVMH's divisions.

In Europe, the U.S. and Japan, sales performance remained robust thanks to solid demand from local luxury consumers and a recovery in international travel, LVMH said. In Asia, including China, growth picked up in the third quarter after a more sluggish performance previously, as pandemic rules were partially eased, the company said.

Demand for luxury goods has so far proved resilient from inflationary pressures, with affluent consumers less impacted by a cost-of-living crisis. LVMH reaffirmed guidance stating that it was confident of maintaining current growth levels with a policy of cost control and selective investment, even in the face of an uncertain geopolitical and macroeconomic environment. (Reuters, Marketwatch)

BoE Governor Bailey announces deadline for bond repurchases

BoE will cease all gilt purchases after Friday as Governor Bailey urged pension funds to complete rebalancing before the end of the scheme. The Pensions and Lifetime Savings Association (PLSA), stated that they hope that the BoE will extend the deadline till the end of October or implement different measures to manage market volatility. (NASDAQ)

13th Oct 22 (Thursday)

UK GDP declines 0.3% MoM in August, raising recession fears

UK GDP declined 0.3% MoM in August (no change expected). Meanwhile July’s data was revised down to show GDP grew 0.1% instead of 0.2%. The reading represents a 2% YoY GDP growth (2.4% E). This puts the UK economy back at its size just before the pandemic.

"The economy shrank in August with both production and services falling back, and with a small downward revision to July's growth the economy contracted in the last three months as a whole," Grant Fitzner of the ONS said.

"The ongoing squeeze on household finances continues to weigh on growth, and likely to have caused the UK economy to enter a technical recession from the third quarter of this year," Yael Selfin, chief economist at KPMG UK, said.

A reduction in the amount spending by the government related to the pandemic was also one of the big causes of the slump in manufacturing which fell 1.6% MoM from July. Manufacturing was also hit by pharmaceutical companies cutting back production. Overall, Services declined 0.1% as entertainment and recreation took a big hit of 5% which was partially offset by professional services and architecture which gained 1.2%. Consumer facing services declined 1.8%. The construction sector grew 0.4% with new work increasing 1.9%. Mining sector was hit by maintenance in the North Sea which slumped 8.2%. Meanwhile, many other consumer-facing services struggled, with retail, hairdressers and hotels all faring relatively poorly

The IMF downgraded its forecast for the UK economy’s GDP growth for 2023 from 0.5% to 0.3%. (BBC, Reuters, ONS)

UK trade deficit widens by 200M GBP as imports jump 5%

UK trade deficit in goods and services widened by 200M GBP to 25.6B GBP. This number excludes precious metals. Goods trade deficit widened by 0.9B to 61.9B GBP, Services trade surplus widened by 0.7B to 36.3B GBP.

Meanwhile, removing the effect of inflation, the total trade deficit actually narrowed by 6.5B to 11.9B GBP demonstrating that UK trade has been impacted by soaring inflation and a falling pound.

Total imports of goods increased by £3.1 billion (5.7%) in August 2022, because of a rise in imports from non-EU countries which increased 13.3% to 30.2B GBP. Total exports of goods increased by £0.4 billion (1.2%) in August 2022, driven by increases in exports to non-EU countries which increased 4.1% to 16.8B GBP.

Meanwhile imports from the EU declined 1.9% to 26.1B GBP while exports declined 1.5% to 17.8B GBP. (ONS)

OPEC cuts oil demand forecast for 2022 and 2023 as they see economies slowing

OPEC in their monthly report, cut its 2021 forecast for growth to 2.7% or 2.64M bpd which is lower than its previous forecast of 3.1% growth representing a 3.1M bpd increase in demand.

In 2023, OPEC sees oil demand rising by 2.34 million bpd, 360,000 bpd less than previously forecast, to 102.02 million bpd.

"The world economy has entered into a time of heightened uncertainty and rising challenges, amid ongoing high inflation levels, monetary tightening by major central banks, high sovereign debt levels in many regions as well as ongoing supply issues," OPEC said in the report.

The U.S. Energy Department, by contrast, sees demand growing by 1.5% in 2023 to 101.03 million bpd, down from 101.50 million bpd forecast last month. It also only expects a 0.8% increase in production to 100.73 million bpd next year.

Brent crude futures rose 49 cents, or 0.5%, to $92.94 a barrel by 0833 GMT. U.S. West Texas Intermediate crude was up 37 cents, or 0.4%, at $87.64 a barrel. (Reuters, Reuters)

India CPI spikes to 7.41% YoY in September

India’s CPI which shows retail inflation, spiked to 7.41% in September (7.3% E) from 7% in August. This is the highest level in 5 months and shows that inflation may not have peaked yet. This is the ninth consecutive time that the CPI print has come above the Reserve Bank of India’s (RBI) upper margin of 6 per cent. the Fuel and light segment rose 10.39 per cent, clothing and footwear spiked 10.17 per cent and the housing segment inched up 4.57 per cent.

The RBI has hiked interest rates by 1.9% to 5.9% this year in an attempt to control inflation, however, the latest data suggests there is more hiking needed as inflation continues to rise. RBI last hiked rates by 50bps in September.

The Consumer Food Price Index (CFPI) or the inflation in the food basket too showed a month-on-month rise during September to 8.60 per cent, from 7.62 per cent in August. Prices of vegetables rose 18.05 per cent on year in September. Apart from this, the spices saw a rise of 16.88 per cent while that cereals and products gained 11.53 per cent and milk and products rose 7.13 per cent. Egg prices slipped (-)1.79 per cent but fruits grew 5.68 per cent.

India’s factory output, measured through the Index of Industrial Production (IIP), witnessed a contraction of (-)0.8 per cent in August.

The IIP contraction in August was mainly because of manufacturing and mining sectors. The manufacturing sector contracted (-)0.7 per cent on-year to 131.0 in August while the mining sector saw a decline of (-)3.9 per cent to 99.6. The electricity sector was the only one that witnessed a growth of 1.4 per cent to 191.3. (Indian Express)

US PPI increases 0.4% in September but yearly PPI growth slows indicating improving supply chains

US Producer prices increased 0.4% MoM in September (0.2% E) after declining 0.2% in August. Core PPI increased 0.3% while services PPI increased 0.4%. This represents a PPI increase of 8.5% YoY (8.4% E) slowing from 8.6% in August. Core PPI gained 5.6% YoY. Still, underlying goods prices were the lowest in 2 and a half years as supply chains improved and commodity prices eased.

Prices for transportation and warehousing services slipped 0.2%. Goods prices increased 0.4% with a 1.2% increase in Food prices as fresh and dry vegetable prices surged 15.7%. Energy prices rose 0.7%, driven by diesel fuel, residential natural gas and home heating oil. But wholesale gasoline prices fell 2.0%. Hotel and Motel accommodation prices surged 6.4%.

Producers could be struggling to pass on higher prices as the margin received by wholesalers and retailers stayed largely unchanged, increasing slightly. Margins for final demand trade services edged up 0.1%. Prices for intermediate goods and services also increased moderately.

Core goods rose 7.5% in the 12 months through September, slowing from an 8.1% increase in August. MoM, core goods prices remained unchanged in September. (Reuters)

FOMC Minutes show that fed members in agreement over higher, faster, longer rate hikes

Minutes from the September 21-22 FOMC meeting showed many Fed officials "emphasized the cost of taking too little action to bring down inflation likely outweighed the cost of taking too much action.". In discussions leading up to a 0.75 percentage point rate hike, policymakers noted that inflation is especially taking its toll on lower-income Americans. Overall, the members agreed that higher, faster, and longer rate hikes were necessary.

The monetary policy committee agreed that higher rates will continue until prices start to come down. Officials further noted that with inflation “showing little sign so far of abating … they had raised their assessment of the path of the federal funds rate that would likely be needed to achieve the Committee’s goals.”

“Participants commented that recent inflation data generally had come in above expectations and that, correspondingly, inflation was declining more slowly than they had previously been anticipating.” They lowered their projections for the economy, expecting GDP to grow at only a 0.2% annualized pace in 2022 and just 1.2% in 2023.

They said inflation was being driven by supply chain problems that were not limited to goods but also to a shortage of labor. The US labor market remains robust despite months of rate hikes. (CNBC)

Wipro profits fall 9% YoY even as Revenue rises 14.6%

Wipro saw Q2 revenue jump 14.6% to Rs. 22,540 Cr (~$27B) but profits after tax declined 9.3% to Rs. 2,660 Cr. (~$3.2B) (INR 2,880 Cr. expected). operating margin in the IT services segment grew 16 basis points QoQ during the quarter to 15.1%. In constant currency terms, the IT services segment revenue increased by 4.1% QoQ and 12.9% YoY. Wipro's top 5 clients grew 19% YoY, and the top 10 clients grew 17% YoY in constant currency terms.

Wipro said it expects revenue from the IT services business to be in the range of $2,811-$2,853 million, which translates to a sequential growth of 0.5% to 2%.

Wipro derived 35.2% of its revenue from BFSI, 18.8% from consumer and 11.4% from health. Top 10 clients contributed around 21% to its revenue. In the quarter, 62% of the revenues came in USD currency, 10% in GBP and 9% in Euro.

“We achieved margins of 15.1% in Q2 after absorbing the impact of salary increases and promotions. Our margin improvement was led by better price realisations and strong operational improvements in automation-led productivity”, Wipro CFO said.

Wipro shares tumbled 5.9% after the result. (Economic Times)

PepsiCo beats expectations and raises guidance as customers willing to pay higher for their products

PepsiCo reported EPS of 1.97 (1.84 E) on Revenue of $21.97B ($20.78B E) which represents an 8.8% YoY growth. Unfavorable currency translation reduced revenue growth by 3 percentage points.

Volume declined 1.5% in convenient foods and edged up 3.0% in beverages. On an organic basis, volumes declined 1% while effective net pricing increased 17%. Cost of sales increased more than revenue growth, up 9.7% to $210.31 billion, as gross margin contracted to 53.1% from 53.5%.

Inventories increased 15.5% to $5.02 billion, after rising 21.6% in the second quarter and increasing 9.5% in the first quarter.

Revenue from PepsiCo Beverages North American rose 3.6% to $6.64 billion, Frito-Lay North America jumped 19.6% to $5.56 billion, Europe increased 0.9% to $3.65 billion and Latin America grew 19.9% to $2.52 billion. Quaker Oats North America revenue was up 15.4% to $713 million. Chief Financial Officer Hugh Johnston said elasticity continues to be “strong and stronger than expected” year to date meaning that PepsiCo expects to be able to charge higher prices from consumers.

The company raised forward guidance and now expects full-year EPS of $6.73 up from $6.63. The company affirmed its plan to return $7.7 billion to shareholders this year, including $6.2 billion through the payment of dividends and $1.5 billion through the repurchase of shares.

PepsiCo stock climbed 4.2% to close at $169.39, the biggest one-day gain since it ran up 5.7% on April 14, 2020. (Marketwatch)

US WASDE report shows lower than expected Soybean yields

USDA’s monthly WASDE report showed that Soybean yield was below analyst expectations.

Corn and Wheat yield projections were in line with estimates.

The market reacted to the news with soybean futures rising 20 cents across the nearby months. (RealAgriculture)

14th Oct 22 (Friday)

US CPI at 8.2% remains hot. Fast Retailing (Uniqlo) sets record profits. TSMC profits up 80%. Blackrock AUM drops 16%.

US CPI remains higher than expected confirming 75bps in Nov and with prediction of another 75bps hike in December with a 62% probability.

German CPI rises to 10%, increasing 1.9% MoM in September. China CPI increases to 2.8% YoY, pace of increase seen quickening as food prices soar. IMF cut its 2022 & 2023 China growth forecasts to 3.2% & 4.4%. MAS tightened monetary policy for the 4th time to combat a 14-year high inflation.

Fast Retailing reported Q4 net of 35.5B Yen (14.9B Yen E) with full year net profit of 273.3B Yen, up 61% YoY. Infosys net profit rises 11%, forward guidance raised. TSMC net profit rises 80% YoY as margins improve sharply.

Blackrock mixed on earnings as revenue drop 14% YoY, AUM drops 16%. Progressive misses earnings as losses mount from Hurricane Ian.

US annual inflation seen slowing to 8.2% but remains higher than expected cementing further rate hikes. Core CPI rises 0.6% MoM with shelter costs soaring.

US CPI was reported at 0.4% MoM (0.2% E) in September up from 0.1% in August. This marks an 8.2% YoY increase (8.1% E) down from 8.3% in August. Core CPI, which excludes volatile food and energy prices, increased 0.6% MoM (0.5% E) in September, marking a 6.6% YoY increase (6.5% E). The food index rose 0.8% for the month and was up 11.2% YoY. Energy prices declined 2.1% with gasoline prices dropping 4.9%, energy prices have rebounded in October so this decline will likely reverse in the next report.

Shelter costs which make up 1/3rd of the CPI increased 0.7% MoM. Owners equivalent rent increased 0.8% MoM in its largest increase since 1990. Transportation services costs increased 1.9% MoM while medical services costs increased 1% MoM. Air fares increased 0.8% MoM and stand 42.9% higher YoY. Used vehicle prices fell 1.1% MoM while new vehicle prices rose 0.7%. Apparel posted a 0.3% MoM decline. Egg prices even dropped, off 3.5% for the month though still up 30.5% from a year ago.

CPI has dropped from its peak of 9% in June but remains at elevated levels and seems to be dropping off far slower than anticipated despite the Fed hiking interest rates by 3% since March. This higher-than-expected reading cemented a 75bps hike at the Fed’s November meeting with traders assigning a 98% chance to 75bps. Traders are also predicting a 75bps hike in December with a 62% probability.

On an inflation adjusted basis, average hourly earnings for workers declined 0.1% MoM.

Initial jobless claims increased 9k to 228k last week. Unadjusted claims jumped 32,275 to 199,662. The number of people receiving benefits after an initial week of aid, a proxy for hiring, rose 3,000 to 1.368 million. Jobless claims remain elevated because of Hurricane Fiona. (Reuters, CNBC, BLS)

German CPI rises to 10%, increasing 1.9% MoM in September

German CPI increased to 10% YoY in September as expected from 7.9% previously. CPI increased 1.9% MoM. Harmonized with the rest of the EU, inflation increased 10.9% YoY (+2.2% MoM).

Inflation rate excluding energy and food was 4.6% YoY. ECB is struggling to control inflation in the EU with soaring energy prices (+43.9% YoY) and food prices (18.7% YoY).

Additionally, the end of government transport subsidies in September likely led to a 1% increase in inflation. Transport prices have increased 14% YoY. Goods increased by 17.2% YoY. While services increased just 3.6% YoY in price. (Destatis)

China CPI increases to 2.8% YoY, pace of increase seen quickening as food prices soar

China CPI increased to 2.8% YoY in September as expected up from 2.5% in August. Core inflation which excludes food and energy prices increased 0.6% YoY down from 0.8% in August. PPI grew at its slowest pace in a year rising 0.9% YoY (1% E) down from 2.3% YoY in August.

Food prices rose 8.8% on year from a 6.1% gain in August. Pork prices leapt 36.0% from 22.4% growth a month prior and vegetable prices jumped 12.1% from a 6.0% rise previously. Another COVID surge in the country is expected to hamper economic activity.

The International Monetary Fund on Tuesday cut its 2022 and 2023 economic growth forecasts for China to 3.2% and 4.4%, respectively, saying the frequent lockdowns under the country's zero-COVID policy have taken a toll. (Reuters)

IEA Report highlights slowing demand for oil. Oil prices fall on US CPI report

IEA’s oil market report highlighted that the demand for oil was slowing as frequent Chinese lockdowns and an ongoing slowdown in the OECD weigh on demand. World oil demand is forecast to rise by 2 mb/d in 2022 and 2.1 mb/d in 2023, marginally lower than in last month’s Report.

World oil production rose 790 kb/d in August to 101.3 mb/d, with a strong recovery in Libya and smaller gains from Saudi Arabia and the UAE offset by losses in Nigeria, Kazakhstan and Russia. Production growth is forecast to slow, edging up by just 280 kb/d to 101.6 mb/d in the next 4 months.

Russian total oil exports rose by 220 kb/d in August to 7.6 mb/d, down 390 kb/d from pre-war levels. Estimated export revenues fell by $1.2 bn to $17.7 bn. Global observed inventories fell by 25.6 mb in July on a drawdown in crude stocks in China and oil on the water as well as from IEA government stocks. OECD industry stocks rose by 43.1 mb to 2 705 mb. IEA member countries released nearly 180 mb of public stocks from March through August, with over 50 mb to be delivered through October.

Brent futures lost $34/bbl and backwardation fell 65% in just three months following a June peak, reflecting a seasonal slowdown in refinery purchases and increased supplies, as well as escalating concerns about the world economy.

Following the US CPI report, oil prices fell. WTI crude prices fell 1.57% to $85.90, while Brent crude fell 1.16% to $91.38 per barrel. (IEA, Oilprice)

MAS tightens monetary policy by re-centering midpoint of exchange rate

Monetary Authority of Singapore tightened monetary policy as expected for the fourth time this year to combat inflation running near a 14-year high and left the door open for further policy action as it warned of risks to the growth and price outlook.

The MAS said it will re-centre the mid-point of its exchange rate-based policy band up to prevailing levels but kept the slope and width of the band unchanged. Friday's move, seen by some as less aggressive as MAS adjusted only one of the three levers in its policy band, marked the fifth tightening since last October.

The MAS manages monetary policy through exchange rate settings. It adjusts its policy via three levers: the slope, mid-point and width of the policy band, which let the Singapore dollar rise or fall against the currencies of its main trading partners within an undisclosed band. (Reuters)

Fast Retailing posts record profit of 273B Yen on strong Uniqlo sales abroad

Fast Retailing reported Q4 net profit of 35.5B Yen (14.87B Yen E) marking a full fiscal year net profit of 273.3B Yen, up 61% YoY. Fiscal-year revenue increased 7.9% to Y2.301 trillion. Fourth-quarter revenue was Yen 536.02 billion (506B Yen E).

A recovery from the coronavirus pandemic has led to a rebound in demand. The rapid fall of the yen against other major currencies also contributed to the result by increasing the value of its overseas earnings.

Fast Retailing projected revenue to increase 15% to Y2.650 trillion and net profit to drop 16% to Y230.00 billion for the fiscal year that started in September. The company said it planned to limit discounts at Uniqlo stores in Japan while adding more stores overseas, especially in Asia.

They aim to triple Uniqlo sales in Europe to Y500.0 billion in five years, from about Y130.0 billion for the fiscal year ended August, and to achieve an operating profit margin of 20% from about 12%. They have observed strong sales in Europe and brand recognition in the region has improved.

The company plans to pay Y680.00 a share in dividends this fiscal year, up from Y620.00 the previous fiscal year. (Nippon, Marketwatch)

Infosys net profit rises 11%, forward guidance raised

Infosys reported revenue of Rs 36,538 Cr. (~ $4.4B) (Rs. 36,564 Cr. E) up 23.4% YoY. Net profit increased 11.3% YoY to Rs. 6,021 Cr. (~$730M) (Rs. 5902 Cr. E). Infosys total contract value (TCV) for Q2 came in at $2.7 billion. Of that, 54 per cent were net new deals.

Operating margins improved 1.5% to 21.5%. The margins saw a favorable impact of currency movements (70 basis points) and cost optimisation (90 basis points) benefits.

Infosys raised its revenue guidance for FY23 to 15-16% from the 14-16% earlier. The company also announced a buyback of shares worth Rs 9,300 crore. The board has fixed the buyback price at Rs 1,850 per share, which is a premium of 30 per cent over Thursday’s closing price of Rs 1,419.7. The firm’s board has approved an interim dividend of Rs 16.50 per share. (Business Standard)

Taiwan Semiconductors net profit rises 80% YoY as margins improve sharply

Taiwan Semiconductors reported net profit for Q3 of 280.87B (~$8.83B), up 80% YoY. Third-quarter revenue increased 48% on year to NT$613.14 billion (~$19.23B). The company's operating profit margin improved by 9.4% from a year earlier to 50.6%. Revenue from smartphones rose 25% from the previous quarter, while revenue from high-performance computing increased 4%.

TSMC said revenue from customers in North America made up 72% of the third-quarter total, up from 64% in the second quarter, while revenue from China accounted for 8%, down from 13% in the previous quarter.

TSMC said it was scaling back on capital spending for the year to $36 billion from a previously estimated $40 billion to $42 billion given a sharp flip in the global chip supply.

For the fourth quarter, TSMC executives guided for revenue between $19.9 billion and $20.7 billion, while analysts had modeled $19.84 billion on average. (Marketwatch, Marketwatch)

Blackrock mixed on earnings; AUM drops 16%

Blackrock reported EPS of 9.55 (7.65 E) on revenue of $4.31B ($4.35B E), down 14.6% YoY. Net income declined 16% to $1.41B.

Assets under management (AUM) dropped 16% to $7.96 trillion. Equity net flows were down $29.28 billion to $4.02T. fixed income were up $90.62 billion to $2.35T. By client type, retail net flows were down $4.89 billion, exchange-traded funds (ETFs) was up $22.37 billion and total institutional was up $47.73 billion. Total inflows for the quarter fell to $17B from $90B in the previous quarter.

Investment advisory and administration fees fell to $3.37B from $3.53B previously. Technology services produced $338M in revenue up QoQ. Distribution fees made $325B down QoQ.

Total expenses declined to $2.79B in the quarter from $2.86B previously. (Marketwatch, SeekingAlpha)

Progressive misses earnings as losses mount from Hurricane Ian

Progressive reported EPS of 0.2 (1.43 E) on revenue of $13.02B (13.32B E), up 5% YoY.

Progressive saw solid growth in commercial lines, increasing 9%. Its auto business declined leaving policies in force 1% higher. Progressive’s combined ratio for the full quarter was 99.2 indicating that they made $0.8 on every $100 of premium.

However, notably, the combined ratio spiked in September to 116.2 leading to a loss of $684M, $350M of which came from underwriting while the rest was from unrealized investment losses.

The huge underwriting loss was in anticipation of losses from Hurricane Ian. (SeekingAlpha)

Walgreens beats earnings but revenue falls YoY

Walgreens reported EPS of 0.8 (0.77 E) on revenue of $32.4B ($32.07B E), up 5.3% YoY. On a net basis, the company swung to a loss of $415 million, or 48 cents a share for the quarter. This includes nonrecurring items, such as impairment charges related to intangible assets in Boots UK.

U.S. retail pharmacy sales fell 7.2% to $26.7 billion while same-store sales increased 1.6%. Cost of sales fell 2.7% to $26.04 billion, as gross margin contracted to 19.8% from 21.9%.

Its international business took a big hit from currency headwinds. It had fourth-quarter sales of $5.1 billion, a drop of 6.6% from the year-ago period. That included a 13.3% adverse currency impact.

Walgreens expects fiscal 2023 EPS of $4.45-$4.65. U.S. Healthcare fiscal 2025 sales target was raised to $11 billion to $12 billion from $9 billion to $10 billion. (Marketwatch, CNBC)

Delta revenue exceeds expectations as they claim continued travel recovery

Delta Airlines reported EPS of 1.51 (1.55 E) on revenue of $13.98B ($12.91B E), up 11% YoY. The air carrier’s net income of $695 million was down from $1.5 billion in 2019. Delta’s fuel bill for the third quarter rose nearly 48% from 2019 to $3.32 billion. Stripping out fuel, costs per available seat mile were up close to 23% from 2019 in the last quarter. The airline said business bookings were 80% recovered to pre-pandemic levels.

International travel, largely sidelined in 2020 and 2021, was a bright spot in the third quarter, with unit revenue growth outpacing domestic for the first time since the pandemic started.

“The travel recovery continues as consumer spend shifts to experiences and demand improves in corporate and international,” said Ed Bastian, Delta’s CEO, in a statement.

For the fourth quarter, Delta expects revenue up 5% to 9% from 2019. FactSet consensus of $11.75 billion implies 0.3% growth. The carrier expects fourth-quarter earnings of $1.00 to $1.25 a share, compared with FactSet’s consensus of 79 cents a share. (CNBC, Marketwatch)

Domino’s Pizza tops revenue estimates, stock rallies 6%

Domino’s Pizza reported EPS of 2.79 (2.98 E) on revenue of $1.07B, up 7% YoY. The company posted net income of $100.5 million, down 16% YoY.

International same-store sales fell 1.6%, while U.S. same-store sales were up 2%. The company opened 225 net new stores in the quarter, 24 in the U.S. and the remaining 201 internationally.

The company is expecting the negative impact of the strong dollar on royalty revenue to rise to $29 million to $31 million for fiscal 2022. It still expects a food basket pricing increase of 13% to 15% for fiscal 2022. (Marketwatch)

15th Oct 22 (Saturday)

Aluminum spikes 7% on Russia ban. JP Morgan, Citi, HDFC, US Bancorp, PNC Financials beat earnings. EU trade deficit at record high.

Aluminum price spikes 7% after potential Russia ban on the London Metal Exchange.

JP Morgan reported EPS of 3.12 (2.92 E) on revenue of $32.7B ($32.13B E) rising 10% YoY. HCL Tech reported revenue of Rs. 24,686 Cr. (~$3B) beating estimates of Rs. 24,382 Cr. growing 19.5% YoY.

Morgan Stanley reported EPS of 1.53 (1.52 E) on revenue of $13B ($13.23B E) slumping12% YoY.

Citigroup reported EPS of 1.5 (1.48 E) on revenue of $18.5B ($18.35B E) with revenue rising 6.3%. HDFC Bank reported PAT of Rs. 10,605 Cr. (~$1.28B) up 20% YoY (16% E).

India’s annual wholesale price index (WPI) eased to 10.7% YoY in Sep (11.5% E) from 12.41% in Aug.

EU Trade deficit at all time high in Aug at €50.9B. Trade deficit has ballooned from €34B in Jul. German WPI surged in Sep rising 19.9% YoY from 18.9% in Aug.

US retail sales stayed flat in Sep (0.2% MoM increase E). US import prices dropped 1.2% (1.1% decline E) in Sep marking 3rd straight month of declining prices. US business inventories rose 0.8% MoM in August (0.9% E). Canada wholesale trades increased 1.4% MoM in August (0.8% E).

EU trade deficit widens to new all-time-high as energy prices soar

EU Trade Deficit in August widened to €50.9B. EU’s trade deficit has ballooned from €34B in July. Previously, EU had generally recorded large surpluses, the shift to deficit has largely been led by soaring prices of energy imports due to the war in Ukraine.

Payments for energy imports have risen by 154% in the period between January and August to 543.8 billion euros, contributing to an overall trade deficit of 309.6 billion euros.

EU imports rose by 53.6% YoY to 282.1B Euros. Exports increased 24% YoY to 231.1B Euros. (Reuters)

US retail sales flat in September, August reading revised up

US retail sales stayed flat in September (0.2% MoM increase expected). August reading for retail sales was revised up from 0.3% to 0.4% MoM. Retail sales were up 8.2% YoY in September. Core retail sales which exclude automobiles, gasoline, building materials, and food services, rose 0.4% MoM in September.

Sales at auto dealerships slipped 0.4% last month, while receipts at service stations dropped 1.4%. Furniture store sales fell 0.7%, while those at building material and garden equipment retailers decreased 0.4%.

Receipts at electronics and appliance stores declined 0.8%. There were also decreases in sales at hobby, musical instrument and book stores, a sign that consumers were pulling back on discretionary spending. Sales at clothing and general merchandise stores rose as did those of online and mail-order retailers. Receipts at bars and restaurants, the only services category in the retail sales report, increased 0.5%.

A survey from the University of Michigan on Friday showed consumer sentiment improved further in October, but inflation expectations deteriorated a bit as average national gasoline prices moved back up. (Reuters)

US import prices fall 1.2% on strong dollar

US import prices dropped 1.2% (1.1% decline E) in September marking the third straight month of declining import prices. Still, import prices are 6% higher YoY. Imported fuel prices dropped 7.5% in September while food import prices increased 0.2%. Excluding fuel and food, import prices fell 0.5%.

US export prices dropped 0.8% in September (1% decline expected) after plunging 1.7% in August. Export prices are 9.5% higher YoY. Prices for agricultural exports decreased 1.0%, pulled down by lower prices for soybeans, fruit, meat and nuts. Nonagricultural export prices declined 0.9%.

Falling import prices also suggested an easing of bottlenecks in the global supply chain, which was reflected in unchanged readings in underlying consumer and producer goods prices in September.

The reduction in core import prices reflects the strong Dollar as it helped the US stave off higher import prices that are wreaking havoc on other countries. The dollar has gained 10.5% against the currencies of the United States' main trade partners since January. (Reuters)

US business inventories increase less than expected as retailers and wholesalers struggle with excess merchandise

US business inventories rose 0.8% MoM in August (0.9% E). Inventories are up 18.2% YoY. Retail inventories jumped 1.3% in August (1.4% E). Motor vehicle inventories rose 3.5% (3.7% E). Retail inventories excluding autos, which go into the calculation of GDP, increased 0.6% as estimated last month.

Wholesale inventories increased 1.3% in August while stocks at manufacturers fell 0.1%. Business sales rebounded 0.3% in August. the ratio of inventories to sales rose to 1.33 from 1.32 in the prior month.

Retailers and wholesalers are finding themselves with excess merchandise as supply chain bottlenecks ease while demand for goods slow. This could see businesses offloading merchandise at discounted rates and putting off new orders at a detriment to manufacturers. (Reuters)

Canada wholesale trade increases 1.4% in Aug

Canada wholesale trades increased 1.4% MoM in August (0.8% E) to 81.3B CAD. In price adjusted terms, wholesale sales rose 1.2%. Wholesale sales are 13.3% higher YoY. after declining 0.6% in July.

The miscellaneous goods subsector, the machinery, equipment and supplies subsector and the food, beverage and tobacco subsector led the growth for wholesale sales in August. Wholesale inventories in Canada rose 1.5% to 123.24B CAD.

Manufacturing sales fell 2% MoM (1.8% decline expected). The drop in manufacturing sales was because of lower sales in petroleum and coal products as well as chemicals. (Yahoo, Marketwatch)

German wholesale prices increase 1.6%

German wholesale price index surged in September rising 19.9% YoY from 18.9% in August. WPI increased 1.6% MoM after a 0.1% MoM increase in August.

The largest impact came from cost of mineral oil products (61.9%), solid fuels (111.9%), petroleum products (61.9%), chemical products (42.0%), grain, unmanufactured tobacco, seeds, etc (30.8%). (SeekingAlpha)

India wholesale prices ease in September

India’s annual wholesale price index (WPI) eased to 10.7% YoY in September (11.5% E) from 12.41% in August. The Wholesale Price Index (WPI) had touched a record high of 15.88% in May.

Food inflation based on WPI Food Index also decreased to 8.08% in September from 9.93% in August. However, inflation in vegetables rose to 39.66% from 22.29% in August.

In the fuel and power basket, inflation came in lower at 32.61% in September, against 33.67% in August. In manufactured products and oil seeds it was 6.34% and (-) 16.55%, respectively. (Livemint)

HCL Tech reports profit rising 7% YoY

HCL tech reported revenue of Rs. 24,686 Cr. (~$2.99B) beating analyst estimates of Rs. 24,382 Cr. Revenue increased 19.5% YoY. HCL reported consolidated net profit of Rs. 3,489 Cr. (~$420M) up 7.1% YoY and above analyst estimates of Rs. 3,418 Cr. the board of directors have approved a dividend of Rs 10 per share.

In constant currency terms, revenue increased 16% YoY. EBITDA margin in the quarter improved to 0.9% to 18% as operating leverage and efficiencies helped offset impact of salary hikes.

The share of revenue from Americas for HCL Tech increased by 60 bps on quarter to 64.8 per cent in Q2. However, the share of revenue from Europe dipped by 30 bps to 27.5 per cent. Still, EU revenue growth was better than the US in constant currency terms.

HCL raised forward guidance in an unexpected move. HCL Tech now sees 13.5-14.5 per cent growth in revenue in constant currency, against 12-14 per cent projected earlier. However, EBITDA margin guidance was lowered to 18-19% from 19-20%. Service revenue is now expected to grow 16-17% YoY in FY23. (Economic Times)

United health beat expectations, raise outlook again as stock surges

United health reported EPS of 5.79 (5.43 E) on revenue of $80.9B ($80.52B E). Revenue increased 11.8% YoY. Net income rose to $5.26B, up 28% YoY. Revenue from premiums rose 13.2% to $64.49 billion, exceeding expectations of $63.77 billion, while products revenue increased 5.6% to $9.19 billion and services revenue were up 8.7% to $6.70 billion.

Growth in the third quarter was driven by continued expansion in the number of people served throughout UnitedHealthcare and Optum Health. Total people served at its UnitedHealthcare business segment increased by 185,000. Optum revenue grew 17% to $46.6 billion.

Total operating costs rose less than revenue, up 10.2% to $73.43 billion, as operating earnings as a percentage of revenue improved to 9.2% from 7.9%.

The company raised its 2022 adjusted EPS guidance yet again to range of $21.85 to $22.05 from the range of $21.40 to $21.90 previously. (Marketwatch)

JP Morgan beats earnings estimates on higher-than-expected interest income

JP Morgan reported EPS of 3.12 (2.92 E) on revenue of $32.7B ($32.13B E). Revenue increased 10% YoY. However, net income fell 16.7% to $9.74B. JPMorgan Chase’s total assets under management fell 13% to $2.6 trillion in the face of losses in the equities market and difficult conditions in the bond market.

The bank said a net credit reserve build of $808 million ate into its net income for the latest quarter. Meanwhile, expenses rose 2.3% QoQ.

Net interest income climbed 34% to $17.6 billion and net interest income excluding its Markets unit rose 51% over the year-ago period to $16.9 billion on higher interest rates. The bank’s trading revenue of $6.8 billion also beat estimates.

JP Morgan expects Q4 net interest income of $19B higher than analyst estimates of $18.2B. JPM said it expects to meet its capital requirements under the international Basel III banking guidelines and resume stock buybacks early in 2023.

JPMorgan’s head count grew to 288,474 as of Sept. 30, up from 278,494 at the end of the second quarter and 265,790 at the end of the third quarter of 2021.

JPM shares rose 2.6% on the announcement. (Marketwatch)

Morgan Stanley misses earnings estimates, stock falls 5%

Morgan Stanley reported EPS of 1.53 (1.52 E) on revenue of $13B ($13.23B E). Revenue declined 12% YoY. Net income fell 32% to $2.7B. Morgan Stanley delivered 15% return on tangible common equity.

Wealth Management added an additional $65 billion in net new assets and produced a pre-tax margin of 28%, excluding integration-related expenses.

Investment banking revenue fell 55% to $1.28 billion in the quarter. Investment management revenue dropped 20% to $1.17 billion.

Morgan Stanley shares fell 5% on the announcement. (Marketwatch, CNBC)

Wells Fargo stock rises despite profit miss

Wells Fargo reported EPS of 1.3 (1.1 E) on revenue of $19.51B ($18.76B E). Revenue increased 3.5% YoY. Net income fell 31% to $3.528B. Chief Executive Charlie Scharf said performance was "significantly impacted" by $2 billion, or 45 cents a share, in operating losses "related to litigation, customer remediation, and regulatory matters primarily related to a variety of historical matters."

Wells Fargo is seeing historically low delinquencies and high payment rates and said the timing of deterioration in those measures due to high inflation remains unclear.

Wells Fargo reported “significant” year-over-year revenue growth of 42% in its commercial banking unit, while consumer banking fell 30% and mortgage banking dropped 80%

They set aside $784M in provisions for loan losses after reducing them by $1.3B last year. Net interest income rose 36%, while noninterest income fell 25%, hurt by a decline in mortgage banking income amid a decline in originations.

Wells Fargo stock rose 3% despite the net income miss. Wells Fargo said it was reducing head count in its mortgage unit as demand for home loans falls in the face of higher interest rates. (Marketwatch)

Citigroup beats earnings estimates but take a hit on divestiture

Citigroup reported EPS of 1.5 (1.48 E) on revenue of $18.5B ($18.35B E). Total revenue increased 6.3%. Citi said its net income dropped 23% to $3.5B. The results included a $520 million pretax gain on the sale of its Asia consumer business.

The decline in profit came in part from an increase in loan loss reserves. Citigroup grew its allowance for credit losses by a net of $370 million during the quarter.

On the trading front, Citigroup reported $3.06 billion in fixed income revenue and $1.01 billion in equities revenue. Analysts were expecting revenue of $3.19 billion and $965 million. Personal banking revenue rose 10% YoY. The bank reported $631 million in investment banking revenue for the third quarter, down more than 60% year over year.

Citigroup also said it continues to scale back its business in Russia. It will end “nearly all of the institutional banking services we offer” in the next quarter as it works to wind down its presence there. (Marketwatch, CNBC)

PNC Financials reports increase in profit and revenue

PNC Financials reported EPS of 3.78 (3.72 E) on revenue of $5.55B (5.41B E). Revenue increased 6% YoY. Net income attributable to common shareholders increased 9.8% to $1.56B.

Net interest income rose 7% to $3.5 billion, driven by higher yields on interest-earning assets and loan growth, partially offset by higher funding costs. Noninterest income fell 11% to $2.07 billion on the back of the acquisition of BBVA USA and higher merger and acquisition advisory fees.

PNC assigned a provision of $241M for credit losses in the quarter up from $36M in Q2. (Marketwatch)

US Bancorp beats earnings estimates as revenue rises

US Bancorp reported EPS of 1.18 (1.14 E) on revenue of $6.3B ($6.24B E). Revenue was up 7.4% YoY. Profit declined 10% to $1.81B. Merger and integration-related charges associated with the bank's acquisition of MUFG Union Bank added up to $42 million, or $33 million net of taxes, dragging earnings down by 2 cents a share.

Net interest income was $3.86 billion, compared with $3.17 billion last year. Provision for credit losses was $362 million, compared with a benefit of $163 million in the year-ago period. (Marketwatch)

First Republic beats earnings as revenue rises

First Republic Bank reported EPS of 2.21 (2.19 E) on revenue of $1.5B ($1.55B E). Revenue increased 17% YoY. Net income increased 20% to $445M. Loans increased 24% YoY to $158.8B.

First Republic booked a provision for credit losses of $36M due to higher loan growth.

First Republic declared a quarterly cash dividend of 27 cents. (Marketwatch)

HDFC Bank reports strong net-profits and double-digit growth on bottom-line

HDFC Banks reported Profit After Tax of Rs. 10,605 Cr. (~$1.28B) up 20% YoY (16% E). Net interest income increased 19% YoY to Rs. 21,021.2 Cr. (~$2.55B). Core net interest margin was at 4.1 percent on total assets, and 4.3 percent based on interest-earning assets.

HDFC Bank increased total loans 23.4% to Rs 14.4 Lakh Cr. while the balance sheet size expanded 21%. Domestic retail loans grew by 21.4 percent, commercial and rural banking loans grew by 31.3 percent and corporate and other wholesale loans grew by 27 percent. Overseas advances constituted 3.1 percent of total advances.

HDFC’s total deposits grew 19% YoY to Rs. 16.73 Lakh Cr. as Current Account Savings Account deposits grew 15.4%.

HDFC’s asset quality improved in the quarter as gross non-performing assets dropped to 1.23%.

Provisions and contingencies for bad loans dropped to Rs 3,240.1 Cr. from Rs. 3,927 Cr.

HDFC’s Capital Adequacy Ratio was at 18% as against a regulatory requirement of 11.7%. (Moneycontrol)

Aluminum price spikes 7% after potential Russia ban

Aluminum prices on the London Metal Exchange spiked 7% higher before ending the day 3.3% higher. The spike was a result of reports that the Biden administration was considering increased tariffs on Russian Aluminum in order to price out Russia producer Rusal.

Rusal is the world's largest aluminum producer outside China, supplying the world with 6% of its needs estimated at around 70 million tons this year. After the U.S. Treasury Department imposed sanctions on Rusal and the LME barred its metal in 2018, aluminum prices rose 30% over the course of a few days.

The LME last week launched a discussion paper on the possibility of banning Russian aluminum, nickel and copper from being traded and stored in its system. (Reuters)

French CPI declines in September, French government will spend $100B Euros to stave off inflation

French CPI, harmonized with the rest of the EU, fell by 0.5% MoM. On an annual basis HICP increased 6.2% YoY in September down from 6.6% in August. The French government has spent a considerable amount of money in its fight against inflation by establishing aggressive price caps on energy and establishing grants and boosting welfare and pension payouts.

French finance minister stated that France will have spent 100B Euros from 2021-2023 in helping control cost-of-living in the country. (Yahoo)

Spain inflation slows to 9% YoY in September

Inflation in Spain eased in September as CPI slowed to 8.9% YoY (9% E) from 10.5% YoY in August. Harmonized with the rest of the EU, inflation slowed to 9% YoY (9.3% E). Core inflation, which strips out volatile food and energy prices, fell to 6.2% year-on-year in September, from 6.4% in August.

Spain's 12-month inflation in September was its slowest rate since May 2022 giving the first signs of inflation in the country slowing after ECB hiked interest rates in the Eurozone. Still, inflation remains elevated due to price of food and energy still soaring. Food and non-alcoholic beverage prices grew 14.4% in September. (Reuters)