Mint Market Watch | 3/Oct to 8/Oct

Mint Market Watch | 3/Oct to 8/Oct

Attention Oil - OPEC+ meets to cut production; US Sep Non-farm Payroll numbers; PMI numbers in China, US, UK and Rate decisions in AU/NZ

Attention Oil - OPEC+ meets to cut production; US Sep Non-farm Payroll numbers; PMI numbers in China, US, UK and Rate decisions in AU/NZ.

3rd Oct 22 (Monday)

Attention shifts to oil this week. On Wed this week, for the first time since Mar 2020, OPEC+ members will meet in person. Expectation is that OPEC+ will discuss to cut production collectively by more than 1 million bpd (~1% of global supplies). OPEC+ actions could push up oil prices further entrenching global inflation.

Amrita Sen of Energy Aspects said that OPEC+ was concerned about global slowdown risk and the resultant impact on oil demand. As a pre-emptive measure OPEC+ was considering large cuts to sustain oil prices. Brent Crude has fallen to $85/barrel (nearly ~30%) from $120 in June.

In equity markets, after a brutal month of September, investors would hope for some respite. Will there be any? Seems unlikely.

This week will bring a host of Federal Reserve Bank speakers. Expectation is that the central bankers will reiterate the goal to not pull back prematurely on restrictive monetary policy and higher rates.

The September jobs report at the end of the week will bring out the US Non Farm Payroll numbers.

Among investor events, presentations by Duke Energy, Hasbro and Box might be of interest. Also Google hosts its Pixel hardware event this week.

TOP ECONOMIC EVENTS THIS WEEK

OPEC+ Meeting

US Nonfarm payrolls

Australia Interest Rate Decision

New Zealand Interest Rate Decision

US JOLTs Job Openings

UK Nationwide HPI

EU, US, UK, Japan and China PMI

US Trade Balance and Factory Orders

German Trade Balance

German Industrial Production

4th Oct 22 (Tuesday)

Global manufacturing activity declining due to worldwide slowdown and cost pressures; EU hits 27-month low.

S&P Global’s PMI survey’s showed manufacturing activity slowing globally. Manufacturing activity across the Eurozone declined further last month as the PMI fell to 48.4 (48.5 E) in September from 49.6 in August, this is the lowest reading in 27 months. Manufacturing activity in Germany contracted for the 3rd straight month, while activity in France contracted at the fastest pace since 2020. Italian activity declined but the pace of decline slowed.

Manufacturing activity shrank in Taiwan (42.2) and Malaysia (49.1) and grew at a slower pace in Japan (50.8), India (55.1) and Vietnam (52.5), as rising raw material costs and the darkening global outlook weighed on corporate sentiment. Meanwhile, PMI data from China last week also showed that manufacturing activity in the country was slowing due to dampened sales and strict COVID lockdowns.

Source: Reuters

US ISM manufacturing PMI falls to 50.9 as new orders and employment contracts

ISM’s survey showed the US Manufacturing PMI fell to 50.9 (52.2 E) in September from 52.8 in August. This marks the slowest growth for the manufacturing sector in the country in two-and-a-half years. The survey also showed that manufacturing employment contracted in September as price pressures at factory and supply bottlenecks started to ease.

The ISM survey's forward-looking new orders sub-index fell to 47.1 last month from 51.3 in August. The ISM's measure of supplier deliveries fell to 52.4 from 55.1.

The measure of prices paid by manufacturers dropped to 51.7 from 52.5 in August.

The ISM survey's measure of factory employment dropped to 48.7 from 54.2 in August.

The ISM survey's measure of factory employment dropped to 48.7 from 54.2 in August.

At the same time, S&P Global’s Manufacturing PMI for the US edged up to 52 from 51.5. Some of the slowdown in manufacturing reflect the rotation of spending from goods to services.

Meanwhile, construction spending in the US declined 0.7% (0.3% E) in August, marking the sharpest decline since 2021. Spending on private construction projects fell 0.6%. Investment in residential construction declined 0.9%, with spending on single-family projects plunging 2.9%. Outlays on multi-family housing projects rose 0.4%.

Tankan Large Manufactures Outlook for Q3 drops to 8, non-manufacturer outlook index improves to 14

Tankan survey showed that Japan’s Large Manufacturers Outlook Index for Q3 dropped to 8 from 9 in the prior quarter (11 E). Meanwhile, outlook for non-manufacturers in the country improved to 14 from 13 previously (13 E). A reading above 0 indicates improving conditions, however this marks the 3rd straight quarter of deteriorating conditions. The survey also showed that CAPEX by all big industry in the country is expected to increase 21.5% in the current fiscal year after a 2.3% drop in the previous year.

"Big manufacturers' sentiment was surprisingly weak as slowing global growth took a toll on the materials sector through declines in commodity prices… If the global economy slows further, other sectors may also see sentiment worsen" said Takeshi Minami, chief economist at Norinchukin Research Institute.

The survey also showed companies expect inflation to stay around the BOJ's 2% target for years to come. Companies expect inflation to hit 2.6% a year from now and 2.1% three years ahead, the tankan showed. Respondents project inflation of 2% five years ahead, the highest level since comparable data became available in 2014.

Source: Reuters

UK manufacturing PMI (48.4) shows falling output due to weak foreign demand

UK’s Manufacturing PMI increased to 48.4 (48.5 E) from August’s low of 47.3 however it remained below 50 indicating contraction in the sector. Manufacturing output fell for a third month in a row in September and orders declined for a fourth consecutive month, hurt by falling foreign demand.

September saw new export business contract at the quickest pace since May 2020, with reports of lower demand from the U.S., the EU and China. Manufacturers faced weak global market conditions, rising uncertainty, high transportation costs reducing competitiveness and longer lead times leading to cancelled orders.

Source: Reuters

Australia building approvals increase 28% in August following an 18% decline

Building approvals in Australia increased 28.1% in August with a sharp bounce back in apartment approvals. This follows an 18.2% decline in July. Approvals for private sector dwellings excluding houses rose 99.1% in August. Approvals for private sector houses rose 4.1 per cent in August.

The value of total buildings approved rose 23.5% in August, following a 14.8% decrease in July. The value of total residential buildings rose 28.5%, comprising of a 32.6% increase in new residential buildings and a 5.4% increase in alterations and additions.

Source: Mirage News

New Zealand business confidence improves to -42% but remains negative as RZNB is expected to deliver 50 bps hike

New Zealand business confidence measured by NZIER increased to -42% from -65% in Q2. Capacity utilization increased to 94.5% from 93.4% last quarter.

Demand looks to be stabilising at a lower level, suggesting a period of weaker growth in the New Zealand economy ahead. Nearly two-thirds of firms expect to raise prices in the fourth quarter even as the economic outlook deteriorates.

The RBNZ is expected to deliver a 50 bps rate hike on Wednesday as they tackle sky-high inflation. The RBNZ has been at the forefront of global rate hikes but the Fed has closed the gap with three 75-point moves, causing the greenback to surge against most other currencies.

The New Zealand dollar’s 6.3% slump the past month, at one point reaching a 13-year low, may fan inflation by making imports more expensive.

Sources: Forex Live, Bloomberg

Oil prices rally heading into OPEC+ meeting

Brent crude futures for December delivery rose $3.72 to $88.86 a barrel, a 4.4% gain. U.S. West Texas Intermediate crude rose $4.14, or 5.2%, to $83.63 a barrel. This comes as investors look towards the upcoming OPEC+ meeting where they will discuss supply cuts. Russia is pushing for a 1M bpd supply reduction. Most traders are expecting a cut of 50k bpd.

Meanwhile, Saudi Arabia stated that they may raise prices for crude grades sold to Asia following demand recovery and increased output from Chinese refineries. The November official selling prices (OSP) for flagship Arab Light crude may rise by 25 cents a barrel. The backwardation in the Dubai market structure widened during trading last month, implying that demand for crude in the near term is rising. The premium for the front month Dubai over the price for the third month averaged $5.36 a barrel in September, up from $5.07 in August.

The market also expects China, the world's biggest crude importer, to increase purchases as Beijing has issued a fresh round of refined product export quotas, totaling 15 million tons. That could encourage Chinese refineries to lift their crude buying to ramp up fuel output.

Credit Suisse’s Credit Default Swaps surge, share price crashes 10% before recovering after speculation around financial health

The cost of buying insurance against Credit Suisse defaulting surged to a record high. Earlier in the day, one-year CDS were quoted at over 500 basis points, versus just over 300 for the five-year, ICE Data Services pricing shows, shooting past the default risk pricing for its European banking rivals, Barclays Plc and Deutsche Bank.

The prices indicated a roughly 23% chance the Swiss bank will default on its bonds within five years. The troubled Swiss bank’s CDS curve also inverted as investors rushed to protect themselves against a near-term default within the next 12 months.

The surge in CDS was led by speculation after reports that the Swiss lender was looking to raise capital. Executives tried to reassure investors stating that Credit Suisse is at a “critical moment” as they prepare to restructure the business and urged investors not to confuse “day-to-day” stock movements with the Swiss firm’s “strong capital base and liquidity position”. However, assurances failed to assuage fears leading to a volatile day of trading for the stock. Executives also reportedly spent the weekend speaking with investors and clients seeking to reassure them about the financial health of the firm.

Credit Suisse shares tumbled nearly 10% at the start of the day but retraced losses through the day to end 1% lower. Shares have fallen 55% this year, while its euro-denominated bonds hit record lows on Monday.

Sources: Bloomberg, Yahoo, CNBC

Australia’s Central Bank surprises with lower-than-expected 25bps hike

Australia’s central bank surprised markets with a 25bps rate hike. Economists were expecting a 50bps hike. This brings the cash rate to 2.6%. The Reserve Bank of Australia said the lower rate hike will “help achieve a more sustainable balance of demand and supply” in the nation’s economy. They also stated that rates had already risen substantially, however further tightening would still be needed. The RBA has also made it clear that it doesn't think the inflation outlook in Australia is as dire as that in the U.S. economy, given comparatively benign wage growth pressures locally.

With high household debt, and around one-third of mortgage borrowers highly exposed to the fastest pace of interest-rate increases since 1994, the RBA has indicated that it is watching conditions in the housing market very closely.

The Australian dollar was down 0.8% at $0.64625 against the Dollar shortly after the decision.

Sources: Reuters, Marketwatch

5th Oct 22 (Wednesday)

US crude stocks declined by 1.77M barrels (+1.96M gains E). US job market slows as job openings fall by 1.5M in Aug. US orders stay flat in Aug as mfg. sector cools.

RBNZ hikes rates by 50bps to 3.5% as expected making the 5th straight 50bps hike. In their statement, the RBNZ also indicated that they considered a 75bps hike.

US Job Openings fall sharply in August, indicating easing of a tight labor market. US factory orders flat in August as manufacturing growth in the country slows

South Korea inflation slows to 5.6% but central bank tightening likely to continue. RBNZ hikes rates by 50bps and deliver hawkish statement.

Japan services PMI increases to 52.2 as tourism demand expected to increase in October.

Spain unemployment increases 0.6% in September

Spain’s unemployment rate increased 0.6% MoM in September. This represents an increase of 17.6k people.

September marks the 3rd straight month of increases. Still, unemployment in the country is down 9.7% YoY. The implicit jobless rate is at around 12.7% (National Statistics Institute for Q2 2022 of 12.48%).

Source: The Corner

US factory orders flat in August as manufacturing growth in the country slows

Orders for manufactured goods stayed flat at $548.4B in August (0.2% increase expected) following a 1% drop in July. Durable-goods orders fell 0.2% in August, unrevised from the initial estimate.

Orders for nondurable goods were up 0.2% in the month. Decline in orders for transportation equipment led the drop in durable-goods orders.

Still, orders for nondefense capital goods, excluding aircraft, rose a revised 1.4% in August, up slightly from the prior reading of a 1.3% gain.

Sources: Marketwatch, Marketwatch

US Job Openings fall sharply in August, indicating loosening in tight labor market

US job openings declined 1.1M to 10.053M in August (10.775M expected) from (revised lower) 11.17M in the prior month. There are still 1.7 jobs for every unemployed person. Layoff rate rose to 1% (1.5M layoffs) from 0.9% (1.4M layoffs) in the prior month while quit rate stood unchanged at 2.8% as 4.8M people quit their jobs (up from 4.1M in July).

The drop in job openings was accompanied by an increase in the unemployment rate to 3.7% from 3.5% in July. The jobs-workers gap fell to 2.5% of the labor force, or 4.0 million workers, from 3.4% in July

The broad decrease in job openings was led by healthcare and social assistance, with a decline of 236,000. There were 183,000 fewer job openings in other services, while vacancies decreased by 143,000 in the retail trade industry. Fewer job openings were also reported in the financial activities, professional as well as leisure and hospitality industries.

Vacancies in the healthcare and leisure industries declined even though employment in the two sectors remains below its pre-pandemic levels, leading some economists to speculate that other factors besides higher borrowing costs were behind the cool off in demand for workers. "The drop in openings could reflect healthcare providers becoming more accustomed to operating under labor shortages and forgoing hiring," said Veronica Clark, an economist at Citigroup in New York.

Resignations increased in the accommodation and food services industry, where 119,000 more people quit, but decreased by 94,000 in the professional and business services sector.

Sources: Reuters

South Korea inflation slows to 5.6% but central bank tightening likely to continue

South Korea’s headline inflation decreased to 5.6% YoY (5.7% E) in September from 5.7% in the prior month. This is the second straight month of inflation cooling in the country. Core consumer price index, which strips off volatile food and energy prices, fell month-on-month for the first time in a year although its annual rate accelerated to 4.1% from 4.0% in August.

Economists said the latest data suggested inflation was at or past its peak, but expected the central bank to stick to its stance given the weakening won and an aggressive monetary policy in the United States. The Won has weakened 16% against the Dollar YTD.

The Bank of Korea will be announcing their interest rate decisions. Economists expect them to raise rates by 50bps in response to the US Fed tightening with 75bps in September. The Bank of Korea has raised its policy interest rate by a total of 2.0 percentage points since August last year from record-low 0.5% to fight inflation. Governor Rhee Chang-Yong has stated that the tightening stance will continue for some time.

Source: Reuters

RBNZ hikes rates by 50bps and deliver hawkish statement

The Reserve Bank of New Zealand hiked interest rates by 50bps to 3.5% as expected. This marks the 5th straight 50bps hike. In their statement, the RBNZ also indicated that they considered a 75bps hike. The Committee agreed it remains appropriate to continue to tighten monetary conditions at a pace to maintain price stability and contribute to maximum sustainable employment.

“Some members highlighted that a larger increase in the OCR now would reduce the likelihood of a higher peak in the OCR being required," the Monetary Policy Committee said in its statement.

The Committee noted the recent fall in the kiwi dollar, stating, "Higher global interest rates and increased risk aversion in global markets have placed downward pressure on the New Zealand dollar," it said. "However, a lower New Zealand dollar, if sustained, poses further upside risk to inflation over the forecast horizon."

The Kiwi Dollar rose 0.15% against the Dollar after the news. In the wholesale interest rate market, the key two-year swap rate was unchanged at 4.48 per cent.

Source: NZ Herald

Japan services PMI increases to 52.2 as tourism demand expected to increase in October

Japan services PMI increased to 52.2 in September from 51.9 in the prior month. The composite CPI of manufacturing and services increased to 51 from 49.4 indicating modest growth in the country.

Prime Minister Fumio Kishida this week pledged to raise inbound tourism spending to more than 5 trillion yen ($34.52 billion) a year, hoping to benefit from windfalls brought by the yen's recent fall to a 24-year low against the dollar. Japan will also loosen its border policies from Tuesday next week, dropping a cap on daily arrivals among other rules. These factors are expected to boost the tourism sector in the country.

Source: Reuters

US Crude Stocks decline by 1.77M

API reported that weekly US crude stocks declined by 1.77M barrel (1.96M barrel gain expected) after a 4.1M barrel buildup last week. The API also reported a draw in gasoline inventories this week, of 3.474 million barrels, adding onto the previous week's 1.048 million-barrel draw. Distillate stocks rounded out the week’s draws with a loss of 4.046 million barrels compared to last week's 438,000-barrel increase.

The draw comes even as the Department of Energy released 6.2 million barrels from the Strategic Petroleum Reserves in the week ending September 30 that left the SPR with 416.4 million barrels.

Source: Oilprice

6th Oct 2022 (Thursday)

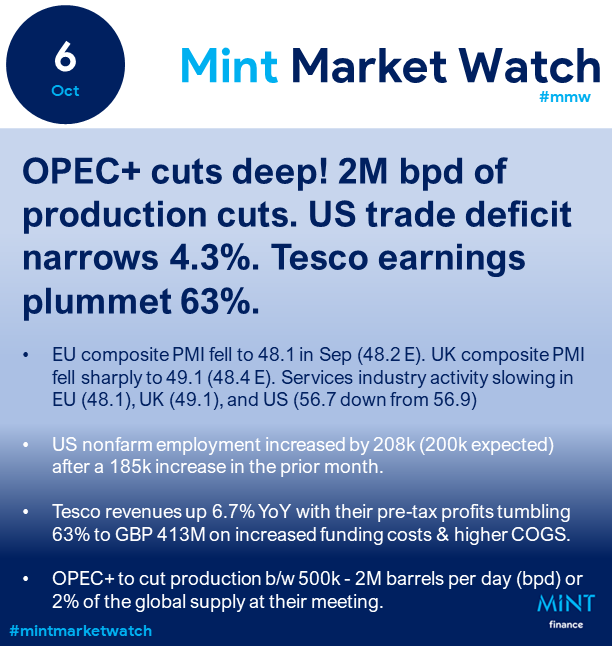

OPEC+ cuts deep! 2 million bpd of production cuts. Services contract in US, UK, & EU. US trade deficit narrows 4.3%. Tesco earnings plummet 63%.

EU composite PMI, which is a gauge for economic activity in the Euro Zone fell to 48.1 in September (48.2 E) from 48.9 in August. UK composite PMI fell sharply to 49.1 (48.4 E). Services industry activity slowing in EU (48.1), UK (49.1), and US (56.7 down from 56.9)

US nonfarm employment increased by 208k (200k expected) after a 185k increase in the prior month.

Tesco revenues of GBP32.46B (up 6.7% YoY) with their pre-tax profits tumbling 63% to GBP 413M on increased finance costs & higher COGS.

OPEC+ agreed to steep oil production cuts between 500k-2M barrels per day (bpd) or 2% of the global supply at their meeting.

OPEC+ to cut oil output by 2M bpd equivalent to 2% of global supply

OPEC+ agreed to steep oil production cuts between 500k-2M barrels per day (bpd) or 2% of the global supply at their meeting. They stated that the deep cuts were necessary to respond to rising interest rates in the West and a weaker global economy. Oil prices have dropped to about $90 from $120 three months ago on fears of a global economic recession, rising U.S. interest rates and a stronger dollar.

The production cuts are based on existing baseline figures, which means the cuts would be less deep because OPEC+ production fell about 3.6 million bpd short of its output target in August. Under-production has been an outcome of Western sanctions on countries such as Russia, Venezuela and Iran plus output problems with producers such as Nigeria and Angola.

Prince Abdulaziz said the real cuts would be 1.0-1.1 million bpd and would mainly come from Gulf OPEC producers such as Saudi Arabia, Iraq, the United Arab Emirates and Kuwait.

Biden called the decision shortsighted and accused OPEC+ of colluding with Russia. The White House said President Joe Biden would continue to assess whether to release further strategic oil stocks to lower prices.

US Crude inventories fell by 1.356M last week indicating higher demand. U.S. gasoline inventories fell more-than-expected by 4.7 million barrels, while distillate stockpiles, which include diesel and heating oil, also posted a larger-than-expected draw, falling by 3.4 million barrels.

Brent crude futures for December settlement edged down 8 cents to $93.29 per barrel by 0656 GMT after settling 1.7% higher in the previous session.

U.S. West Texas Intermediate (WTI) crude futures for November delivery slid 15 cents to $87.61 per barrel, building on a 1.4% rise on Tuesday.

Sources: Reuters, Investing, Reuters

German trade balance continues to narrow to 1.2B Euros

Germany’s trade balance narrowed to 1.2 Billion Euros (4.0B E) in August from 3.4 Billion Euros previously.

Stronger demand from the United States and China helped push exports to 133.1 billion euros ($132.59 billion) in August, up 1.6% from the previous month.

Imports also increased more than expected, rising 3.4% to 131.9 billion euros, the seventh month in a row of growth.

Source: Reuters

EU Composite PMI falls to 48.1 in September

EU composite PMI, which is a gauge for economic activity in the Euro Zone fell to 48.1 in September (48.2 E) from 48.9 in August. A reading below 50 indicates that economic activity in the country is contracting. Services PMI for the EU fell to 48.8 (48.9 E) from 49.8.

Services activity weakened in Germany, Italy and Spain, although in France while growth was weaker than a preliminary estimate it was faster than in August. Earlier this week, manufacturing PMI declined to 48.4 indicating falling demand as energy prices soar.

"We think some economies, including Germany, are already contracting and expect the euro zone as a whole to fall into recession in Q4." said Jessica Hinds at Capital Economics.

Source: Reuters

UK composite PMI falls to 49.1 in sharp drop

UK Services PMI declined to 50.0 in September (49.2 E) from 50.9 in August. The composite PMI fell to 49.1 (48.4 E) from 49.6. This means that overall business activity in the country is contracting.

Services companies that comprise the bulk of the private-sector economy were the least positive about the outlook since May 2020. New orders from both home and abroad declined, with survey respondents blaming Brexit and a weaker world economy, as well as subdued confidence and customers cutting costs.

Most of the PMI survey data was collected before Sept. 23, when new finance minister Kwarteng plunged markets into chaos with historic tax cuts and borrowing in his "mini-budget". The central bank was forced to intervene to stabilise UK bond markets.

Source: Reuters

US businesses added 208k jobs in September

ADP reported that US nonfarm employment increased by 208k (200k expected) after a (upwardly revised) 185k increase in the prior month. Annual pay increased 7.8% YoY. Those changing jobs saw a median change in annual pay of 15.7%, down from 16.2% in August. ADP’s report comes two days before the closely watched nonfarm payrolls report issued by the Bureau of Labor Statistics.

A big jump in trade, transportation, and utilities jobs of 147,000 was reported. Professional and business services added 57,000, while education and health services picked up 38,000 and leisure and hospitality grew by 31,000. There also were losers within the services sector, as information declined by 19,000 and financial activities saw a loss of 16,000 positions. Goods-producing industries reported a loss of 29,000 positions, with manufacturing down 13,000 and natural resources and mining losing 16,000.

Source: CNBC

US Services industry activity slows slightly as PMI drops to 56.7

ISM reported that US Services PMI dropped to 56.7 (56 E) in September from 56.9 in the prior month. A reading above 50 indicates expansion in the services sector, which accounts for more than two-thirds of U.S. economic activity.

The ISM report's measure of new orders received by services businesses slipped to 60.6 from 61.8 in August. The ISM report's services industry employment gauge shot up to 53.0 from a reading of 50.2 in August, suggesting job growth was likely solid in September. The ISM survey's measure of supplier deliveries fell to 53.9 from 54.5 in August indicating that transportation and warehousing industry are still facing shortages.

A survey from S&P Global showed service industry activity increasing in September as their PMI increased to 49.3 from 43.7.

Services activity is being supported by a shift in spending from goods. Fifteen industries, including mining, public administration, retail trade, information, and construction, reported growth. But accommodation and food services, arts, entertainment, and recreation, as well as transportation and warehousing reported a decline in activity.

Source: Reuters

US Trade Deficit narrows 4.3% to $67.4B

Trade Deficit narrowed again, decreasing 4.3% to $67.4B. This is the lowest level in more than a year. The smaller trade deficit could spur a rebound in GDP after it contracted at a 0.6% pace in the second quarter.

Imports declined 1.1% to $326.3 billion, likely driven by slowing demand and unsold goods. There were big declines in crude oil and capital goods imports. Motor vehicle imports, however, increased and were the highest on record. Imports of services rose, lifted by gains in travel and charges for the use of intellectual property. The real value of imports has dropped 19% (annualized) in the last 5 months.

Exports slipped 0.3% to $258.9 billion, also reflecting slowing demand in Europe and elsewhere. The decline in exports occurred almost across the board, with large decreases in non-monetary gold, crude oil and motor vehicles and parts. Exports of consumer goods increased, mostly reflecting pharmaceutical preparations, while exports of capital goods were the highest on record. Exports of services fell as gains in business and financial services were offset by a drop in travel.

With the dollar increasing nearly 10.7% from the start of the year, US manufactured goods are now becoming less competitive.

Source: Reuters

Canada building permits increase 11.9% in August

The total value of building permits in Canada increased 11.9% MoM in August to 12.5B CAD (-0.5% drop expected) after a 7.3% drop in July. Building permits provide an early indication of construction activity in Canada and are based on a survey of 2,400 municipalities, representing 95% of the country's population. The issuance of a permit doesn't guarantee that construction is imminent.

Construction intentions in the residential sector increased by 12% from the previous month to C$8.45 billion, as gains in Ontario offset losses posted in seven provinces. Construction intentions in the single-family homes component edged up 0.4%.

Construction intentions in the commercial component decreased 1.4%. Conversely, Manitoba saw notable growth in August due to a $50 million permit for an office building in Winnipeg.

Source: Marketwatch

Tesco profits decline 63% as costs increase

Tesco reported revenue of GBP32.46B, up 6.7% YoY. Their pre-tax profits declined 63% to 413M pounds on increased finance costs and higher cost of sales.

The company said that post-pandemic normalization has been compounded by cost-of-living-driven changes in customer behavior but said its solid business performance and acceleration of its Save to Invest program have led to a good first-half financial result.

Tesco slightly lowered its full year guidance, stating that they expect GBP2.4-2.5B in adjusted retail operating profit slightly down from April’s estimate of GBP2.4-2.6B. The Tesco Bank business is expected to deliver an adjusted operating profit of around GBP120 million to GBP160 million.

The company’s board declared an interim dividend of 3.85 pence a share, up from 3.20 pence a year earlier.

Tesco also said it intends to deliver its original three-year savings plan a year early, and it was targeting around GBP1 billion in cumulative savings by the end of February.

Source: Marketwatch

07th October 2022 (Friday)

EU Retail Sales fall 0.3%. German factory orders drop 2.4% MoM in Aug. Japan's Seven & I beats estimates. UK construction PMI up to 52.3.

UK Construction PMI, which gives a gauge into activity by construction firms, increased to 52.3 (48.0 E) in September.

EU retail sales fall 0.3% in August showing weakening consumer demand. German factory orders drop 2.4% in August, dragged by fall in orders from EU.

US initial jobless claims jump to 219k, boosted by Hurricane Fiona.

Japan's Seven & I holding’s, the parent of 7-Eleven stores delivered net profit (+28%) and revenue (+55%) increase in H1, forward guidance raised on strong overseas business

Levi Strauss reported EPS of 0.4 (0.37 E) on revenue of $1.52B ($1.6B E) up 1.3% YoY. It reported net income of $172.9M.

EU retail sales fall 0.3% in August showing weakening consumer demand

EU retail sales declined 0.3% MoM in August (0.4% decline expected) after a (revised down) 0.4% MoM decline in July. This marks a 2% (1.7% E) YoY drop in retail sales in the Eurozone.

The sales decline in August came despite a sharp rise in the volume of sales of car fuels during the holiday season, which rose 3.2% month-on-month and 5.1% year-on-year, but failed to offset falling sales of food and drinks and internet or mail order shopping.

Non-food retail sales overall did rise by 0.2% in August, although that was down 3.0% from a year earlier.

Source: Reuters

UK construction PMI jumps to 52.3 showing activity is growing again

UK construction PMI, which gives a gauge into activity by construction firms, increased to 52.3 (48.0 E) in September from 49.2 in August. This means that construction activity in the country is growing again. Still, construction firms said clients were slow, or reluctant, to sign off projects due to inflation concerns, squeezed budgets and worries about economic outlook.

However, other data in the report suggested that growth in the sector may be short lived.

New orders showed the weakest growth since May 2020. Business optimism hit the lowest since July 2020. Average cost burdens increased sharply in September, but the overall rate of inflation eased. Commercial work increased only marginally, and civil engineering activity fell for the third month in a row. Meanwhile, employment growth accelerated from August's 17-month low. Around 21% of the survey panel reported a rise in staffing levels, while only 8% signalled a decline. Supply shortages eased in September.

German factory orders drop 2.4% in August, dragged by fall in orders from EU

German factory orders dropped 2.4% MoM (0.7% decline expected) in August. Meanwhile, July’s reading was revised to show a growth of 1.9% compared to previous reading of 1.1% decline.

Domestic industrial orders fell by 3.4% and those from the euro zone by 3.8%. non-Eurozone foreign orders fell 0.4%. Disregarding volatile large-scale orders, manufacturing orders posted a 0.8% increase in August on the previous month.

Source: Reuters

ECB monetary policy meeting minutes show governing council as hawkish

Minutes from ECBs monetary policy meeting on 7-8th September showed that a 75bps rate hike was favored by a large number of governing council members who felt that this still left monetary policy expansionary.

The council felt that frontloading of rate hikes was necessary to bring the (at the time) neutral interest rate higher in order to fight inflation. Others felt that a 50bps rate hike was necessary as 75bps could unnecessarily worsen the pending economic downturn.

The council expects to raise rates further.

Source: Econostream

US initial jobless claims jump to 219k, boosted by Hurricane Fiona

US initial jobless claims increased 29k to 219k (203k E) from (revised down) 190k in the prior week. Unadjusted claims increased 13,264 to 167,083.

Some of the larger-than-expected jump in jobless claims reported by the Labor Department on Thursday was blamed on Hurricane Fiona, with filings surging in Puerto Rico, which was ravaged by the storm in the second half of September. Claims for Puerto Rico jumped 3,917, accounting for about 30% of applications. The archipelago normally makes up less than 1% of national claims.

Claims data in the coming weeks will likely be distorted by Hurricane Ian, which cut a swath of destruction across Florida and the Carolinas at the end of September.

Source: Reuters

Japan household spending slows in August as post-COVID boom fading

Japan household spending fell 1.7% MoM in August (0.2% increase expected) after falling 1.4% in July. This marks a 5.1% YoY increase in household spending (6.7% E). Average wages in the country grew 1.7% in August, but still lagged annual inflation, which grew at a 3% rate in August.

Spending in Japan has been increasing over the past year as COVID curbs start to be removed, however, that seems to be slowing with the rising inflation. The yearly reading for August was also boosted by a lower base-level as in August 2021, the government ramped up state of emergency restrictions to battle a resurgence of COVID cases.

Spending on items such as food and utilities grew steadily. But consumers were wary of spending on big purchases such as furniture and housing. Rising inflation and a weakening yen have weighed heavily on consumer sentiment, offsetting an initial boost after the Japanese government relaxed most COVID-linked curbs this year.

Seven and I holding’s net profit (+28%) and revenue (+55%) increase in H1, forward guidance raised on strong overseas business

Seven and I holdings reported Net Profit of 136.09B Yen ($940M) for H1 up 28% from H2 2021. For Q2, Net Profit was 71.05B Yen (68.81B Yen expected). H1 revenue increased 55% to 5.652T Yen. Q2 revenue was 3.2T Yen up 31% from Q1 but below analyst estimates of 3.246T Yen.

First-half operating profit from its Japan convenience-store business rose 2.7% to 126.71 billion Yen, while that of its overseas convenience-store business more than doubled to 115.60 billion Yen from 57.20 billion Yen a year earlier. The 7-Eleven operator said retail gas prices have risen sharply due to higher crude-oil prices, helping boost earnings at its overseas convenience-store business. Its department store and speciality store business posted a first-half operating profit of 465 million Yen, compared with an operating loss of 7.77 billion Yen a year earlier.

Seven & i raised its revenue and net profit forecasts for the fiscal year ending February, thanks partly to stronger earnings from its overseas convenience-store business. It now expects revenue to rise 33% to Y11.646 trillion and net profit to climb 25% to Y264.00 billion.

Source: Marketwatch

Constellation brands beats earnings estimates with higher sales but cut EPS outlook

Constellation brands reported EPS of 3.17 (2.78 E) on revenue of 2.66B (2.5B E) up 12% YoY. The company posted a net loss of $1.151 billion, or $6.30 a share in the quarter vs $1.5M or 1 cent per share a year ago. The net loss included one-time items such as losses in cannabis venture Canopy which booked an impairment charge of $1.06B.

The company said its beer business achieved double-digit sales, driven by Modelo Especial and Corona Extra which grew 15% YoY. The wine and spirits business saw growth driven by U.S. shipment volume growth and a strong performance by fine wine and craft spirts in international markets.

Despite the higher performance in the quarter, the company lowered its EPS outlook. They now expect $0.75 to $1.15 per share compared to previous report of $11.15 to $11.45 per share. Net sales are expected to grow 8-10% to $7.42B. Operating income is also expected to increase 3-5%. The company's wine and spirits division is expected to see a sales decline of up to 2% (down to $2B).

The board declared a quarterly cash dividend of 80 cents a share. Constellation Brands also said it has agreed to sell to the Wine Group LLC some of its mainstream and premium wine brands, including "Cooper & Thief" and "the Dreaming Tree," as it shifts its strategy toward fine wine brands and craft spirits.

Sources: Marketwatch, Marketwatch, Marketwatch

McCormick profits and sales rise on higher prices

McCormick reported EPS of 0.69 (0.71 E) on revenue of $1.6B ($1.63B E) up 3% YoY. They posted a profit of $222M or $0.82 per share up 4.7% YoY. The profit included one-time items such as after-tax gain on the sale of its Kitchen Basics business in August 2022.

Gains were seen in the consumer-business unit and the flavors division, as the company sought to recover cost inflation that had been outpacing its price increases. Cost of sales increased more than sales, rising 8.3% to $1.03 billion, to knock gross margin down to 35.5% from 38.7%.

Sales were up 6% on a constant currency basis, reflecting 10% growth from higher prices. Higher sales were partially offset by declining volume and product mix, Kitchen Basics divestiture, withdrawal from low-margin India business and Russia.

The company reaffirmed previous forward guidance.

Sources: Marketwatch, Marketwatch

Levi Strauss cuts annual guidance as economic fears grow

Levi Strauss reported EPS of 0.4 (0.37 E) on revenue of $1.52B ($1.6B E) up 1.3% YoY. It reported net income of $172.9M.

After missing sales estimates, the company reduced annual forecast for revenue and earnings stating that the reduction was a result of the significant incremental currency headwinds from the stronger U.S. dollar, as well as a more cautious outlook for North America and Europe due to macroeconomic conditions and ongoing supply chain disruptions.

Executives now expect annual adjusted earnings of $1.44 to $1.49 per share down from $1.5 to $1.56 previously. Revenue is expected between $6.15 to $6.17 down from previous estimate of $6.4 to $6.5.

Shares fell between 4.5% and 5% in after-hours trading following the announcement, after closing with a 3.9% decline at $15.93.

Source: Marketwatch

08th Oct 2022 (Saturday)

US Non-Farm Payrolls rise 263k (250k E). Hourly earnings rise 0.3% MoM. Oil price jumps 4% on OPEC+ cuts as $100 in sight.

US Non-Farm Payrolls rise by 263k, unemployment rate drops to 3.5% while average hourly earnings rise 0.3% MoM. Strong labor market in the US leaves more room for the Fed to hike interest rates.

Oil price jumps 4% on the back of OPEC+ supply cuts. Brent futures up 3.7% to $97.92. WTI crude rose 4.7% to $92.64.

German industrial production declines 0.8% in August

UK labor market shows signs of slowing demand for workers.

German industrial production declines 0.8% in August

Germany’s industrial output declined 0.8% MoM in August (decline of 0.5% expected). In the energy-intensive industrial branches, production fell by 2.1% in August 2022 compared with the previous month—a much steeper drop than the overall industrial production decline.

Apart from the high energy prices, which have forced energy-intensive industries to curtail production or shut down factories, industrial production in Germany is still affected by the extreme shortage of intermediate products, the statistics office said.

Source: Oilprice

UK labor market shows signs of slowing demand for workers

A survey from KPMG and REC showed that UK businesses are being more cautious when it comes to hiring with worsening economic conditions. Overall vacancy growth softened for the sixth month in a row in September, to mark the slowest rise in demand for staff since February 2021.

“Some employers, even those who anticipate that the recession may be short, are taking steps now to contain costs, including hiring freezes,” Claire Warnes, head of education, skills and productivity at KPMG UK, said.

Meanwhile, labor productivity in the UK increased 0.3% in Q2 in the UK slowing from a 1.2% increase in Q1.

Source: Yahoo

US Non-Farm Payrolls rise by 263k, unemployment rate drops to 3.5%

Non-Farm Payrolls in the US increased by 263k in September (250k expected) after increasing by 315k in August. Unemployment rate dropped to 3.5% from 3.7%. The labor force participation rate dropped from 62.4% to 62.3% this represents a 57k drop in the labor force. A more encompassing measure that includes discouraged workers and those holding part-time jobs for economic reasons saw an even sharper decline, to 6.7% from 7%. Average hourly earnings rose 0.3% MoM up 5% YoY.

Leisure and hospitality led the gains with an increase of 83,000, still 1.1 million jobs short of its February 2020 pre-pandemic levels. Health care added 60,000, professional and business services rose 46,000 and manufacturing contributed 22,000. Construction was up 19,000 and wholesale trade climbed 11,000. Government jobs decreased 25k while financial activities and transportation and warehousing both saw losses of 8,000 jobs.

Overall, the job report showed that the US labor market was still strong which leaves room for the Federal Reserve to hike interest rates further. This also reduced hopes for a 50bps rate hike in the next meeting. U.S. dollar index (DXY) which measures the USD against a basket of currencies was last up 0.6% and hit its highest level in a week. The index is up about 18% for the year so far. GBP dropped 0.9% after dropping 1.4% overnight. Offshore Yuan weakened 0.7%, the Euro weakened 0.6% and the Yen weakened 0.2%.

Oil price jumps 4% on the back of OPEC+ supply cuts

Oil prices jumped 4% to a 5-week high on the back of OPEC+’s decision to cut production by 2M bpd. Brent futures rose $3.50, or 3.7%, to settle at $97.92 a barrel, while U.S. West Texas Intermediate (WTI) crude rose $4.19, or 4.7%, to end at $92.64. U.S. heating oil futures jumped 19% this week to their highest close since June, boosting the heating oil crack spread - a measure of refining profit margins - to its highest close on record.

The OPEC+ cut comes ahead of a European Union embargo on Russian oil and will squeeze supply in an already tight market. US Oil rig count dropped by 2 to 602 this week signaling production shortages in the future.

Source: Reuters