Mint Macro Review - Issue 3

Mint Macro Review - Issue 3

Week ending 27th Aug 22 | #mmr

More and sharp equity market correction in the near term? Why, what gives?

Fed asserts its determination to fight inflation. Quantitative Tightening (QT) of $90B starts next month. Strong USD is hurting consumers globally & eventually corporate earnings.

Drought in many parts of the world (mainly in Europe and China) harming supply chain, restricting electricity supply and spiking electricity costs. Chinese macro economy points to broad based weakness chiefly in its property sector. Expensive mortgage & utility bills hurting consumers while obliterating discretionary spend. Savings rates at historical low levels.

Read Mint Disclaimer

Executive Summary

Powell takes hawkish stance at Jackson Hole symposium, committing to rate hikes until inflation reaches target levels (read more)

JPMorgan considers adding India debt to flagship index (read more)

US GDP fell less than previously thought in Q2 with jobless claims falling mildly reaching a 1 month low and pointing to tight labor market (read more)

US New Home Sales drop 12.6% even as prices remain high (read more)

China pumps a trillion yuan ($146 billion) in economic stimulus to assist infrastructure, property and private businesses (read more)

China's Fragile Economy Is Being Hammered by Driest Riverbeds Since 1865 (read more)

Euro falls below USD parity again as EU business activity contracts on cost-of-living crisis and supply constraints (read more)

Pandemic & War led turmoil seeding a new Macro Super Cycle tilting power from capital to labor (read more)

Nvidia misses earnings estimates lowers guidance for Q3 while Sales Force beats estimates but trims guidance (read more)

Julian Robertson aged 90 dies leaving a legacy of more than 200 cub hedge funds (read more)

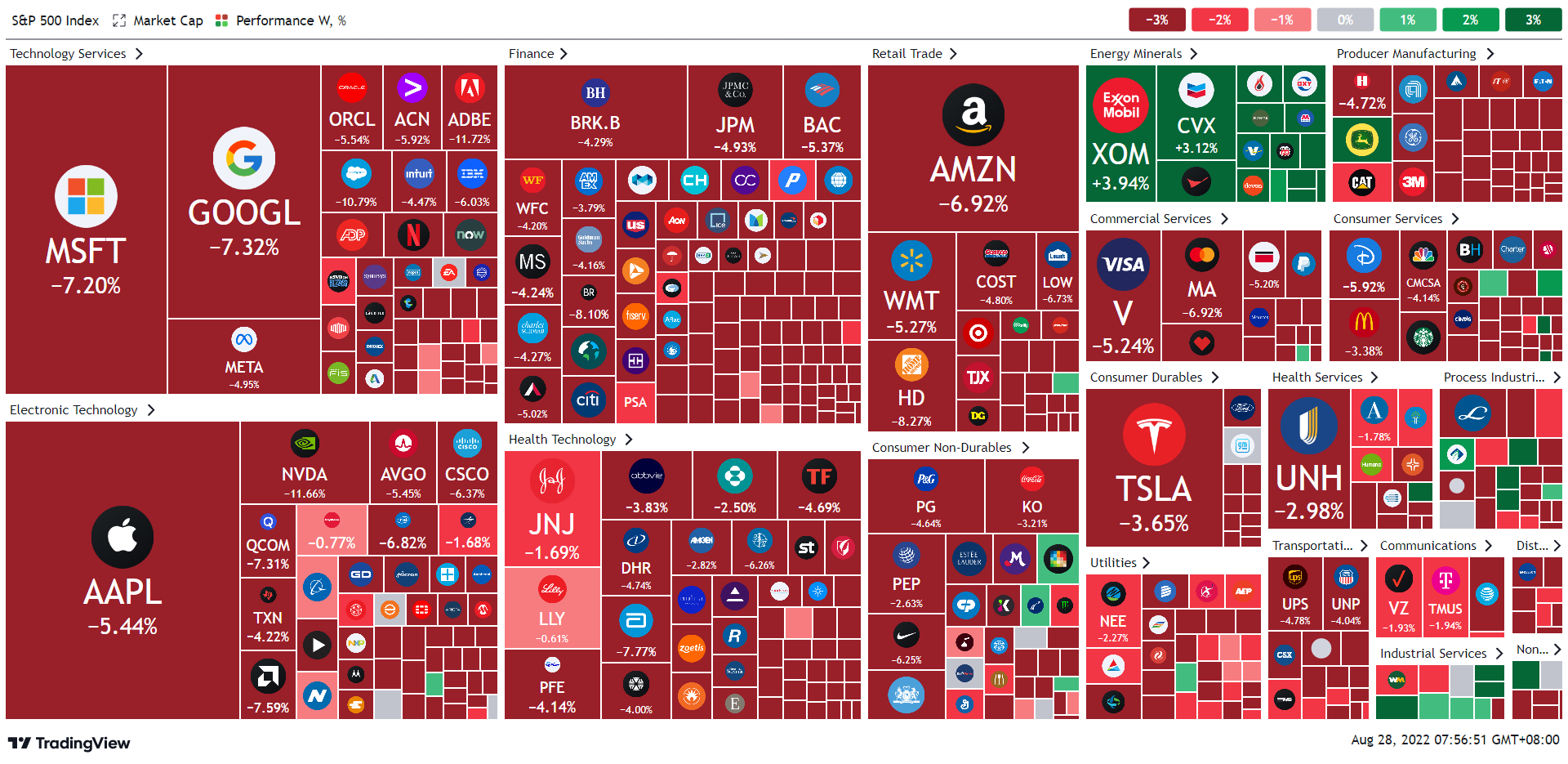

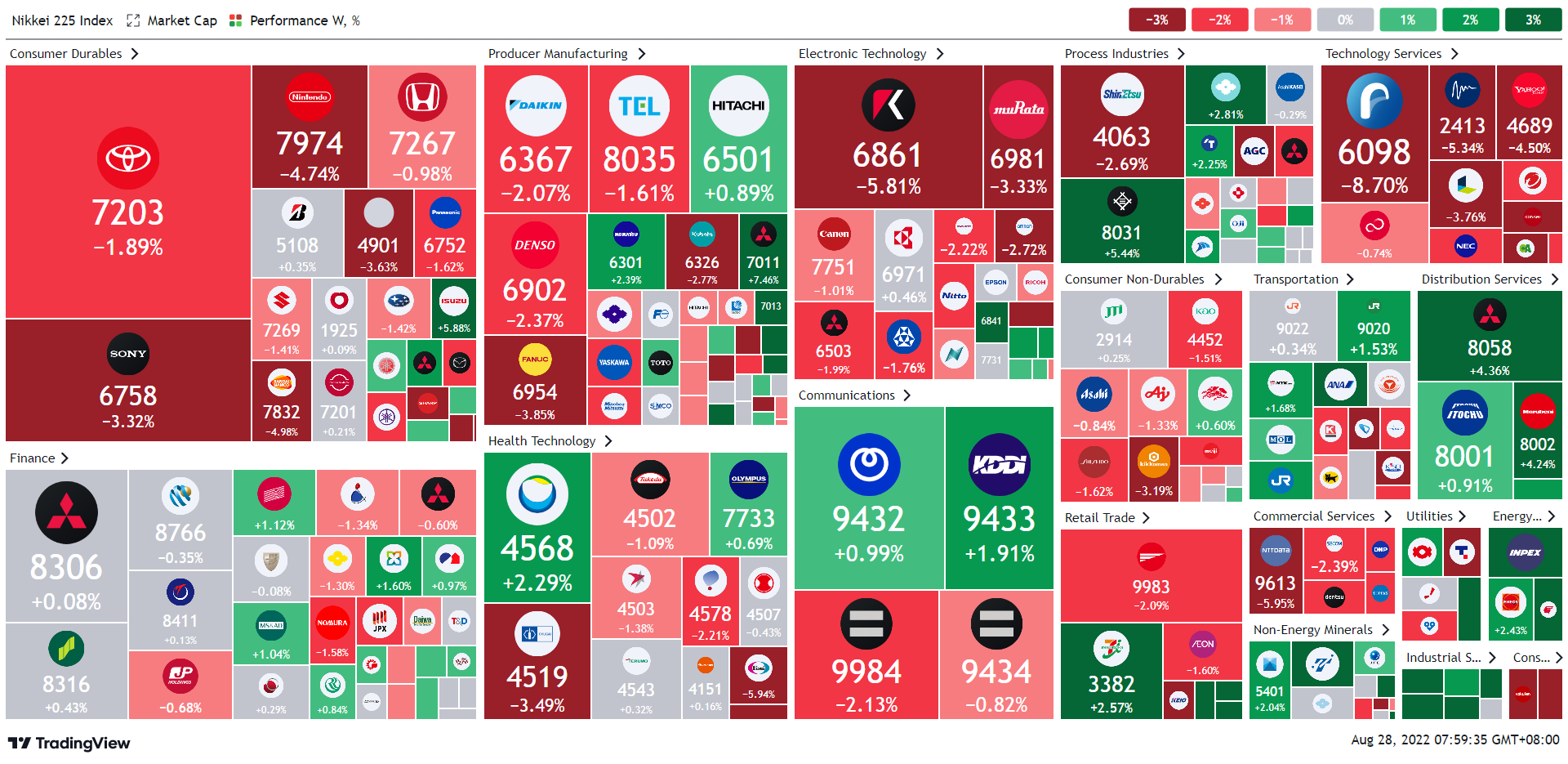

Equity Market Weekly Returns (S&P500, Nikkei225 & Nifty50)

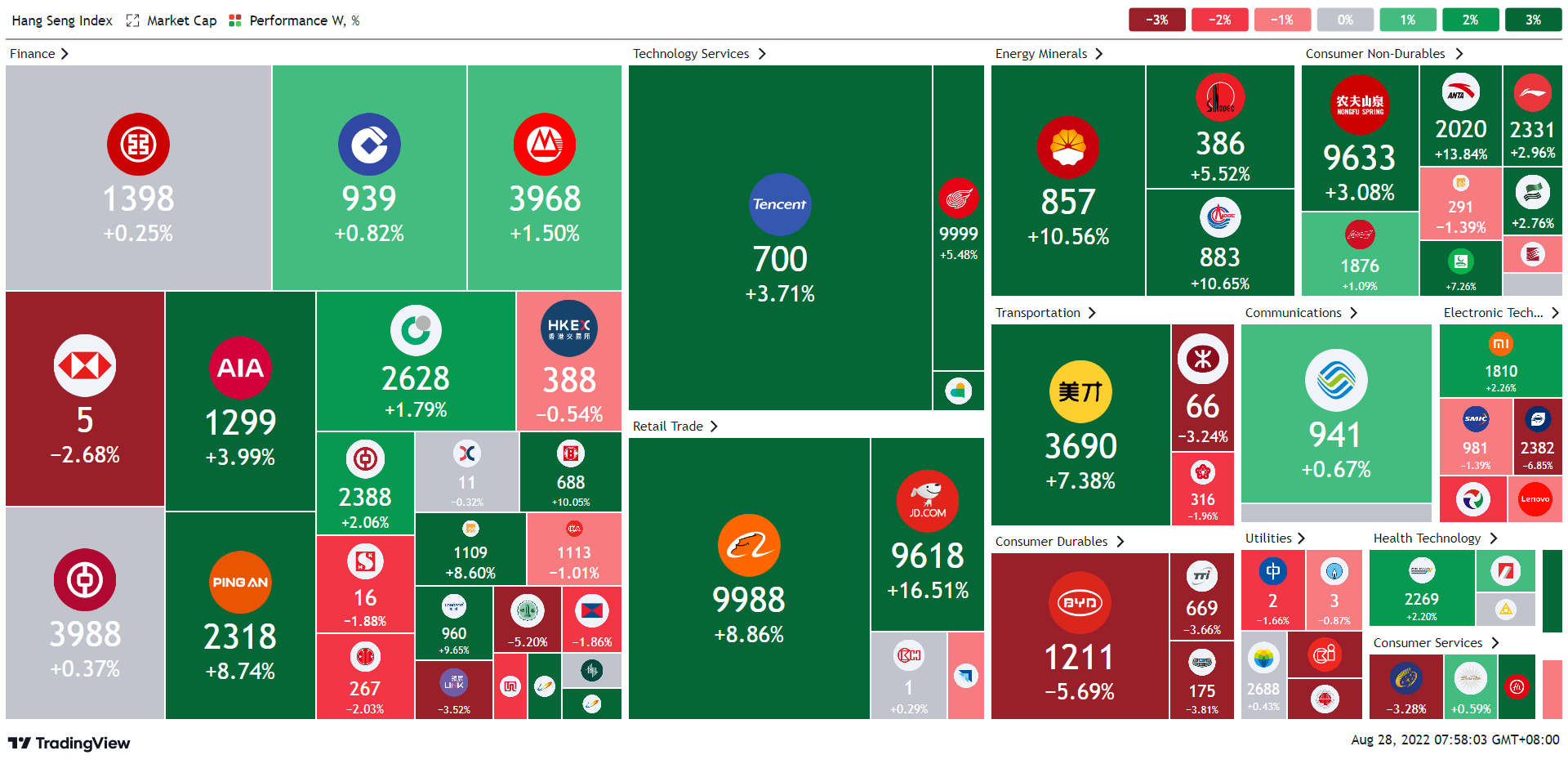

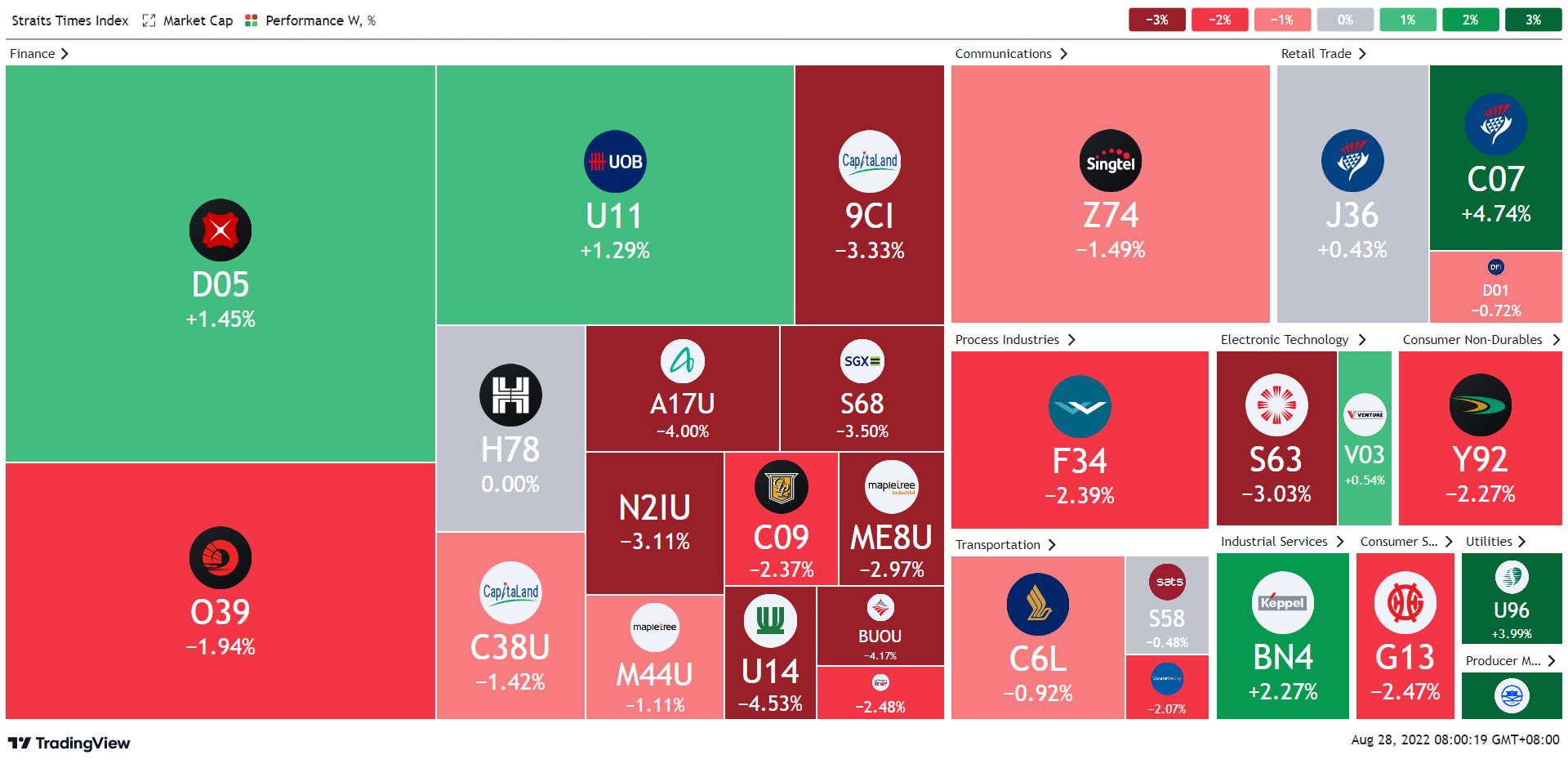

Click here to see heatmaps of equity markets in Nasdq100, Hong Kong, Singapore, and Taiwan.

Powell takes hawkish stance at Jackson Hole symposium, committing to rate hikes until inflation reaches target levels

Jerome Powell stated that Federal Reserves will continue with rate hikes until inflation reaches target level of 2% from its reported level of 8.5% according to CPI or 6.3% according to the PCE Price Index.

Powell said that the U.S. economy will need tight monetary policy "for some time" before inflation is under control. That means slower growth, a weaker job market and "some pain" for households and businesses. (Reuters)

2.25% is the total rate increase from four consecutive hikes

Fed has instituted four consecutive rate hikes totaling 2.25%. Investors are anticipating a 0.5% or 0.75% rate hike next month when the Fed meets on 20/Sep. (CNBC)

Recent economic data which suggested that inflation had peaked had led some investors to believe that the central bank could be more lenient with rate hikes. However, the stance taken by Fed Chair sent clear message that rate hikes would not be shifted to rate cuts until target inflation levels are reached, stating “The historical record cautions strongly against prematurely loosening policy”. (Reuters, CNBC)

Markets reacted negatively to the news, with the S&P 500 down 3.37%, the DJI down 3.03% and NASDAQ 100 down 4.1%.

Source: Reuters, CNBC, Federal Reserve

Return to Executive Summary

JPMorgan considers adding India debt to flagship index

RBI introduced fully accessible route bonds in March 2020, allowing foreign financial institutions to invest in rupee-denominated bonds without restrictions.

USD 30 Billion is the estimated fund inflows into India from inclusion into JPM’s bond index

Benchmark inclusion would drive an estimated $30bn in passive investor inflows according to Goldman Sachs.

JPMorgan is sounding out big investors on adding India to its emerging markets bond index as the country’s domestic market opens up to foreign capital.

The Wall Street bank was seeking investor views on whether to make a large chunk of India’s $1tn rupee-dominated bond market eligible for inclusion in the GBI-EM Global Diversified index of local currency debt.

The JPMorgan consultation should be complete by next month, with the announcement of an official proposal expected in October.

India is not included in most other bond indices, such as Bloomberg’s Global Aggregate index or the FTSE Emerging Markets Bond index.

FTSE Russell placed New Delhi’s bonds on a watchlist for possible inclusion in early 2021 but said in March that the status remained unchanged, though it is scheduled for another assessment next month. FTSE Russell declined to comment.

One of the stumbling blocks to drives for inclusion has been where and how trading should be settled, whether outside India’s borders on a platform such as Euroclear that is familiar to financial institutions, or in India, where investors would have to complete onerous registration procedures.

Source: FT

Return to Executive Summary

US GDP fell less than previously thought in Q2 with jobless claims falling mildly reaching a 1 month low and pointing to tight labor market

U.S. gross domestic product contracted at a 0.6% annual rate from April to June, compared with an initial estimate of a 0.9% decline. (WSJ)

One factor was an upward revision of consumer spending, which accounts for the bulk of economic output. (WSJ)

Brian Bethune, an economist at Boston College, said that the economy paused in the first half of 2022, but the solid labor market means it didn’t dip into a recession. (WSJ)

The number of people who applied for unemployment benefits last week fell to a one-month low of 243,000, indicating layoffs remain near record lows and that a tight labor market is keeping the U.S. economy moving forward. (Marketwatch)

New jobless claims fell by 2,000 from a revised 245,000 (initially 250,000) in the prior week. (Marketwatch)

1.42 million is the number of people collecting unemployment benefits and remains at a near 50-year low

The number of people already collecting unemployment benefits declined by 19,000 to 1.42 million. They remain near a 50-year low. (Marketwatch)

Continuing claims, a proxy for the number of people receiving government unemployment payments, decreased by 19,000 to 1.42 million (WSJ)

Source: WSJ, MarketWatch, WSJ

Return to Executive Summary

US New Home Sales drop 12.6% even as prices remain high

Sales of new U.S. single-family homes plunged 12.6% to 511k units in July as persistently high mortgage rates and house prices further eroded affordability. The drop was 10% higher than expected (Reuters)

The housing market has been the sector hardest hit by the aggressive interest rate increases delivered by the Federal Reserve to tame inflation (Reuters)

Despite slowing demand, house price growth remains strong. The median new house price in July was $439,400, an 8.2% jump from a year ago. (Reuters)

At the current sales pace, it would take 10.9 months to exhaust the supply of new homes in the US, the most since 2009 and nearly double the figure at the start of this year.

Removing seasonal adjustments to the data, the amount of time rises to 11.2 months. Sales of new US homes fell in July to the slowest pace since early 2016 as high borrowing costs and elevated prices weaken demand.

Source: James Wong, Reuters

Return to Executive Summary

China pumps a trillion yuan ($146 billion) in economic stimulus to assist infrastructure, property and private businesses

Just a day after China’s central bank reiterated that it was sticking to its policy of limited stimulus measures, policy makers surprised observers by announcing a packet of 1 trillion yuan — the equivalent of $146 billion — in pro-growth measures.

The new initiative, issued by the State Council — China’s cabinet — centers around 19 measures that emerged from a meeting late Wednesday chaired by Premier Li Keqiang.

Among the allowances, state policy banks were given an additional 300 billion yuan ($44 billion) focused mainly on financing infrastructure projects. Local governments were given the green light to use more than 500 billion yuan ($73 billion) of existing special bond quotas and were promised reduced financing costs through interest-rate changes.

Amid an energy crisis sparked by severe droughts and heat waves, the cabinet said central-government-run electricity firms will be allowed to sell 200 billion yuan ($29 billion) in special debt to ensure adequate energy supply.

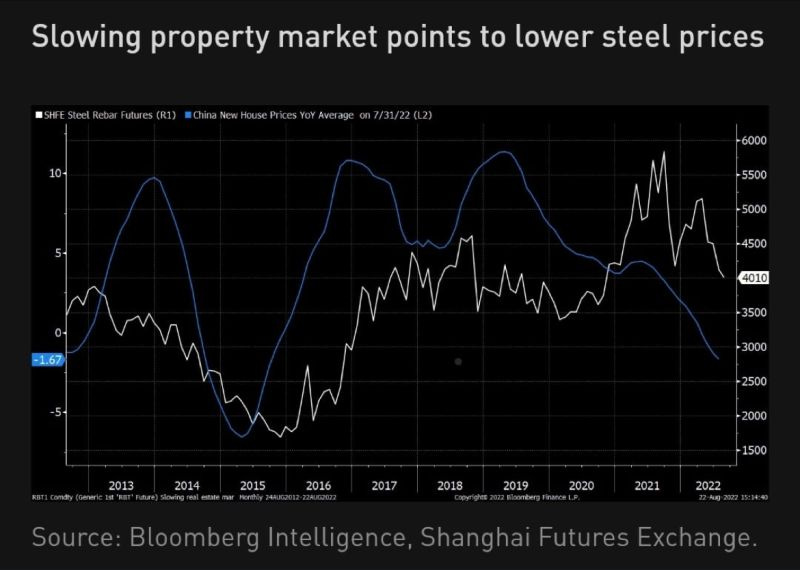

As reported on BloombergNEF, Steel prices weaken as China’s economy cools. Real estate crisis puts strain on demand for steel rebar. Producers expect weak demand as mill utilization remains low. Prices of Shanghai-traded steel rebar futures, already more than 20% off their year-to-date highs, look set to extend declines as the fundamental outlook worsens for the once-hot commodity primarily used in infrastructure construction.

Source: MarketWatch

Return to Executive Summary

China's Fragile Economy Is Being Hammered by Driest Riverbeds Since 1865

An extreme summer has taken a toll on Asia’s longest river, which flows about 3,900 miles (6,300 kilometers) through China and feeds farms that provide much of the country’s food and massive hydroelectric stations, including the Three Gorges Dam — the world’s biggest power plant.

157 years - Yangtze - Asia’s longest river is at its lowest since records began in 1865

A year ago, water lapped almost as high as the riverbank where Wan swims. Now, the level is at the lowest for this time of year since records began in 1865, exposing swathes of sand, rock and oozing brown mud that reeks of rotting fish.

“And it keeps going down,” said Wan, who last week needed to descend almost 100 steps — usually hidden beneath the water-line — to cool off on a sweltering 40-degree-Celsius (104 degrees Fahrenheit) day.

Factories shut down as extreme heatwave strains energy grids. Sichuan is hardest hit as hydropower output slashed by half.

Yangtze’s retreating water levels have snarled electricity generation at many key hydropower plants, sparking energy chaos across parts of the country. Mega cities including Shanghai are turning off lights, escalators and cutting back on air conditioning.

Tesla Inc. has warned of disruptions in the supply chain for its Shanghai plant, and others such as Toyota Motor Corp. and Contemporary Amperex Technology Co., the world’s top maker of batteries for electric vehicles, have shuttered factories.

Source: Bloomberg

Return to Executive Summary

Euro falls below USD parity again as EU business activity contracts on cost-of-living crisis and supply constraints

EU Manufacturing PMI fell from 49.8 to 49.7 in August while the Services PMI fell from 51.2 to 50.2 Composite PMI also declined from 49.9 to 49.2, an 18-month low. The decline can be associated to curtailed spending due to a cost-of-living crisis and supply constraints that hurt manufacturers.

According to S&P Global, the decline in business activity was centered in Germany, which posted the sharpest decline in output since June 2020. Outside of Germany and to a lesser extent France, output did increase, but marginally. (Marketwatch)

13% is the extent to which Euro has weakened relative to USD so far this year

The EURUSD on Monday fell back below parity against the dollar and has dropped 13% this year. (Marketwatch)

Mark Cus Babic, an economist at Barclays, said the data is consistent with the bank’s prediction of a eurozone recession in the second half of the year. He noted that tourism and the already weak position of manufacturing limited the decline. “Once the summer tourism tailwind fades, the euro area services PMI is likely to move to contractionary territory as well,” he said. (Marketwatch)

Source: MarketWatch

Return to Executive Summary

Pandemic & War led turmoil seeding a new Macro Super Cycle tilting power from capital to labor

Existing worker shortages combined with deglobalization and easier fiscal policies plus population aging will lead to structural labor shortages. Consequently, this will tilt the balance of power away from capital for the first time since the early 1980s is the key takeaway from Octavian Adrian Tanase.

Octavian derives these observation from TS Lombard's - The New Macro Super Cycle - report authored by Dario Perkins. In this report, Mr Perkins argues that:

Inflation/recession pendulum continues to swing, and offers no clarity for investors over the next 3-6 months.

The macro super cycle reflects the balance of power between labour and capital. That balance of power is starting to shift, for the first time since the 1980s.

Like other historic events, COVID-19 and the war in Ukraine will mark a secular turning point in global inflation and interest rates.

Central banks cannot stand in the way of this super-cycle, even if they are willing to cause a recession.

The underlying task of monetary policy is shifting. The implications for financial markets are profound (and not necessarily bearish).

Source: TS Lombard

Return to Executive Summary

Nvidia misses earnings estimates lowers guidance for Q3 while Sales Force beats expectations but trims guidance

Nvidia reported EPS of 0.51 (0.52 E) on revenue of 6.7B (6.83B E). Q3 revenue projections were $5.9 billion in the quarter, lower than expectations of $6.9 billion. (Yahoo)

“We are navigating our supply chain transitions in a challenging macro environment and we will get through this,” Nvidia founder and CEO Jensen Huang (Yahoo)

-33% and -44%; Gaming segment revenue dropped 33% YoY and 44% QoQ

According to the company's numbers, gaming segment revenue dropped an eye-watering 33% year-over-year and 44% quarter-over-quarter. Revenue was also hurt by 12.6% decline in PC sales. (Yahoo)

Nvidia said its data center business grew 61% in the quarter. The data center segment is Nvidia's main growth engine. (Yahoo)

Meanwhile, Salesforce reported EPS of 1.19 (1.03 expected) on revenue of 7.72B (7.7B expected). Salesforce instituted its first major share-repurchase plan, committing $10 billion to buying its own stock. (Marketwatch)

Salesforce executives lowered guidance for Q3 with adjusted earnings of $1.20-$1.21 a share on sales of $7.82B-$7.83B ($1.28 per share on revenue of $8.07B was expected by analysts on average). Q3 will also include the annual Dreamforce conference in September — a major revenue driver for the company. (Marketwatch)

Source: Yahoo, MarketWatch

Return to Executive Summary

Julian Robertson aged 90 dies leaving a legacy of almost 200 cub hedge funds

Julian Robertson took a deceptively simple approach to investing: own the best companies and bet against the worst ones.

Robertson, who has died aged 90, was an investment industry giant who spawned a dynasty of hedge fund managers known as the “Tiger cubs”. Almost 200 hedge funds can trace their origins back to Tiger Management, including Bill Hwang’s Archegos Capital Management, which blew up in 2021.

6am sharp, Robertson rang the trading desk to check in on performance

Aged 48, he co-founded Tiger, named after his tendency to call people “Tiger” when he could not remember their name. Every morning at 6am sharp, Robertson rang the trading desk to check in on performance.

As Tiger grew, it expanded beyond its core expertise in US equities into government bonds, commodities & currencies. His refusal to embrace the dotcom boom cost the fund a fifth of its value in 1999. Robertson was ultimately right about the dotcom bubble. But it was too late for Tiger.

After losses and a slump in assets, the hedge fund finally returned outside investor money in 2000. Its charismatic founder was living proof that in the stock markets, being early is the same as being wrong.

Source: FT

Return to Executive Summary

Equity Market Weekly Returns (Others)

Disclaimer

Mint Macro Review is for informational purposes only and does not constitute financial, investment, risk management, accounting, or tax advice. Nothing stated in this document is to be construed as a recommendation, solicitation, endorsement or offer to buy or to deal in any financial products.

Trading and investment in any financial products are exposed to risk. There are no such thing as risk-free returns. This material has been published for general education purposes only. It does not address specific investment or risk management objectives, financial situation, or needs of any person.

Advice should be sought from a financial advisor regarding the suitability of any investment or risk management product before investing or adopting any investment or hedging strategies. Past performance is not indicative of future performance.