Mint Macro Review - Issue 4

Mint Macro Review - Issue 4

#mmr | 28/Aug to 03/Sep

125 years of history point to September being the weakest month in US equity market returns. Will 2022 be any different? Time will tell.

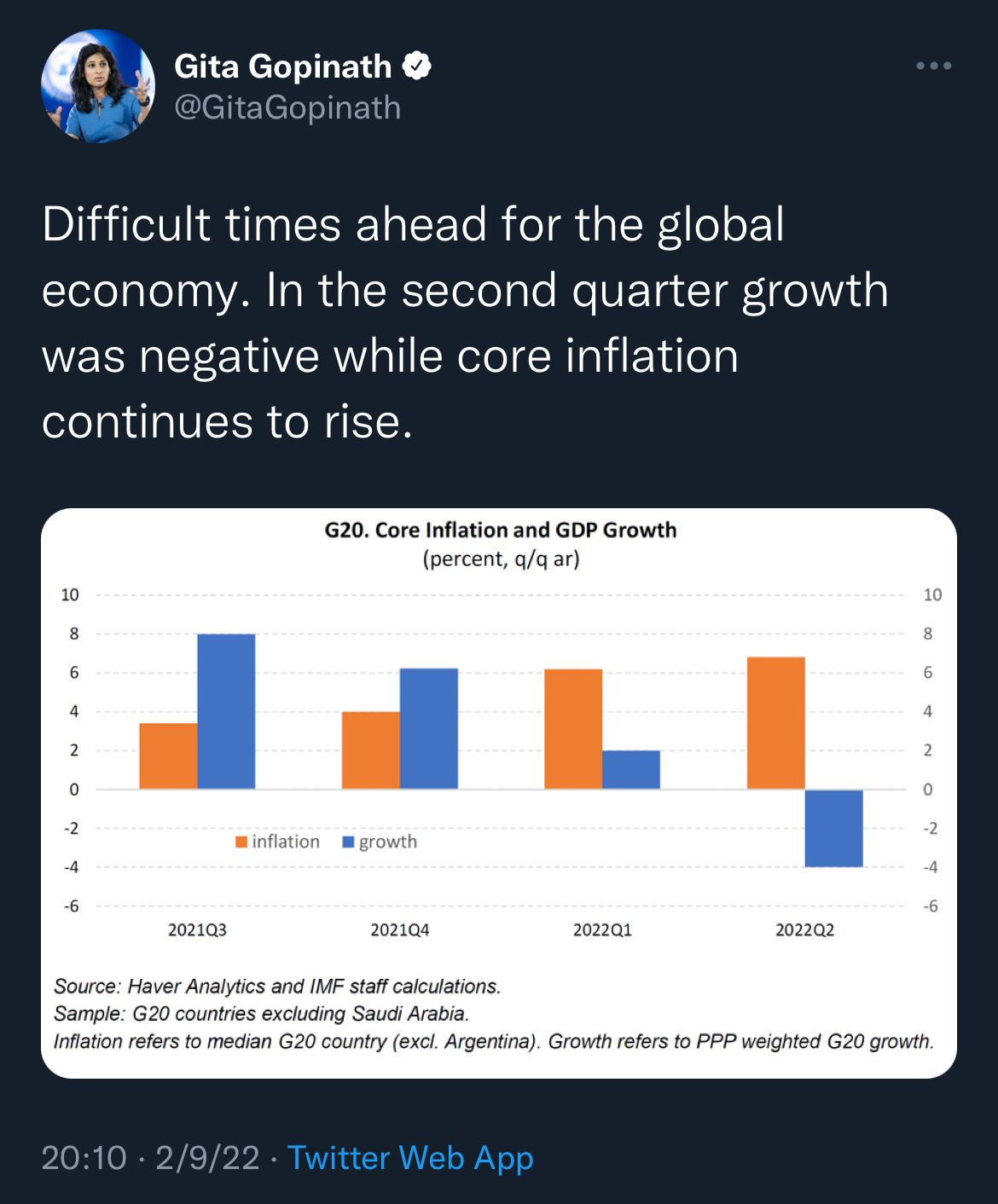

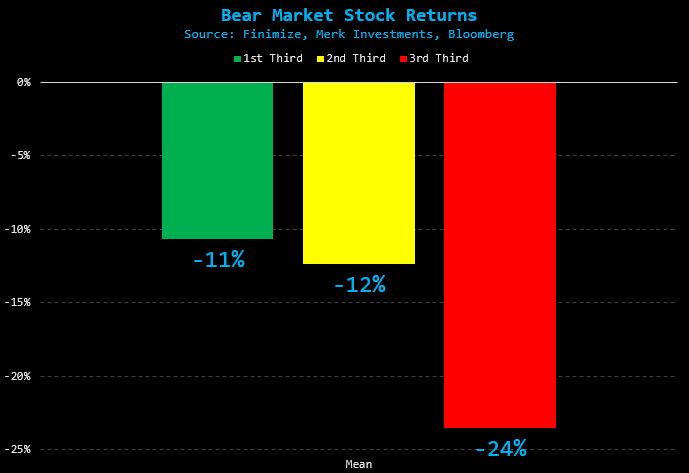

Brutal Bears: Research shows that bear markets play out in phases. Which phase the current bear market is in, is anybody’s guess. What’s more important is to note that final third phase of each bear market is 2X more painful than the first two. Average losses of 24% has been observed in the last 16 bear markets. Risk manage your portfolio as we journey through.

Record Setting Yen: Japanese Yen is setting records on rising carry trades. Being the only zero-yielding currency, carry trades across multiple pairs continues to rise amplifying downward pressure.

Unprecedented Dominance: Apple to launch new models of its existing products on 7/Sep. Apple continues to conquer market-share and now enjoys unprecedented dominance.

Singapore - Asia’s Default Wealth Centre: Growing affluence, Newly minted billionaires, Crackdown on ultra-rich, Covid restrictions continue to cement Singapore as Asia’s wealth center.

Read Mint Disclaimer

Previous issues - Issue 1, Issue 2, Issue 3.

Executive Summary

Apple’s new product launch on 7/Sep against the backdrop of dominant market share (>50%) for its phones. (read more)

India sets its eyes on semiconductor manufacturing & targets to quadruple electronics industry to $300B by 2026. (read more)

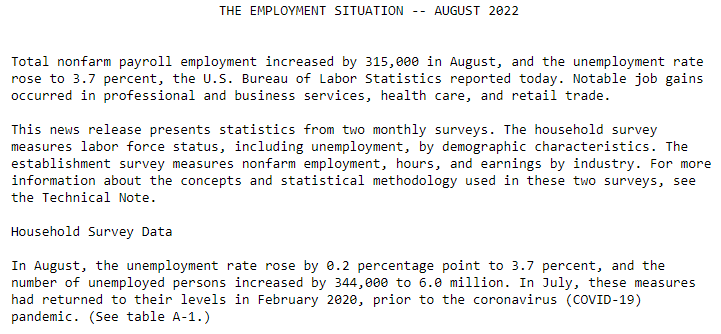

US Non-farm payrolls increase by 315k; unemployment rate increases to 3.7%. Labor market shows signs of cooling. (read more)

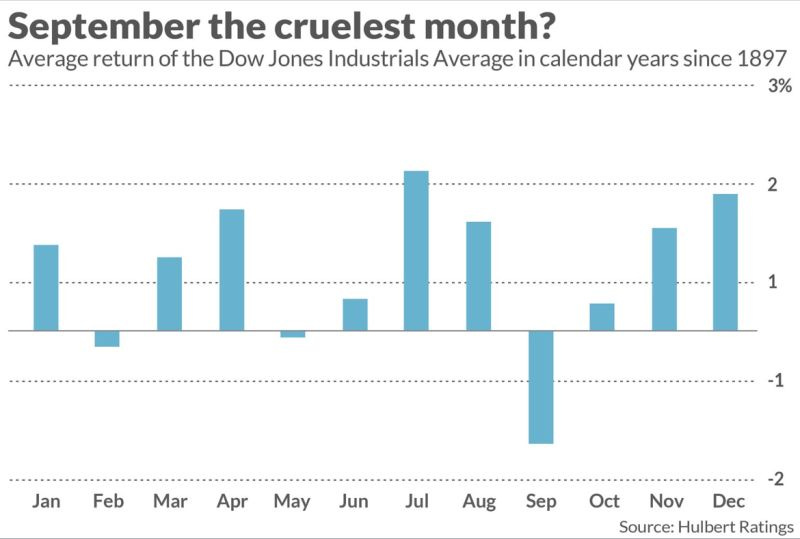

September has the notorious reputation of being the worst month for stock returns. Reason remains mysteriously unknown. (read more)

Growing affluence, Newly minted billionaires, Crackdown on ultra-rich, Covid restrictions continue to cement Singapore as Asia’s wealth center. (read more)

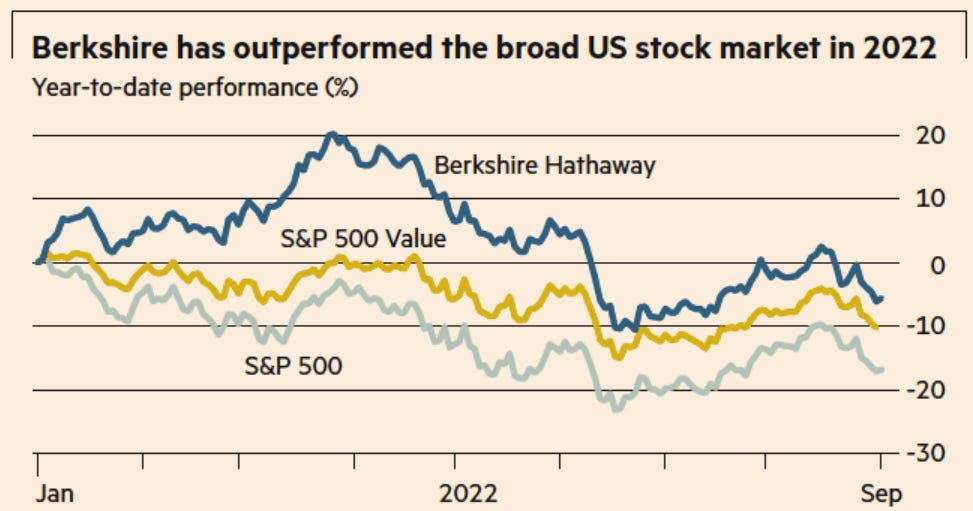

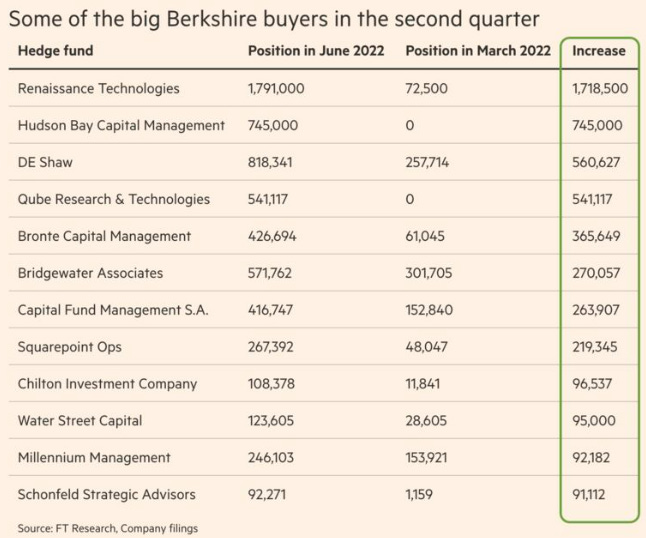

Quant Hedge Funds pile into Warren Buffet’s Berkshire Hathaway. (read more)

Yen's decline accelerating as it trades past 140 to the dollar. (read more)

Even as markets have corrected massively, more pain in store remains if history of bear markets were to repeat. (read more)

BYD net income triples in H1 to 3.6B Yuan ($521M) with record output and sales. (read more)

Collectibles may offer hedge against inflation. (read more)

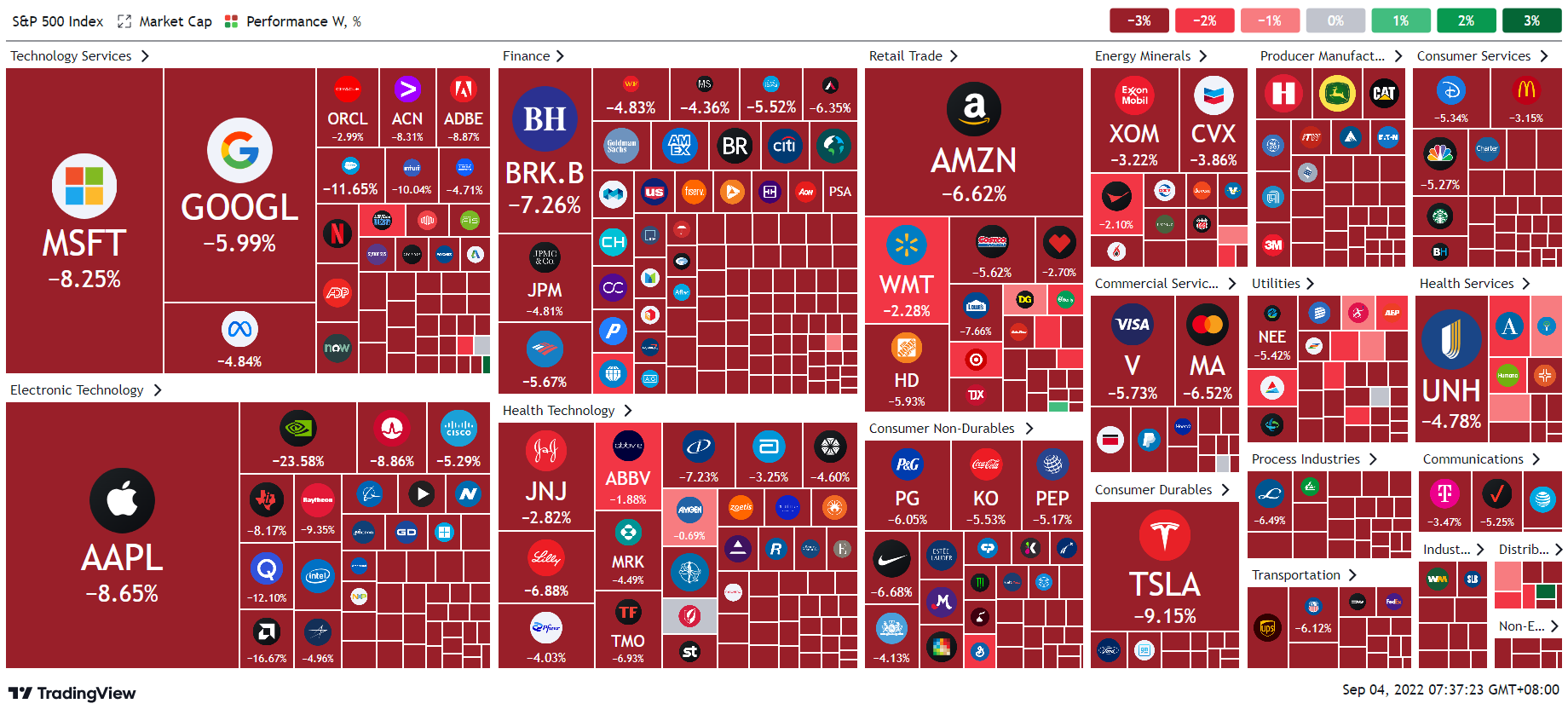

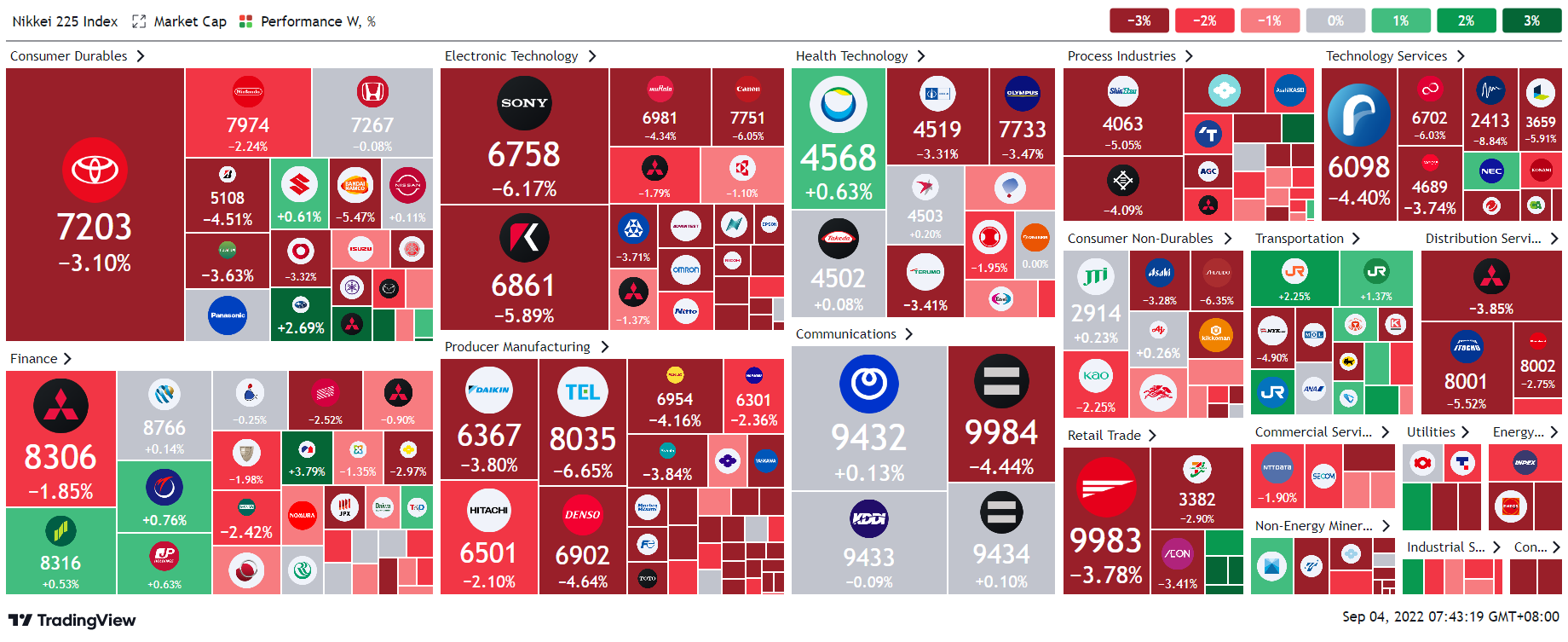

Equity Market Weekly Returns (S&P500, Nikkei225 & Nifty50)

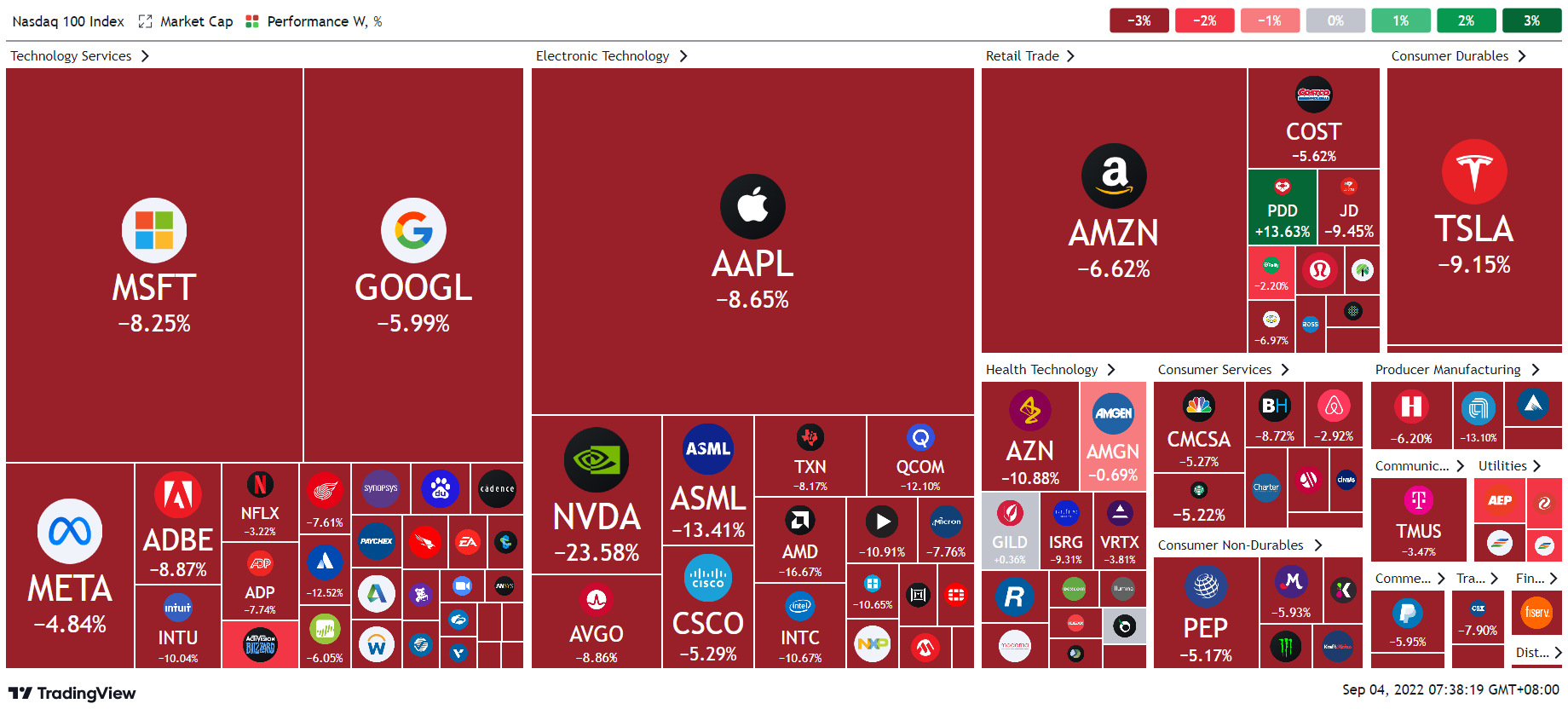

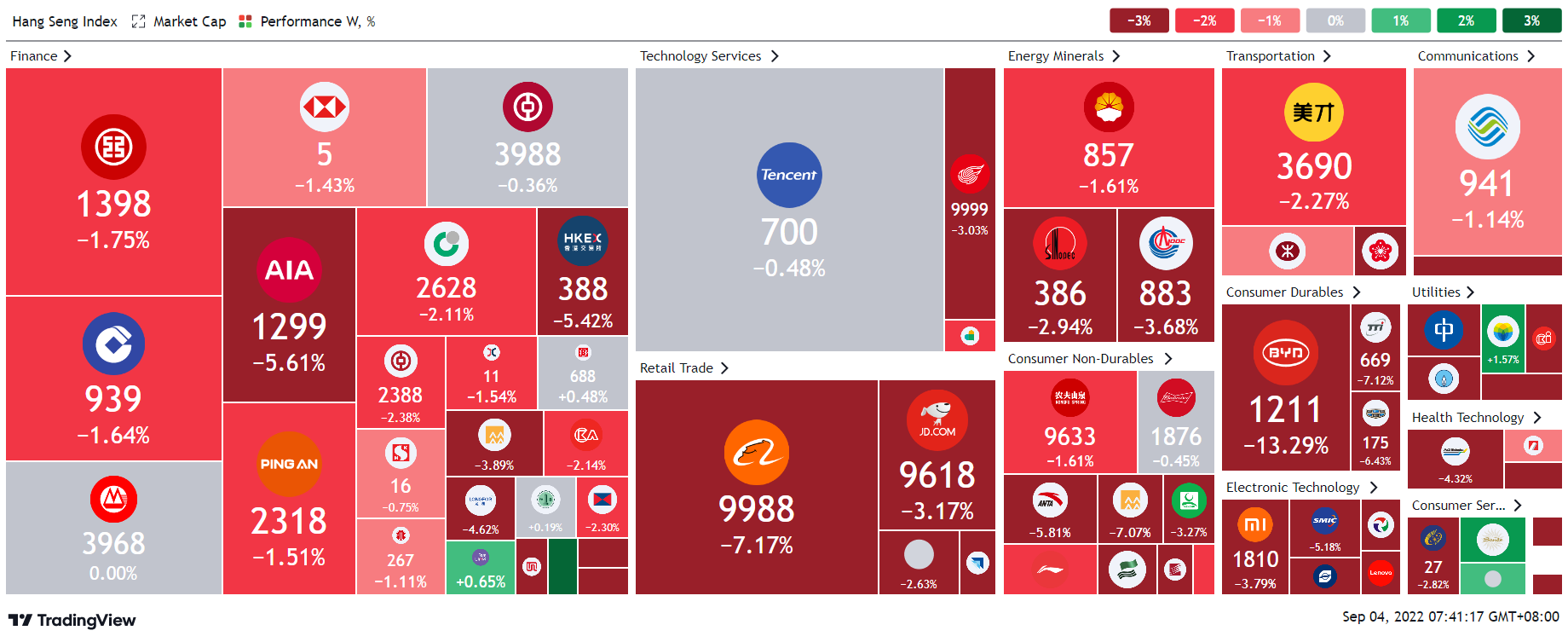

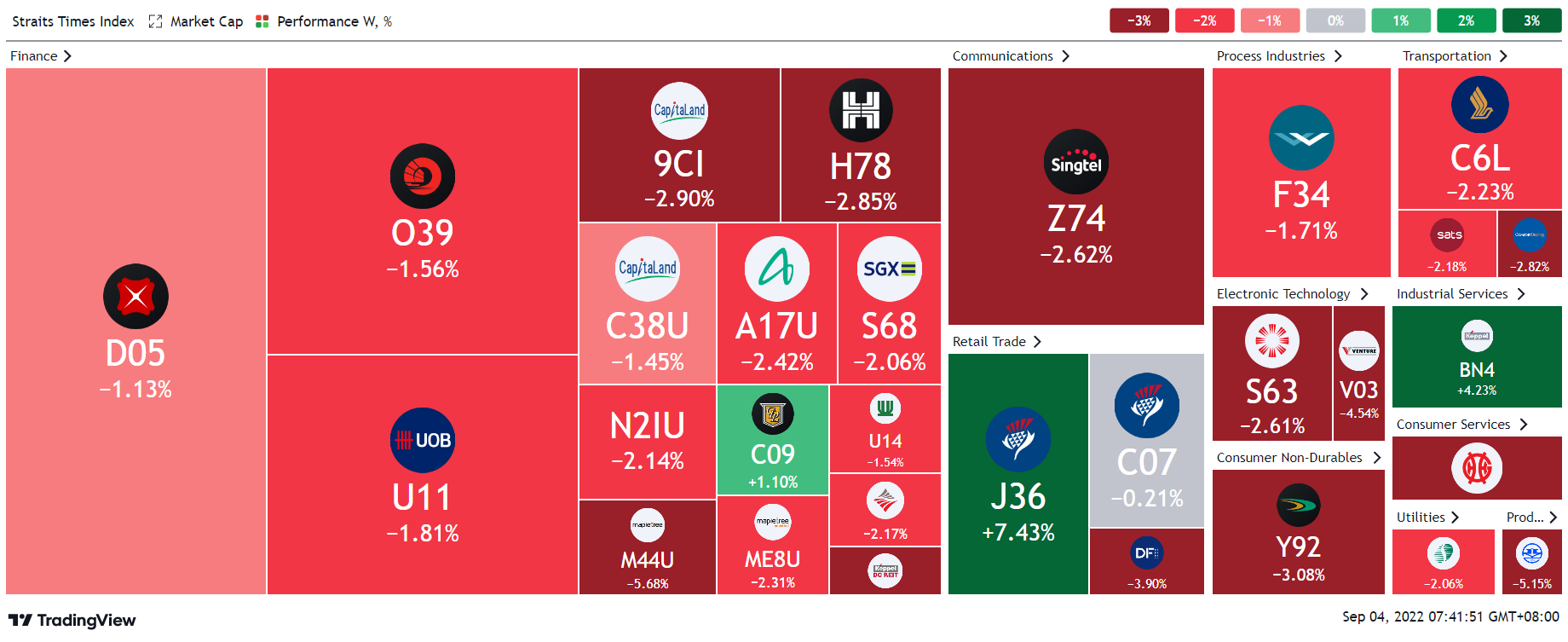

Click here to see heatmaps of equity markets in Nasdaq100, Hong Kong, Singapore, and Taiwan.

Apple product launch on 7/Sep against the backdrop of dominant market share (>50%) for its phones

Apple Inc.’s big product launch is expected to unveil the iPhone 14 and new watches. This year's event is themed “Far Out” with the invite set against a cluster of stars in outer space.

What could “Far out” stand for? Mark Gurman of Bloomberg thinks that the space theme could be a reference to satellites.

He reported previously that Apple was planning to add significant satellite capabilities to its devices, including an emergency texting feature and a mechanism for reporting major incidents in places without cellular service. Apple has also internally discussed the idea of giving its watches satellite features.

Another possibility is that Apple is hinting at enhanced photography capabilities or a feature that could rival Google’s long-existing astrophotography mode.

Meanwhile, Apple outstrips Android in US for share of smartphones used. Apple has overtaken Android devices to account for more than half of smart-phones used in the US. That gives Apple an edge as it enters finance and healthcare sectors.

Subscribers of Apple services reached 860 million; that’s 2X the number of Netflix & Disney+ subscribers combined. Services deliver 70% profit margin to Apple

>50% milestone was first passed in the quarter ending in June, according to data from Counterpoint Research. About 150 devices using Google’s Android operating system, led by Samsung and Lenovo, accounted for the rest.

Android-powered smartphones first went on sale in 2008, a year after the iPhone launched, and overtook the iOS installed base in 2010, according to NPD Group. In the three previous years, Apple never had anything near 50% market share, as sales were dominated by Nokia, Motorola, Windows and BlackBerry.

With the iPhone reaching saturation, Cook has pushed into movies, television, advertising, payments and fitness & health, leveraging an installed global base for iPhones that surpassed 1 billion in 2020.

Apple’s installed global user base surpassed 1 billion in 2020

The result is a diverse set of “services” revenue that consistently grows in double digits and delivers profit margins north of 70% and that is twice the profitability of its hardware business. Subscribers of Apple services reached 860 million in the June quarter — roughly double the number of Netflix and Disney+ subscribers combined.

India sets its eyes on semiconductor manufacturing & targets to quadruple electronics industry to $300B by 2026

India has put $10B of incentives to attract manufacturers to set up new “fabs” (semiconductor fabrication plants) and encourage investment in related sectors such as display glass.

$300B by 2026, up from $75B in 2021

If successful, an Indian chipmaking industry has the potential to be extremely lucrative for the country, supporting a rapidly growing global demand as well as its domestic industry’s voracious needs.

Manufacturers are lining up to take up the $10B offer. Singapore based IGSS Ventures has signed MoU with Tamil Nadu state government. ISMC (Israel based JV between Israel’s Tower Semiconductor & Abu Dhabi-based Next Orbit Ventures) has signed LOI with Karnataka state government. Foxconn has teamed up with Indian group Vedanta to build a semiconductor plant, surveying sites in Gujarat and Maharashtra.

Complexity of semiconductor production and supply chains have led to supply concentration, led by China, Taiwan and South Korea. That is now changing. In July, the US passed the Chips and Science Act that includes $52B of grants to support chipmaking and research and development. Meanwhile the EU is looking to build semiconductor resilience with its own €43B Chips Act.

New Delhi laid out its pitch to chip-makers last December with the India Semiconductor Mission, unveiled by the IT Minister Ashwini Vaishnaw.

India’s ambition is to triple its revenues from the electronics industry to $300B by 2026, up from $75B in 2021, and to export $120B of that.

Sources: FT, India Semiconductor Mission, and India Electronics Overview

US Non-farm payrolls increase by 315k; unemployment rate increases to 3.7%. Labor market shows signs of cooling.

The US added 315k new jobs in August higher than the expected 300k but lower than the gain of 526k in July. The US Labor Department’s employment report also revised the number of jobs created in June down by 107k.

US added 315k new jobs in August higher than the expected 300k

The hourly pay rose a modest 0.3% in August to $32.36, marking a high YoY increase of 5.2%.

Unemployment rate rises to 3.7% in August from 3.5% in July. The increase in unemployment rate could be linked to 786,000 people entering the labor market moving the overall size of the labor market to a record high.

The broad increase in hiring last month was led by the professional and business services industry, which added 68,000 jobs. Healthcare payrolls increased by 48,000 jobs. Employment in the retail trade sector rose by 44,000 jobs, while manufacturing added 22,000 positions. Construction employment rose by 16,000 jobs. Leisure and hospitality payrolls increased by 31,000 but remain below pre-pandemic levels.

Source: Marketwatch, Reuters, US Bureau of Labor Statistics

September has the notorious reputation of being the worst month for stock returns. Reason remains mysteriously unknown.

Source of September’s terrible stock market record remains as mysterious as ever. Since 1897, the first full year of the Dow Jones Industrial Average’s DJIA existence, the U.S. market benchmark has produced an average loss of 1.13% in September. That compares to an average gain of 0.77% across the other 11 months of the calendar.

Over the 125 year history, September had produced a loss of 1.13% on average relative to 0.77% average gains across the remaining 11 months

The U.S. market’s poor showing in September also has remarkable consistency. There are myriad ways of slicing and dicing data into various subsets, and in most of them the average September still is a loser for stocks.

If statistics alone were a sufficient basis for betting on a pattern, then traders could be comfortable expecting stocks to post a loss in September. But, as statisticians remind us, correlation is not causation.

That doesn’t mean none exists; it’s impossible to prove a negative. But the continued failure to discover such an explanation, despite numerous efforts, makes it increasingly likely that no such explanation will be found.

Source: James Wong

Growing affluence, Newly minted billionaires, Crackdown on ultra-rich, and Covid restrictions continue to cement Singapore as Asia’s wealth center

Wealth management professionals in Singapore are reporting an increasing number of tycoons from across South China Sea and Indonesia.

MAS estimates that there were about 400 single family offices as at the end of 2020, and about 700 at the end of last year.

Start with China first. Years of political crackdowns, severe Covid-19 lockdowns, and rising unease of Beijing's global reputation, many rich Chinese are setting up family offices in Singapore.

FT Wealth reports that previously Hong Kong used to be the natural out-of-China stepping stone. Now, the real offshore for in Asia has defaulted to Singapore.

Beijing’s increasing talk of "common prosperity" and "going after the entrepreneurs" has made it unsettling for those Chinese who made their fortunes in China.

For family offices in Singapore to qualify for tax exemptions, minimum investment of S$10m (USD 7.1m) & in some cases employment of professional from outside the family is required.

Second Indonesia. This week, The Business Times reported that Indonesia’s newly-minted tech billionaires are beginning to “diversify their wealth and are increasingly looking to Singapore to set up family offices and seek new investment opportunities”.

Indonesia’s traditional family-owned businesses have long established a presence in the Singapore and now technopreneurs are now joining this exclusive club.

SEA’s largest economy has produced 13 unicorns over the past decade, including startups such as Gojek, Tokopedia, Bukalapak, OVO (PT Visionet Internasional), and Traveloka; while the accelerated digital adoption over the pandemic created newer second-generation unicorns Xendit, Ajaib, and PT. Global Jet Express (J&T Express).

The Monetary Authority of Singapore (MAS) estimates that there were about 400 single family offices as at the end of 2020, and about 700 at the end of last year. Some estimate that the number of Indonesian family offices in Singapore has risen by as much as 50% over the past three years.

Source: FT Wealth, Business Times

Quant Hedge Funds pile into Warren Buffet’s Berkshire Hathaway

Hedge funds have been buying into Berkshire Hathaway stock in Q2 ‘2022, with DE Shaw, Renaissance Technologies and Bridgewater Associates buying millions of shares.

USD 900M; Top hedge fund names collectively have bought shares worth >$900M as at end of June

Berkshire meets many of the criteria for such funds and has become a favourite this year. Its shares are relatively inexpensive based on its earnings compared with many other companies. Berkshire, which is the largest component in the S&P 500 value index, has fallen 6% in 2022, far outperforming the 17% decline in the benchmark S&P 500.

New buyers list is dominated by quant funds with top names collectively buying shares worth more than $900mn at the end of June as per Financial Times reporting.

Berkshire (class B stock) ranked among the 10 largest holdings for 22 hedge funds, while 98 of the money managers tracked by Goldman disclosed a stake in the company. It stands out on a list of the most popular long bets that is otherwise dominated by technology companies such as Amazon, Microsoft, Apple and Face-book owner Meta.

Source: FT

Yen's decline accelerating as it trades past 140 to the dollar

The new 24-year low of ¥140/$. What gives? Widening policy divergence between the rate-raising US Federal Reserve and resolutely ultra-loose Bank of Japan. Hawkish comments from Fed officials. Anticipated rate rises in the US in coming months.

Yen trades at a new 24-year low; Yen has come under ever more downward pressure from rising yen carry trade being the world’s only zero yielding currency

Some traders say they can identify no obvious technical support levels between here and the yen’s 1998 low of ¥147/$. Analysts at JPMorgan said on Thursday that they would not rule out the yen falling more deeply past ¥145/$, as policy divergence resumed an influence over the currency pair that had broken down over the summer.

A weaker yen has, in the past, prompted net buying of Japanese stocks. In 2022, however, the yen has plunged and foreigners have been net sellers of over ¥650bn of stocks since January.

Meanwhile, said JPMorgan’s Benjamin Shatil, the yen has come under ever more downward pressure from the recent surge in the so-called yen “carry trade” — the investment strategy of borrowing in a low-yielding currency and selling it to fund speculative investments in higher ones.

As countries other than the US enter monetary tightening cycles, the yen is rapidly becoming the world’s only zero-yielding currency, inviting yen-funded carry trades across a widening selection of currency pairs.

Source: FT

Even as markets have corrected massively, more pain in store remains if history of bear markets were to repeat

In eleven of the past sixteen bear markets, stocks have experienced their largest losses in the last third. Losses in that third part have on average been twice as large as the losses in the first and second parts.

Why?

One potential explanation is that behavioral biases prevent investors from accepting the new reality.

Biases like anchoring (sticking to recent ATH), extrapolation (believing in the Fed put), the disposition effect (growing fond of stocks they own), and underreaction to news (seeing the worsening conditions, but refusing to sell) all lead investors to cling to their stocks for as long as possible.

On average, markets have shed 24% in the final third of a bear market cycle

Eventually though, when stocks slide far enough or for long enough, those biases give way, fear replaces greed, and investors finally start to reduce their stock holdings rather than buy the dip. Negative sentiment and selling pressures feed through each other and lead prices to fall sharply. And it’s only after investors have "really" thrown in the towel that stocks can bottom.

Right now, it seems we’re much closer to the first rather than the last stage. Investors are still holding dearly to their stocks, and there's certainly no sign of capitulation. And even if the narrative is turning more negative, expectations for companies' earnings and margins remain way too optimistic.

Investors may be slowly accepting that the macro environment is changing for the worse, but it's still a long way before it's fully reflected in the price.

Sources: Merk Investments via Finimize, Chart by Mint Finance

BYD net income triples in H1 to 3.6B Yuan ($521M) with record output and sales

BYD reported revenue of 150.6B Yuan up 66% YoY (166B expected). Net income in H1 tripled from a year earlier to 3.6 billion yuan ($521 million) (2.8B – 3.6B expected).

Revenue from automobiles and related products rose 130% to about 109 billion yuan in H1, while handset components, assembly services and other products dropped 4.8% to 41 billion yuan.

BYD has managed supply-chain disruptions better than others as it makes its own components such as batteries and semiconductors. The company also avoided the majority of Shanghai’s Covid lockdowns because it has factories elsewhere.

BYD could deliver 1.5 to 2 million vehicles this year as capacity expands to meet a backlog of orders.

BYD sold more new energy cars in the first seven months of this year than in 2020 and 2021 combined.

The group’s share of China’s NEV market reached 24.7% in H1. The company is expanding overseas, announcing sales in seven new markets in recent months, including Japan, Thailand and Germany. (Bloomberg)

Source: Bloomberg

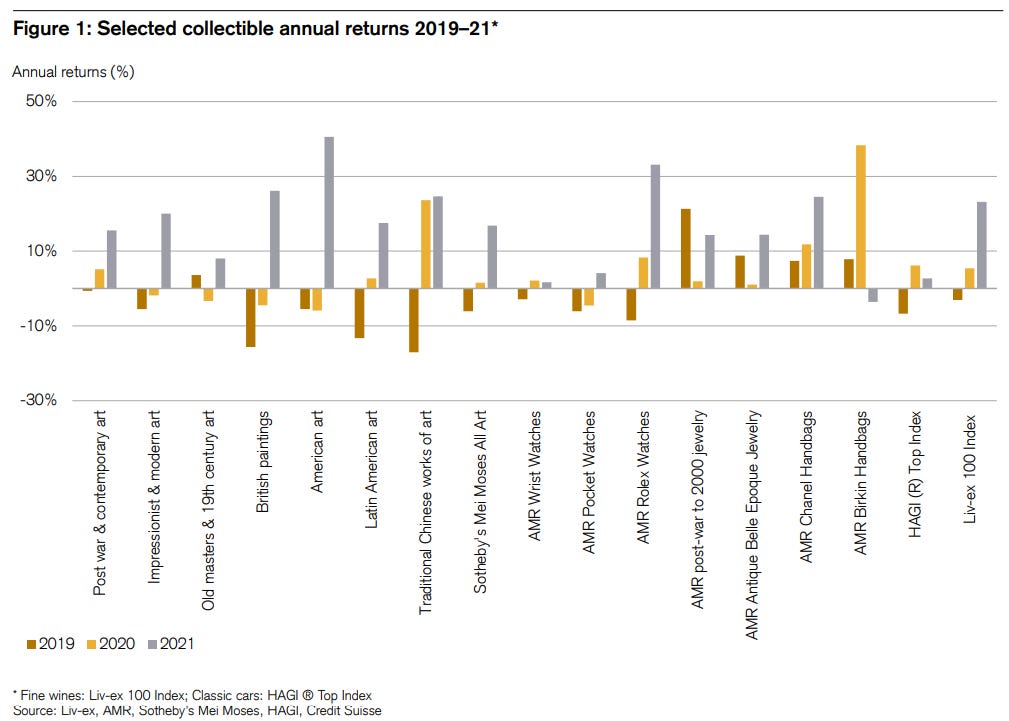

Collectibles may offer hedge against inflation. Investors have to be mindful of risk-to-reward ratio besides being wary of transaction costs & liquidity.

Inflation is everywhere. No market - developed or developing - has been spared. In some cases, they are at record highs unseen in decades. No where to hide? Or is there?

Chanel handbags, Rolexes and traditional Chinese works of art, offer best inflation protection according to a report published by Credit Suisse in collaboration with Deloitte.

Before diving in to invest into these collectibles, investors have to be mindful of that holding these assets are expensive relative to financial asset holdings. Storage and insurance can be material enough to erode returns.

Unlike financial assets - majority of which can be traded on a liquid order book - collectibles cannot easily be dealt with. Transacting at auctions can be expensive and slow.

As Stephen Wagstyl of FT Wealth puts it, “Just don’t expect to turn this stuff easily into cash in a crisis”. He further adds that, “In extremis, you may not find a buyer, but you will at least be able to drown your sorrows in style”.

Chanel bags & Rolex watches have delivered >200% in returns-to-risk ratio

Source: FT Wealth, Credit Suisse and Deloitte report

Equity Market Weekly Returns (Others)

Previous Issues

Disclaimer

Mint Macro Review is for informational purposes only and does not constitute financial, investment, risk management, accounting, or tax advice. Nothing stated in this document is to be construed as a recommendation, solicitation, endorsement or offer to buy or to deal in any financial products.

Trading and investment in any financial products are exposed to risk. There are no such thing as risk-free returns. This material has been published for general education purposes only. It does not address specific investment or risk management objectives, financial situation, or needs of any person.

Advice should be sought from a financial advisor regarding the suitability of any investment or risk management product before investing or adopting any investment or hedging strategies. Past performance is not indicative of future performance.

Questions and/or feedback, please write to learnmore@mintfinance.xyz