Mint Macro Review - Issue 5

Mint Macro Review - Issue 5

#mmr | 04/Sep to 10/Sep

Mint Macro Review (#mmr) is Mint Finance’s weekly observations and commentary on global macro forces and key business updates.

In this week’s edition, as much as we dislike sounding gloomy; market developments, indicators and expert commentators aren’t seeing anything but just that.

Speaking to CNBC, financial historian Dr Niall Ferguson said that the conditions required to spark a repeat of 70s raging inflation plus international conflict, is at work. More political and economic upheaval is what he sees coming.

In a research paper, world’s largest hedge fund - Bridge Water’s Bob Prince, Aaron Goone and Atul Narayan - argue that equity markets have not priced in next stage of QT. More price correction to the downside is what they see coming.

In line with that, institutions have been buying up record levels of portfolio insurance in the form of long puts which is 3X more than what was seen in 2008 GFC.

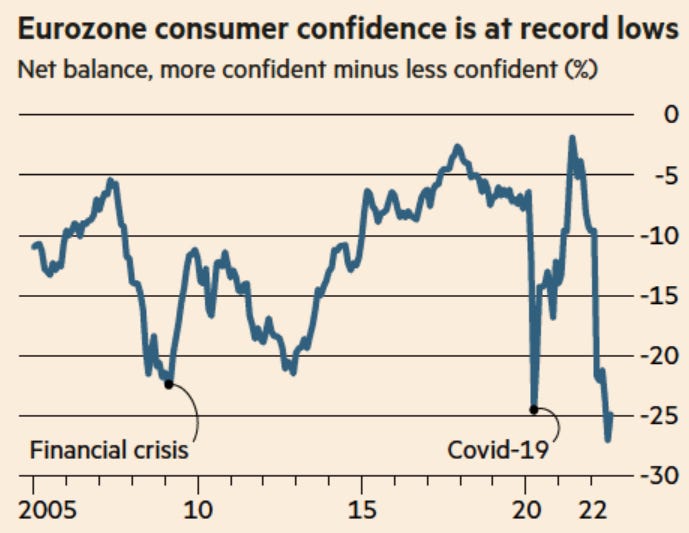

Two-thirds and more of Bloomberg’s poll respondents (53,000 of them) expect stock prices to keep falling. Eurozone consumer confidence is at record low. All of this, well before the onset of winter.

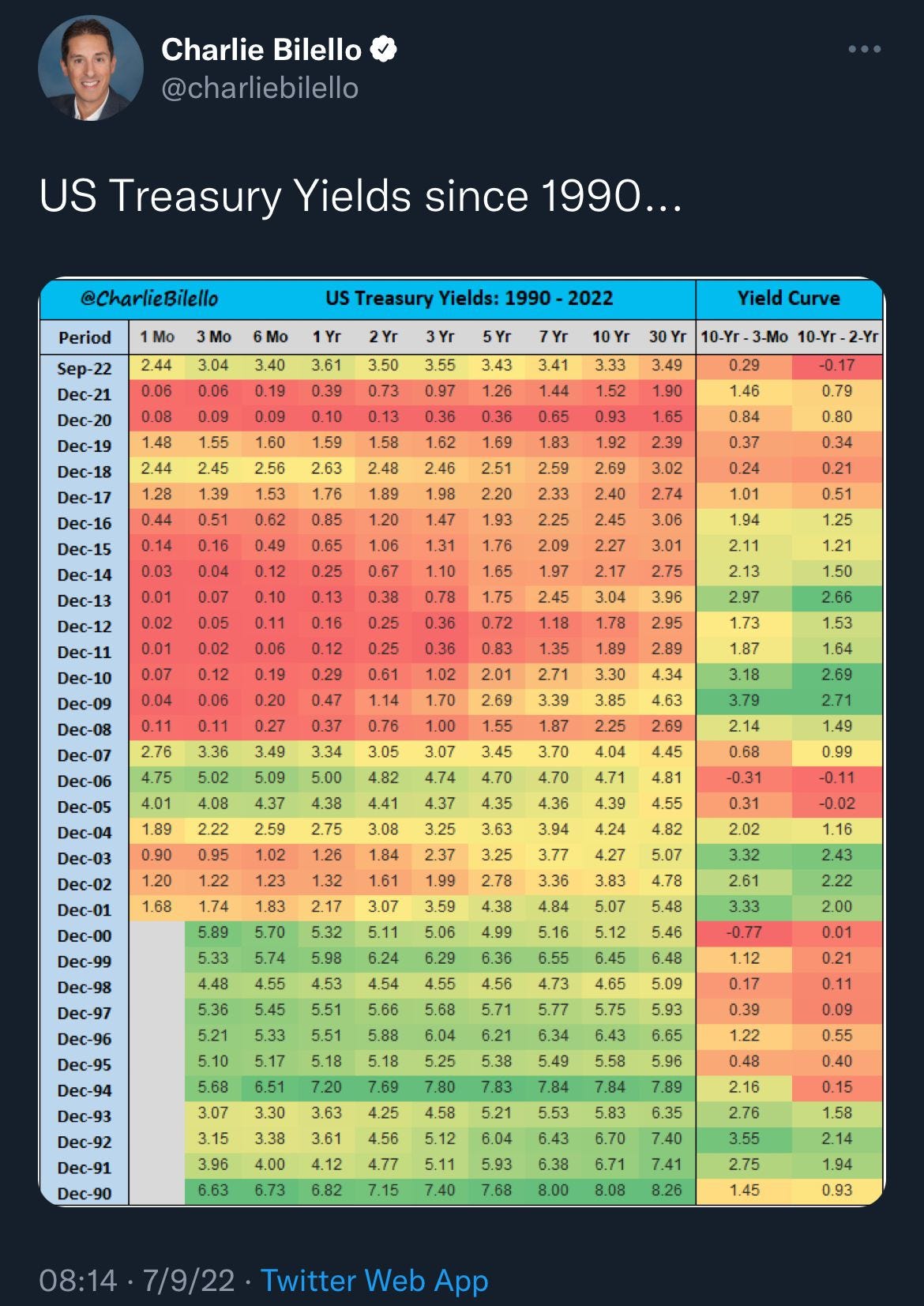

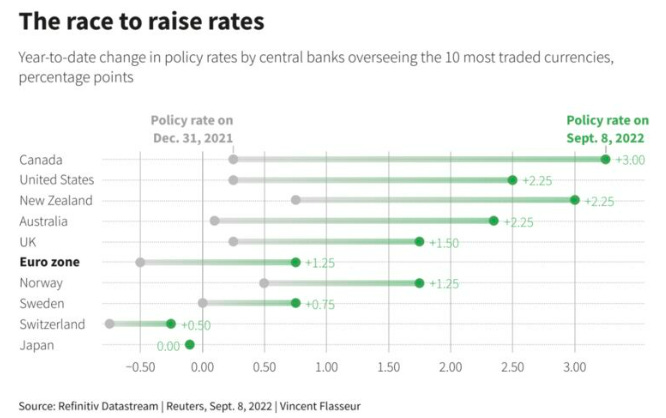

Rising rates and an inverted 10y-2y yield curve as evidenced from the charts below points to a recession ahead. For many analysts, recession has moved from being a risk-scenario to a base-case scenario.

Every cloud has its silver lining. We’re looking for one.

Source: @charliebilello on Twitter

In this week’s #mmr

Read Mint Disclaimer

Read previous issues - Issue 1, Issue 2, Issue 3 and Issue 4.

Executive Summary

GLOBAL MACRO NEWS

Inflating Geopolitics and Pandemic induced fiscal & monetary policies, are likely to create an upheaval worse than in the 70s, says Dr Ferguson. (read more)

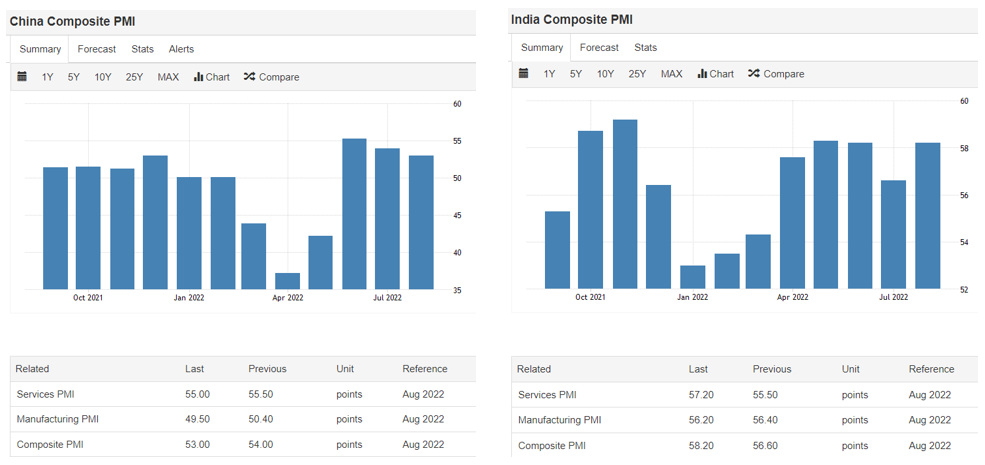

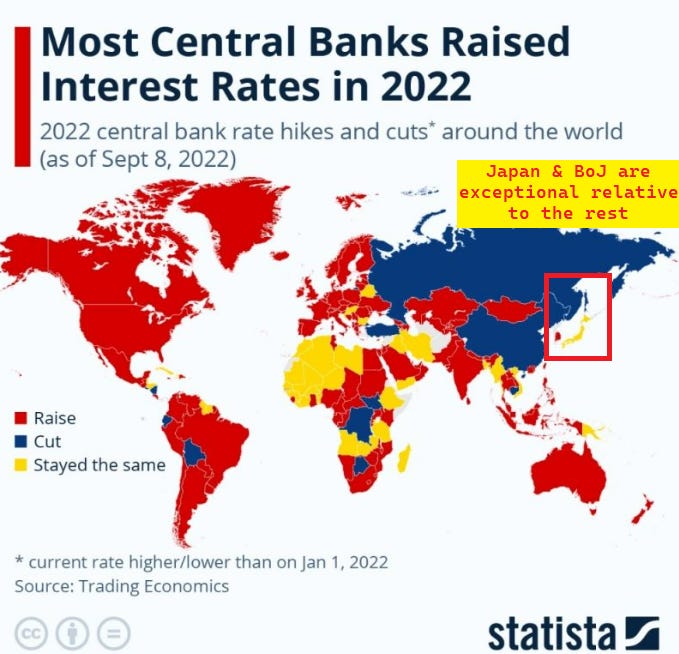

Aug PMI readings show contraction in Japan, EU and the UK. India PMI points to growth and expansion while economic activity in China holds steady. (read more)

US Fed’s swift rate rises to fight surging inflation has created a strong USD. (read more)

Equity Markets aren’t pricing the next stage of QT. (read more)

Required rebound in market returns to fully recover from a drawdown isn’t trivial. Rate of return to recoup losses is not asymmetric. (read more)

Resilient India: Its economy appears to be resilient in the face of significant downturn in all other major economies. What explains? (read more)

COMPANY NEWS AND UPDATES

Since Jobs, Apple has squeezed lot of juice from its product range and “evolutionary” changes with little, if any, revolutionary product innovation. (read more)

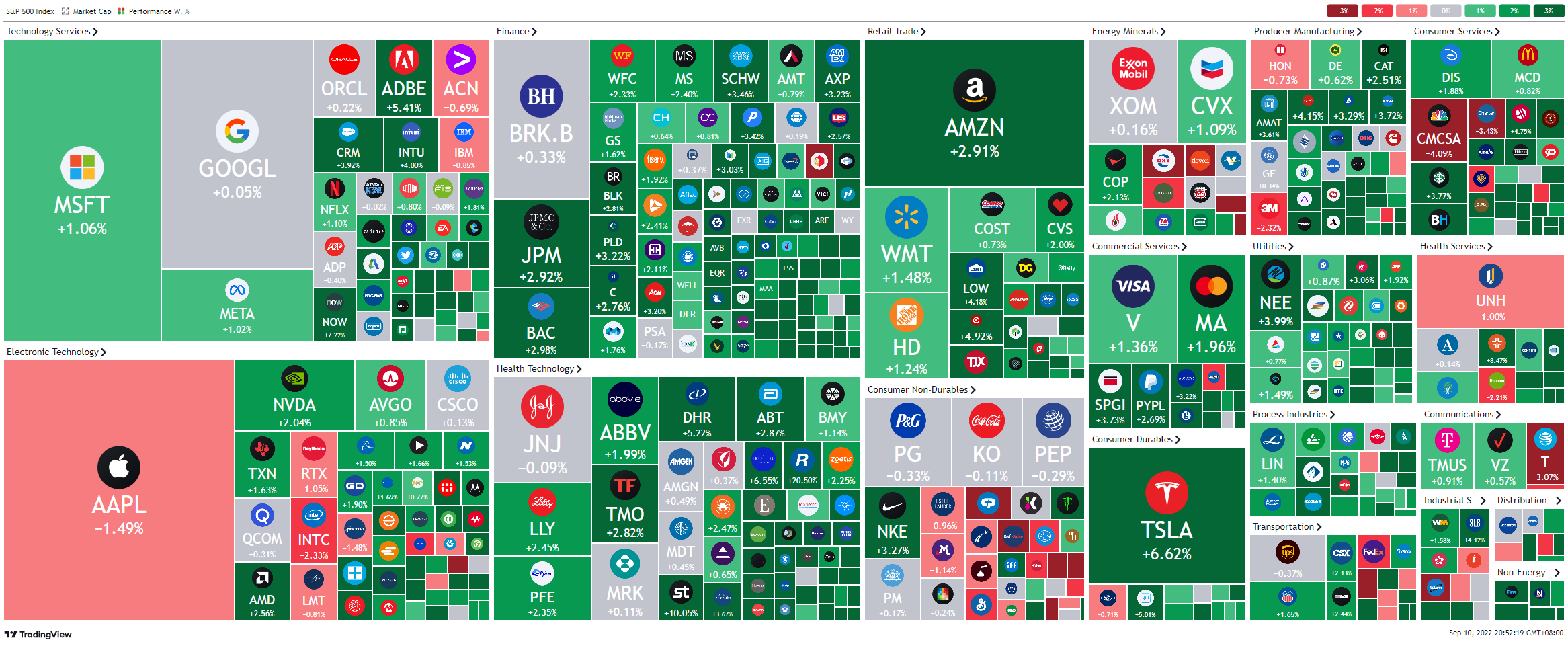

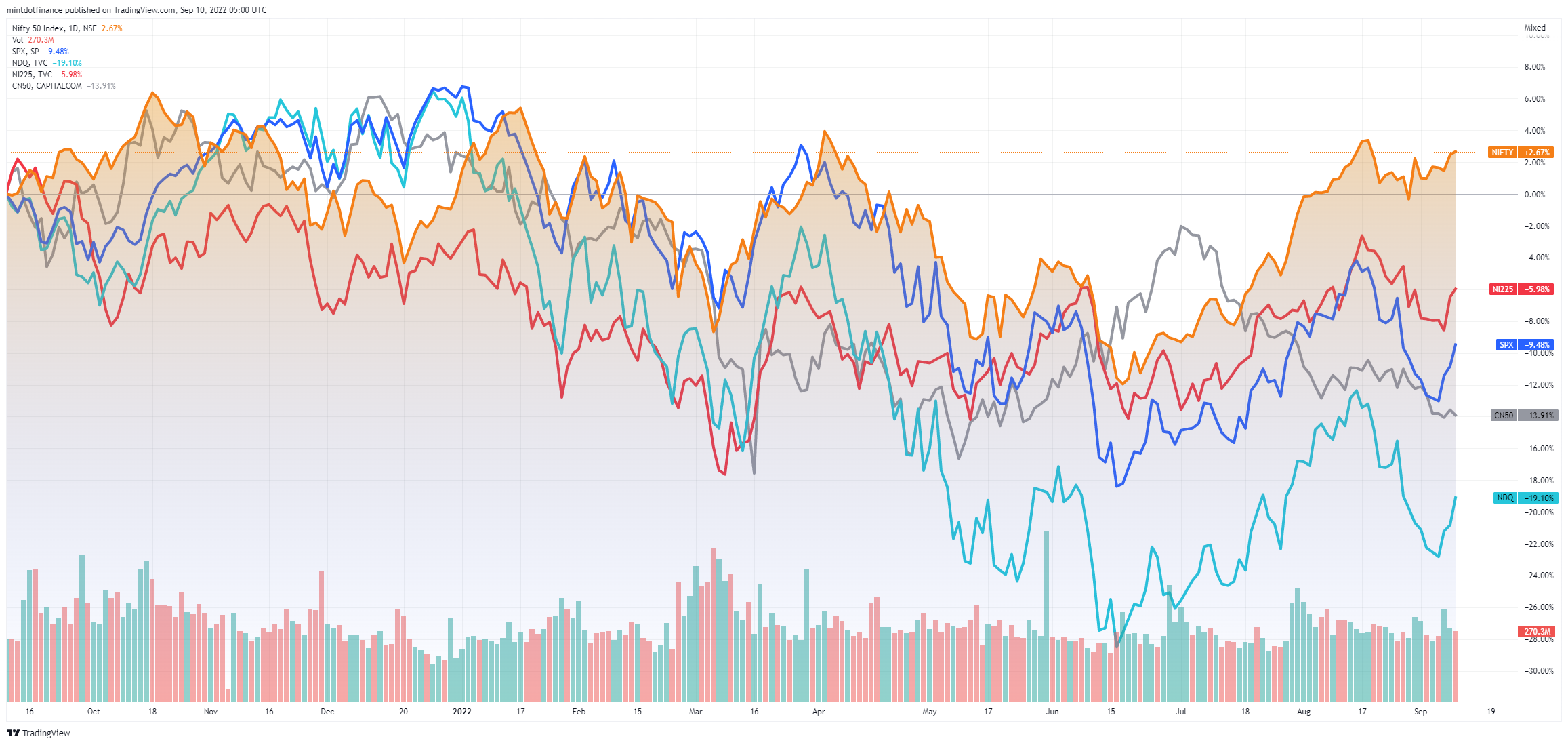

Equity Market Weekly Returns (S&P500, Nikkei225 & Nifty50)

Click here to see heatmaps of other leading equity markets.

Macro News Highlights

Source: Mint Market Watch

GLOBAL MACRO NEWS

Inflating Geopolitics and Pandemic induced fiscal & monetary policies, are likely to create an upheaval worse than in the 70s, says Dr Ferguson

Speaking to CNBC at the Ambrosetti Forum in Italy, Historian Niall Ferguson said that the conditions required to spark a repeat of the 70s i.e. raging inflation plus international conflict, is in place.

lower productivity growth, higher debt levels & less benign demographics point to upheavals far worse than 70s

Dr Ferguson asserted that the world is sleepwalking into political and economic upheaval similar and worse than the 1970s.

Akin to the present war in Ukraine, the 1973 Arab-Israeli War led to involvement of superpowers - the Soviet Union and the U.S., sparking a wider energy crisis. Back then, the war lasted 20 days in contrast to the six months and still waging this time around.

Politicians and central bankers have been vying to mitigate the worst effects of the fallout, by raising interest rates to combat inflation.

Among the reasons for that, he said, were currently lower productivity growth, higher debt levels and less favorable demographics now versus 50 years ago.

Concerns expressed by Dr Ferguson is perhaps expressed in the size of the puts established by institutional traders as evidenced in the chart as tweeted by @sentimentrader.

In 22 years of doing this, none stand out like this one. Last week, institutional traders bought $8.1 billion worth of put options. They bought less than $1 billion in calls. This is 3x more extreme than 2008.

Institutional traders bought $8.1B worth of puts which is 3x more extreme than 2008

A Bloomberg YouTube poll earlier this last week points to similar sentiments of more pain in store for equity markets.

Source: CNBC, @SentimenTrader on Twitter, Bloomberg YouTube Poll

Purchasing Managers Index (PMI) shows contraction in activities in Japan, EU and the UK. India PMI points to growth and expansion while economic activity in China holds steady.

Japan service sector activity contracted in Aug as a resurgence in COVID-19 infections hurt demand. Service Purchasing Managers Index dropped to 49.5 in August from 50.3 in July. Composite PMI which measures both services and manufacturing also dropped to 49.4 indicating overall contraction in Japan’s private sector.

EU Composite PMI dropped further in Aug, indicating that the EU is heading into a recession. EU Services PMI fell to 49.8 in Aug from 51.2 in Jul. Composite PMI which measures both manufacturing and services also declined to 48.9 in Aug from 49.9 in Jul.

PMI < 50 indicates contraction. PMIs in JP (49.4), EU (49.4) & UK (49.6) exhibits economic contraction. Data from India (58.2) points to economic growth & resilience.

UK slides into contraction in Aug as composite PMI dropped to 49.6. The UK reported services PMI of 50.9 in August down from 52.6 in July. Overall, the Composite PMI dropped to 49.6 in August from 50.9 in July.

India Services PMI remains strong at 57.2 indicating resilience of service sector. India's seasonally adjusted services PMI, for August, stood at 57.2, up from four-month low of 55.5 in July. Gains in new business, ongoing improvements in demand conditions and job creation fueled the rise in the index with optimism at its greatest degree since May 2018.

China Caixin Services PMI dropped to 55 in Aug from 55.5 in Jul. Despite the decline, the index showed strong sector growth.

Sources: Trading Economics, Reuters (Japan), Marketwatch (China), Reuters (EU), Reuters (UK), and, CNBCTV18 (India)

US Fed’s swift rate rises to fight surging inflation has created a strong USD

Given raging inflation, the same sum of USD buys less than before at a grocery store. But, travel past the American shores, the same sum of USD will buy much much more.

Euro is trading below par $0.99 at a twenty year low, while one pound can be bought at $1.15 (the lowest level for the since 1985).

US Fed's continuing support for steep interest rate hikes to fend off rising inflation has been more aggressive than any other major economies. Naturally that's made the dollar attractive to investors seeking higher rates on their cash. This trend is likely to continue given the Fed's firm resolve in breaking surging inflation.

A stronger dollar isn't strictly a good, or bad, thing. Importing goods from abroad is now relatively cheaper for Americans. However, firms selling abroad, its products are now pricier and consequently less competitive than before.

Meanwhile, the Renminbi is tumbling. The drop in the value of the renminbi is symptomatic of the deep problems facing the world's second-largest economy. The Chinese policymakers who influence the currency have in the past drawn a line in the sand around the 7-per-dollar level and seemingly resist to let it move beyond that.

The Renminbi has weakened by as much as 10% against the dollar over the last six months and on Thursday was hovering around 6.96 per USD.

If the government doesn't want the price to cross a certain level, it gradually moves the official price away from that number. The last time the yuan crossed the 7-per-dollar mark was during the height of the trade war in 2019.

Currency analysts expect the Renminbi to pass 7-per-dollar soon, and say it's a sign that China's policymakers are growing more worried about the malaise of their economy.

Zero-Covid policy has resulted in repeated and ongoing lockdowns that are hobbling economic activity. China's housing market is witnessing one of its largest downturn on record denting Chinese consumer confidence and retail sales. A bright spot for China is its strength in exports.

A weaker currency basically allows China to build on that export strength since the U.S. is its largest export market.

Chinese officials won't want the RMB to tumble too fast spooking investors leading to rampant capital outflow.

Meanwhile, the Bank of Japan (BoJ) has held ground (via Yield Curve Control) on loose monetary policy keeping rates unchanged even in the face of rising inflation.

That makes the Yen, even more attractive for running carry trades against more FX pairs as it is the only non-yielding currency. Currency experts anticipate that continued rate increases from the Fed could result in JPY breaching 147 to the dollar, a level last seen in 1998.

Source: Chartr, Axios, FT, ECB

Equity Markets aren’t pricing the next stage of tightening cycle

According to Bridge Water Associates (BW), while equities are discounting elevated interest rates, the market is not taking into account the impact of QT (quantitative tightening) on growth and earnings.

Analysts at BW believe that the current tightening cycle will result in some mix of weaker growth, higher rates, and/or stubbornly high inflation. These outcomes present risks to equities that investors need to consider.

Tightening cycles are adverse for asset prices. As discount rates rise, present value of future cash flows drop. To entice investors away from cash and into those assets, yields on such assets must rise.

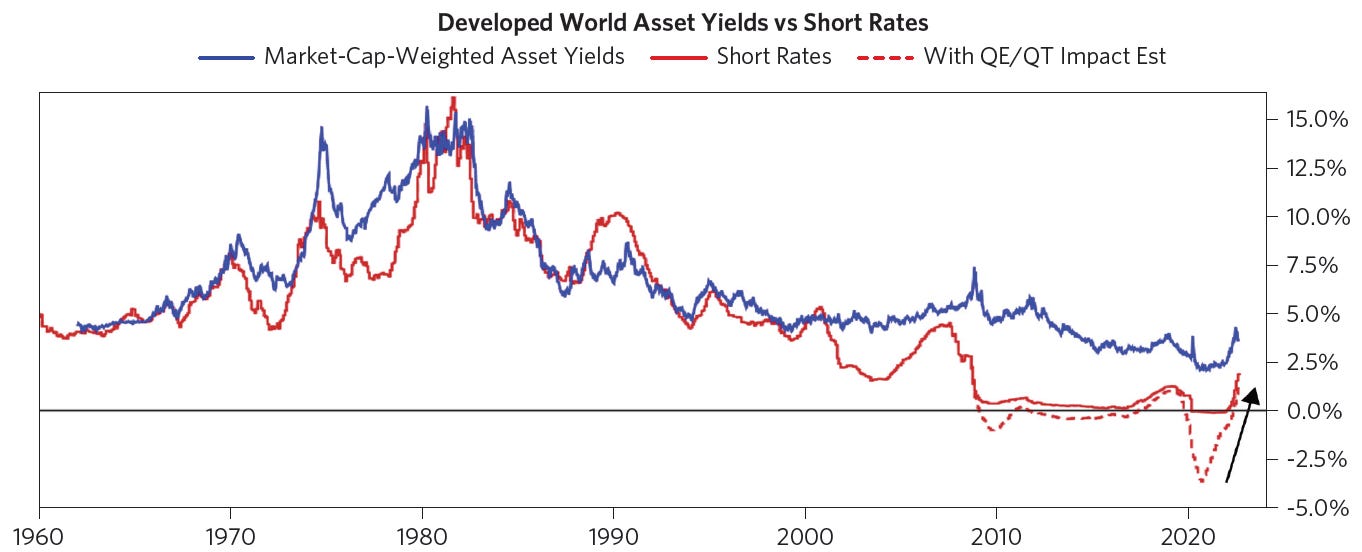

Chart below shows developed asset yields alongside short rates.

As rates rose this year, asset yields in the developed world rise. Such tightening environments, when cash is becoming more attractive, are terrible for financial asset returns, as the rising discount rates and risk aversion weigh on prices.

While the response of asset yields to rising short rates is rapid, typically it takes more time for the tightening to shake the economy leading to earnings decline. Inflation comes down with a lag to the decline in the real economy. Tightening cycle generally doesn’t end until it is clear that inflation will soon come down to reasonable levels.

Equity prices are most vulnerable during the period when earnings decline and there is continued tightening combined with rising asset yields.

According to BW analysts, equity markets are still in a transition phase and haven’t yet reached the point where reported earnings or analyst forward EPS expectations have started to come down.

In short, more pain, more drawdowns and price corrections are still in store. This vindicates the analysis presented in last week’s #mmr.

Source: Bridgewater Associates, LP

Required rebound in market returns to fully recover from a drawdown isn’t trivial. Rate of return to recoup losses is not asymmetric.

Powerful graphic visualization from Compounding Quality depicting the percentage gains required to fully recover from a loss.

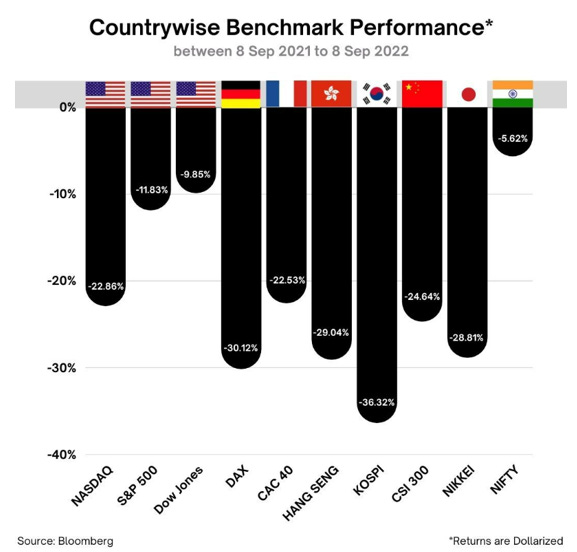

Equity markets in US, Europe, Japan and China have come off fiercely and more seem to be in store.

Percentage of stocks delivering dividend yields > 10-year US Treasury yields is less than 10% akin to the time before the commencement of Global Financial Crisis (GFC) of 2008.

Source: Compounding Quality, Bloomberg

Resilient India: Its economy appears to be resilient in the face of significant downturn in all other major economies. What explains?

The IMF forecasts real GDP growth of 7.4% this year. According to Pine Bridge Investments, the long term force vectors including digitalization, decarbonization, growth in direct-to-consumer commerce, and the geopolitical rewiring of supply chains will play to India's benefits.

S&P BSE Sensex index is expected to double over the next three years

In Pine Bridge’s assessment, five reasons explain attractiveness of Indian equities:

Large and liquid opportunity set (India is the third-largest equity market in Asia ex Japan in terms of market cap, after China and Hong Kong plus the value of share trading reached US$123 billion in June 2022, making it one of the more liquid markets in the region)

Corporate profits are looking up (The S&P BSE Sensex index is expected to double over the next three years, led primarily by compound annual corporate profit growth of 25%)

Rising ESG awareness may usher in positive change (renewable energy generation in India has been increasing; while coal dominates power generation, the country aims to reach 450GW of renewable capacity by 2030. By 2040, solar power is expected to match coal’s share of power generation)

Growing global interest in India equities (global benchmark exposures to India equities remain low relative to the size of its economy; the structural misalignment in the benchmarks is a long-term positive for investors, with India’s weight expected to eventually increase)

Stable economic prospects (Unlike previously, India’s macroeconomic standing today is strong, with record-high FX reserves)

Source: Pine Bridge Investments

COMPANY NEWS AND UPDATES

Since Jobs, Apple has squeezed lot of juice from its product range and “evolutionary” changes with little, if any, revolutionary product innovation

On 7/Sep, Apple announced the new iPhone 14 and a refresh of its most-popular wearables, including new AirPod Pro and a more resilient Apple Watch.

New iPhone models support Emergency SOS messaging via communication satellites when the phone is out of range of a cell signal. iPhone’s antennas can connect to satellite frequencies. Apple says it can take <15 seconds to send a message with a clear view of the sky, and the interface guides users to point their phone in the right direction and walks them through the steps to connect with emergency service providers. It’s also possible to use the Find My app to share location without sending a message.

Notwithstanding elegant design updates, the iPhone 14 is an evolution and no product revolution in a long long time. Cook has been criticised for milking existing products rather than launching new revolutionary products.

Under Cook, Apple has more than tripled its revenue & stock prices are up more than 10x.

During Cook's tenure sales have more than tripled and the company's share price is up more than tenfold.

While the product suite may not have changed much, its services business is undergoing a revolution. Apple's services include the App Store, Apple Music, Apple Pay, Apple TV and a new area of intense focus — advertising.

Apple’s services contributes more revenues than Mac & iPad sales put together

After having made it difficult for other ad platforms like Facebook and Snap to target ads at users, Apple is reported to be ramping up its own advertising efforts.

The company is reportedly looking to double its advertising workforce, suggesting that even Apple can't resist the high margin temptation of selling advertising space on its most valuable properties.

The next big product innovation from Apple? Perhaps that would be the Apple Car.

Sources: Chartr, 9to5mac, Business Insider, and The Verge

Equity Market Weekly Returns (Others)

Previous Issues

Disclaimer

Mint Publications are for informational purposes only and does not constitute financial, investment, risk management, accounting, or tax advice. Nothing stated in this document is to be construed as a recommendation, solicitation, endorsement or offer to buy or to deal in any financial products.

Trading and investment in any financial products are exposed to risk. There are no such thing as risk-free returns. This material has been published for general education purposes only. It does not address specific investment or risk management objectives, financial situation, or needs of any person.

Advice should be sought from a financial advisor regarding the suitability of any investment or risk management product before investing or adopting any investment or hedging strategies. Past performance is not indicative of future performance.

Questions and/or feedback, please write to learnmore@mintfinance.xyz