Mint Macro Review Issue 6

Mint Macro Review Issue 6

#mmr | 11/Sep to 17/Sep

Mint Macro Review (#mmr) is Mint Finance’s weekly observations and commentary on global macro forces and key business updates.

Last week, we highlighted serious concerns expressed by Dr Ferguson, findings from Bridge Water’s research paper, and, record high puts (i.e. insurance) being bought by institutional investors.

Not unsurprisingly, markets witnessed sharp corrections following stubborn US inflation report and then fueled by fears of resolute central bankers, key market indices duly tanked.

For sometime now, capital markets have operated as if laws of gravity didn’t exist. Near “free” money, TINA effect (There Is No Alternative to stocks in the absence of yields elsewhere) made even distant returns look attractive. Not anymore. Regime change? Absolutely.

Gone are the days of “cash is trash”. With rates rising and inching towards middling single digit levels, leaving cash in bank is earning non-trivial yields and are also moving away from non-yielding assets such as gold. Hence, gold is now trading at a 2-year low. Typically, gold is seen as a hedge against inflation. In the long term, maybe; but clearly not in the short term.

As much as investors, political leaders and central bankers would wish for, this inflation is NOT transitory. Inflation is stubborn. It is here to stay and for considerable period of time.

As anyone who gets macro-economics can appreciate, monetary policy transmission takes time. Meanwhile, could central bankers who are acting in unprecedented synchronicity go overboard? Good chance that they could. Precisely, why market cycles occur.

Fears of recession is palpable. World Bank issued warning in a report on 15/Sep that key central banks moving in “graceful” tandem could send global economy into a devastating recession and hence urging caution.

Stubborn inflation could tempt central bankers into a HFL moment as Dr Mohamed El-Erian puts it. HFL? It is the possibility that central banks could push funding rates Higher, and get there Faster, and leave rates at elevated levels Longer.

Dr El-Erian writes in the FT that part of the stunning shift in market sentiments from hope to despair is driven by anticipated central bank response to sticky inflation. US Fed Governors have been unusually consistent in stating their unconditional commitment to fend off an unacceptably high inflation.

Given current high inflation, the US Fed is seemingly left with no choice but to front load its policy response including a 75bps rate hike for an unprecedented third consecutive time.

Sustained and rising levels of market volatility driven chiefly in part by central bank policy decisions compounded by bear market rallies amid fears of recession sets the ground for months of rough ride in markets ahead.

Source: @GitaGopinath on Twitter and Link to Dec 2021 NBER paper referenced in the Tweet above.

In this week’s #mmr

Read Mint Disclaimer

Last three issues - Issue 5, Issue 4, & Issue 3

EXECUTIVE SUMMARY

GLOBAL MACRO NEWS

1. US CPI coming higher than expected sends global equities into a tailspin (read more)

2. Dissecting US Consumer Price Inflation (CPI) numbers (read more)

3. A dozen Central Banks to announce rate decisions, with majority of them within a 24-hour window (read more)

4. US home mortgage rates rise fastest in 50 years (read more)

COMPANY NEWS AND UPDATES

5. Twitter shareholders to force Elon to complete the sale but hurdles remain (read more)

6. Citing deteriorating macroeconomic conditions, FedEx withdrew guidance and announced weak preliminary results (read more)

7. Adobe shares plummet >20% on news that it plans to acquire Figma for $20B paying 50x current ARR (read more)

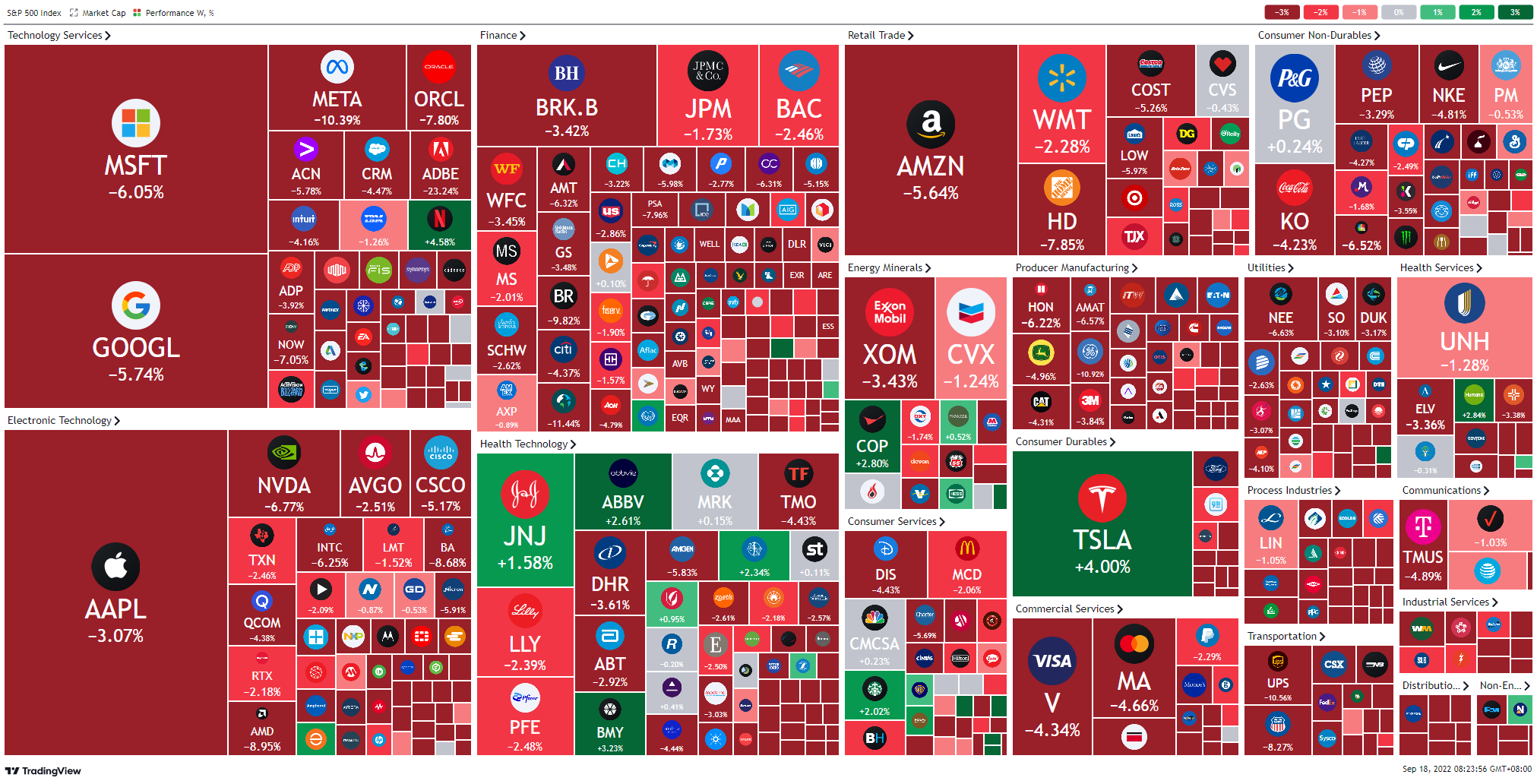

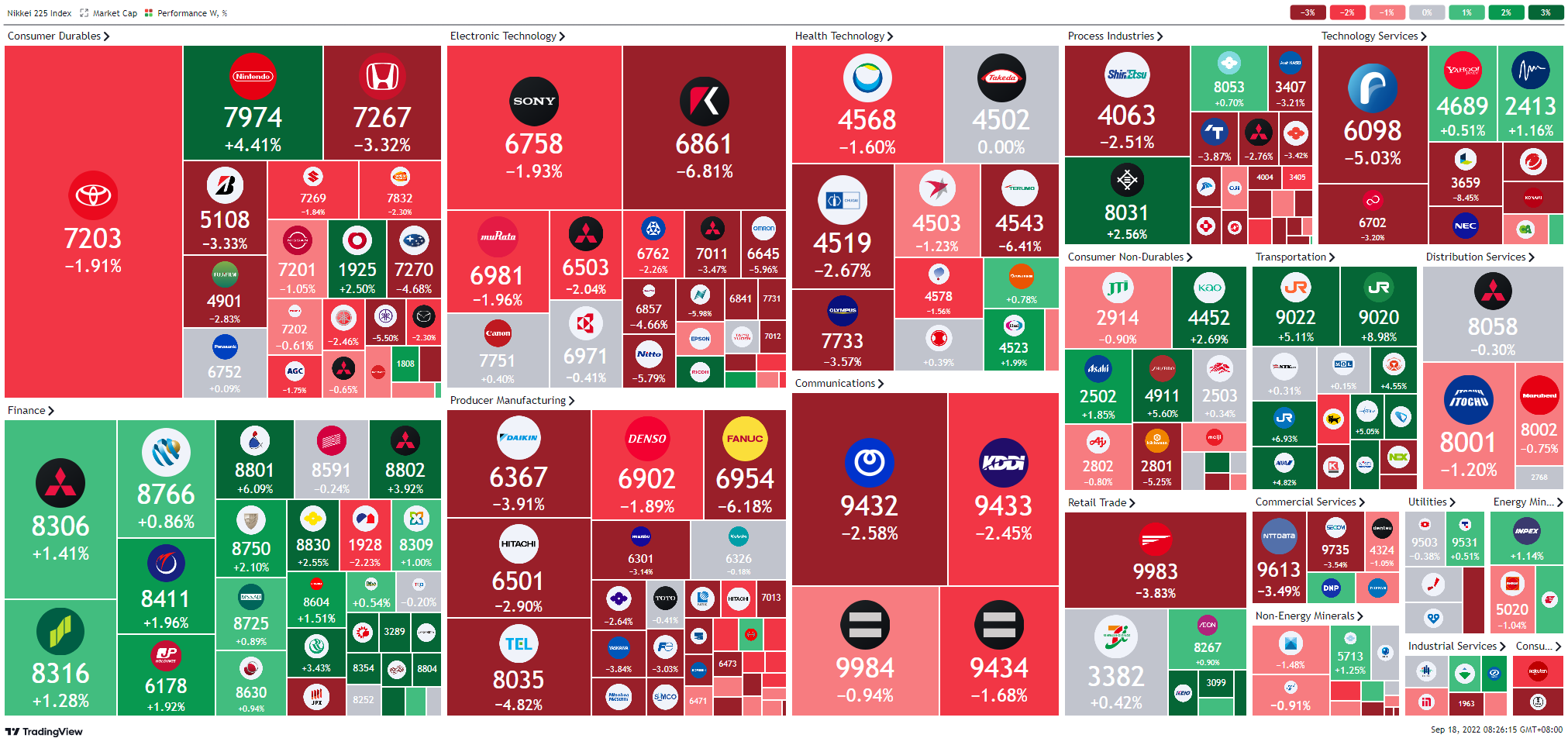

Equity Market Weekly Returns (S&P500, Nikkei225 & Nifty50)

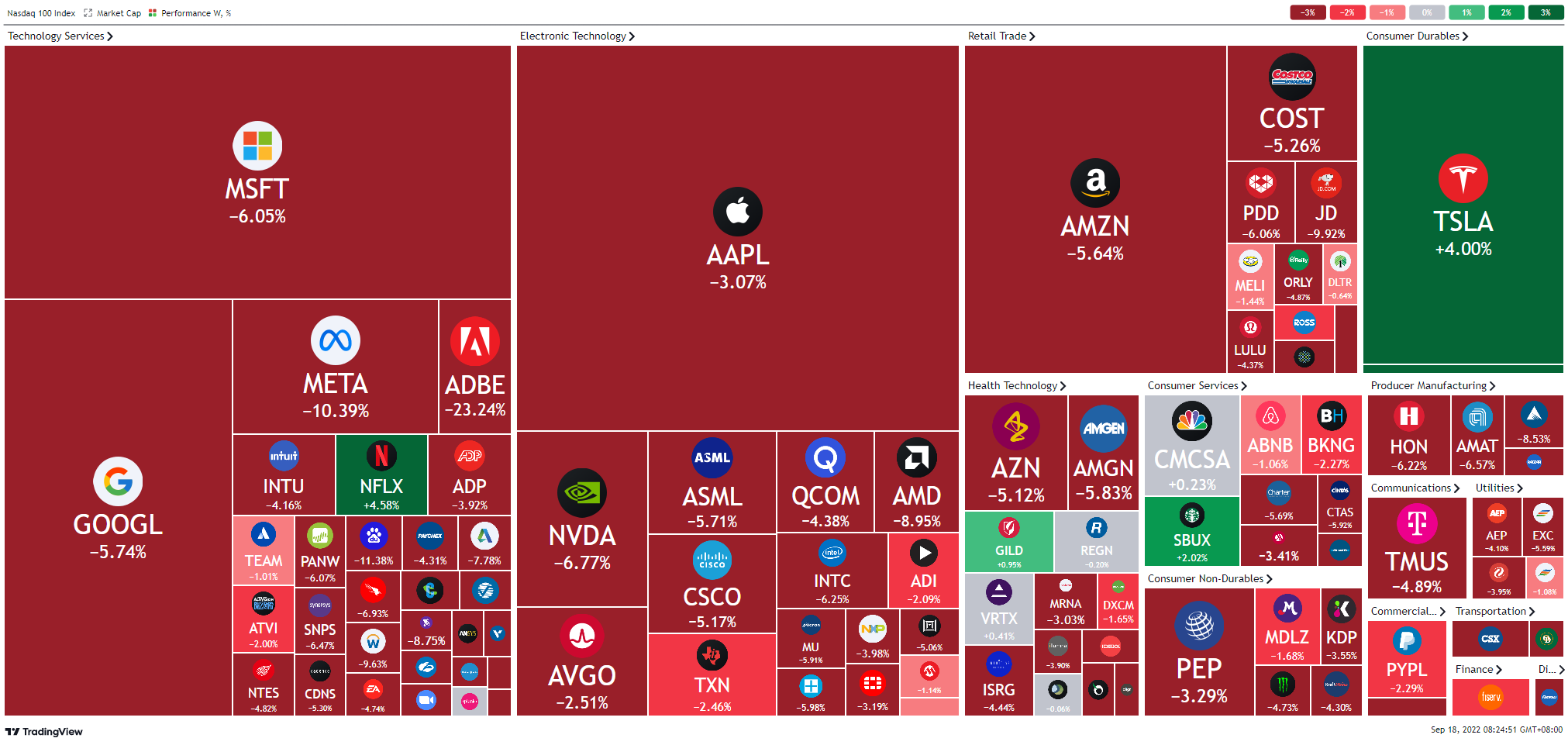

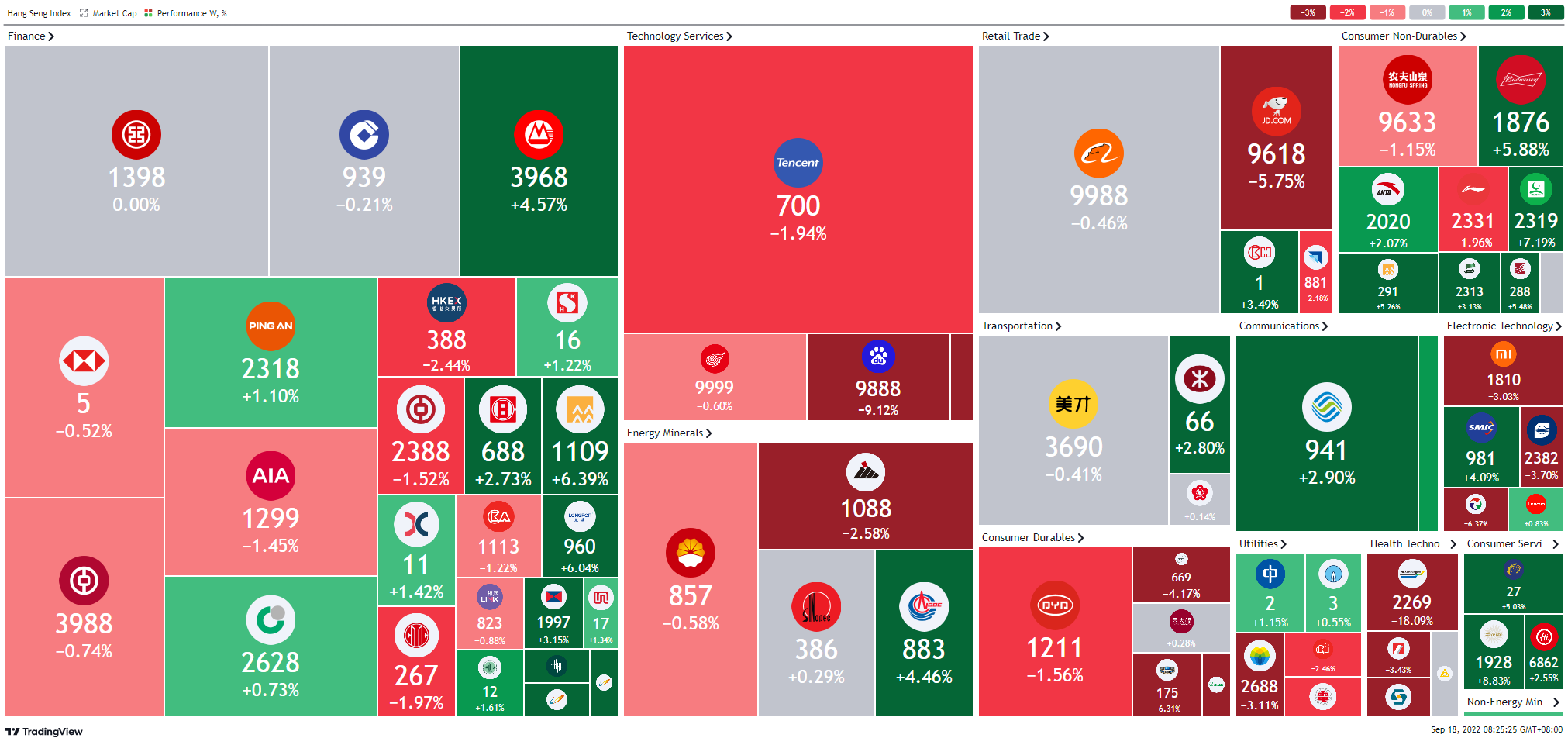

Click here to see heatmaps of equity markets in Nasdaq100, Hong Kong, Singapore, and Taiwan.

Macro News Highlights

Source: Mint Market Watch

GLOBAL MACRO NEWS

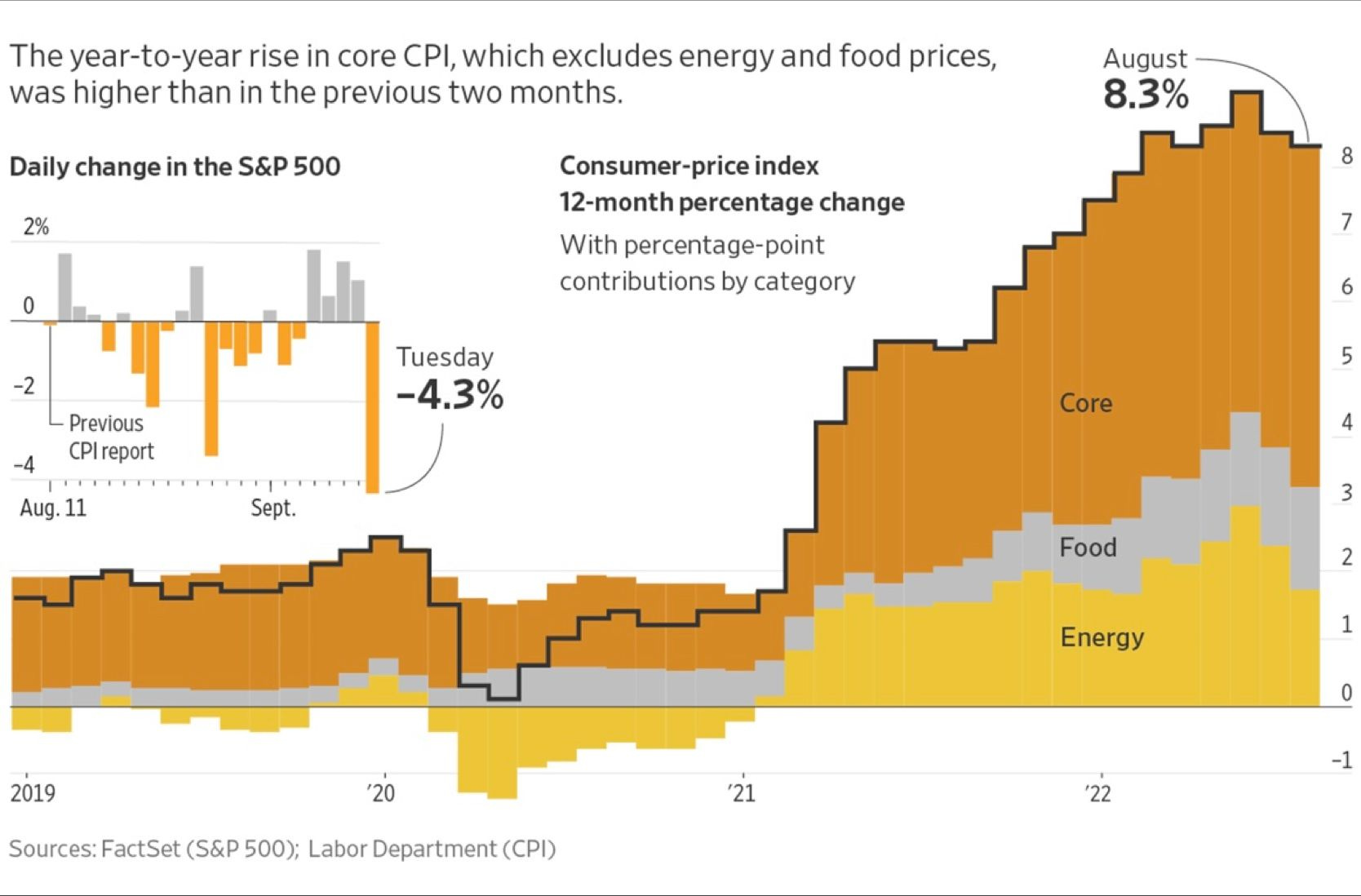

US CPI higher than expected sends global equities into a tail spin

Stocks fell sharply on 13/Sep (Tue) after inflation reports, after a key August inflation report came in hotter than expected, hurting investor optimism for cooling prices and a less aggressive Federal Reserve.

DJIA slid 1,276.37 points, or 3.94%, while S&P 500 dropped 4.32% to 3,932.69, and the Nasdaq sank 5.16% to end the day at 11,633.57.

Just five stocks in the S&P 500 finished in positive territory on 13/Sep after “hot” inflation report

Just five stocks in the S&P 500 finished in positive territory. Tech stocks were hit particularly hard, with Facebook-parent Meta skidding 9.4% and chip giant Nvidia shedding 9.5%.

YTD 2023, the S&P 500 Index has shed some 20%.

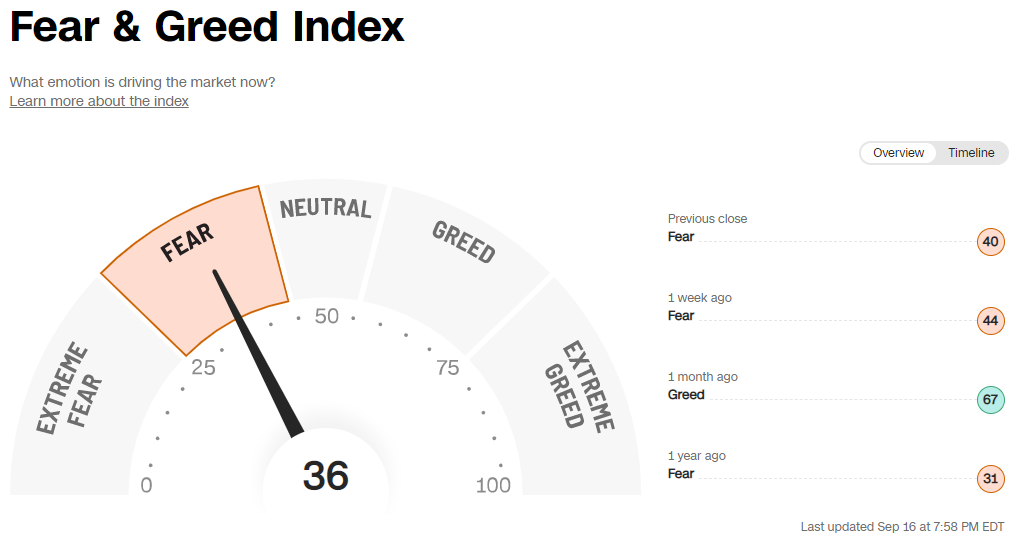

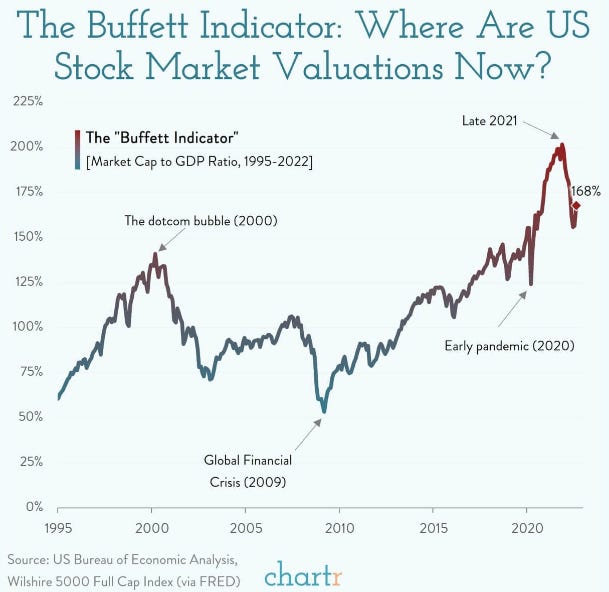

A stubborn inflation has made central bankers resolve harder than before to fend off inflation. Central bank's decision on rates will have outsized impact on equities. Notwithstanding, the corrections this year and the one's last week, where are we now?

With myriad ways to value stocks, Chartr presents the ratio of total market capitalisation to GDP. A simple metric that compares the total value of public equities with the actual economic output of the country as a whole.

170%; Buffet Indicator even after the recent falls, the ratio is >140% recorded during dotcom bubble

The indicator currently hovers around 170% which when placed in historical context is striking.

Even after the recent fall in markets the ratio is still one of the highest on record, north of the ~140% recorded during the dotcom bubble of 2000, and considerably elevated compared to the average since 1995 (109%).

Sources:

Dissecting US Consumer Price Inflation (CPI) numbers

US CPI increased 0.1% MoM in August (0.1% decline expected), up from a flat reading in July. CPI was up 8.3% YoY (8.1% expected). Core CPI, which excludes volatile items such as food & energy, increased 0.6% MoM (0.3% E). Core CPI increased 6.3% YoY.

Owners equivalent rent, a measure of the amount homeowners would pay to rent or would earn from renting their property, increased 0.7% (up 6.3% YoY).

Rent represents a significant share of the CPI reading and the slow-moving nature of rent prices means that housing could continue to boost inflation over the next few months.

Meanwhile, Food prices rose 0.8%, with the cost of food consumed at home increasing 0.7%. Food prices have increased 11.4% YoY.

New motor prices vehicles increased 0.8%, healthcare costs rose 0.7%, cost of prescription drugs increased 0.4%.

Source: CNBC, U.S. Bureau of Labor Statistics, Wall Street Journal

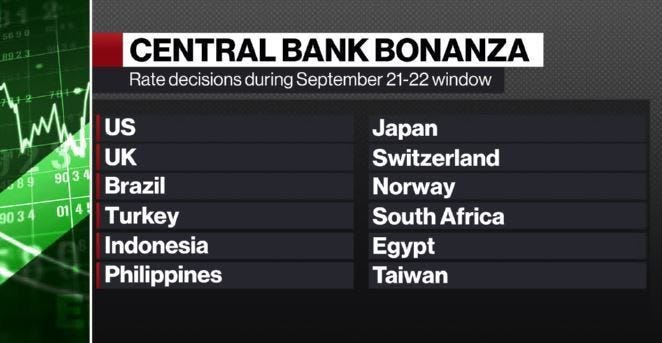

A dozen Central Banks to announce rate decisions, with majority of them within a 24-hour window

Over three days, Central Banks across the globe are expected to deliver interest-rate hikes adding up to more than 500 basis points combined. That aggregate number could be bigger is some of the officials opt for more aggression.

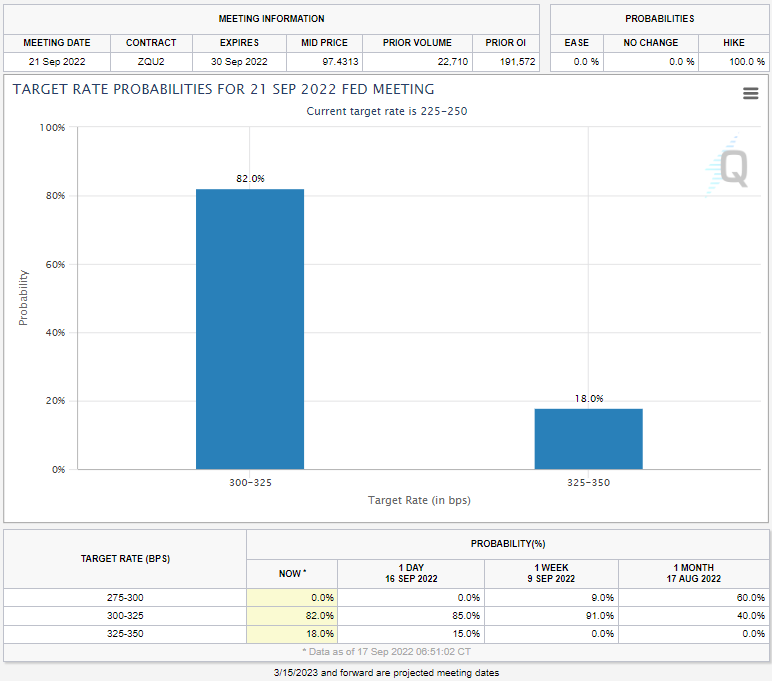

Soon after the release of inflation numbers, the probability of a 100bps hike in fed funds rate during the 21/Sep meeting inched up to 32% as of 14 Sep 22. As of 17/Sep market close, that probability has eased to 18%.

Sources: CME Fed Watch Tool

US home mortgage rates rise fastest in 50 years

Average 30-year fixed mortgage rose to 6.02% up from 5.89% a week ago and more than double from the same period last year. These rates are now at its highest in 14-years and has been rising at its fastest in 50 years.

US mortgage rates are rising at its fastest in 50 years and is now at its highest in 14 years

Rising Fed funds rate directly impacts mortgage rates. Low housing inventory, tight supply and keen demand from buyers continues to support a double digit growth in US home prices.

Central bankers will have keen eye to this as softening of home sales prices and consequent easing of rent of primary residence is critical to bringing inflation down.

Source: FT

COMPANY NEWS AND UPDATES

Twitter shareholders to force Elon to complete the sale but hurdles remain

Twitter shareholders have voted to ratify Elon Musk's $44 billion buyout offer, the company said in a statement.

Musk's April acquisition offer, which he rescinded in July, required stockholder approval before it could be finalized. During the seven-minute call, Twitter said the preliminary vote-count was enough to approve the deal, according to a report by Bloomberg News.

Shares of Twitter closed last week at $41.45 per share, lower than Musk's $54.20 offer.

Meanwhile, Elon Musk leaned heavily on whistleblower - Peiter "Mudge" Zatko - claims in his amended counterclaims against Twitter in his attempt to renege on a $44B deal to take Twitter private.

The public version of the counterclaim has been released, and from the outset it's advancing an altered argument for canceling the deal beyond Musk's claims that Twitter's "key metric" - monetizable daily active users - was misrepresented due to false and spam accounts.

"In what can only be described as one of the most significant whistleblower complaints in recent history," Zatko submitted his 84-page whistleblower report, outlining a series of explosive disclosures regarding misconduct within Twitter," Musk's team says.

Sources: MT Newswires, Seeking Alpha, and Bloomberg

Citing deteriorating macroeconomic conditions, FedEx withdrew guidance and announced weak preliminary results

FedEx - the US logistics company - seen as an economic bellwether given its significant role in global commerce - sent markets down even more on depressing forecasts.

FedEx announced its preliminary quarterly financial results ahead of its quarterly earnings next week. Its share prices got hammered 21% dropping from $204.87 on a share (15/Sep close) to end $161.02/share on 16/Sep close.

Citing deteriorating macro economic conditions and softness in global volumes, FedEx announced several cost cutting measures including closure of ninety (90) office locations, five (5) corporate office facilities, deferred hiring, reduced flights, and cancellation of projects.

FedEx reported EPS of 3.44 (5.17 expected) on revenue of 23.2B (23.62B expected). FedEx withdrew its full-year forecast citing a volatile environment that precluded prediction. The company reduced its forecast CapEx for the year by $500M to $6.3B.

For its fiscal second quarter the company expects adjusted EPS of at least $2.75 on revenue of between $23.5 billion to $24 billion. Wall Street analysts were looking for Q2 EPS of $5.48 and revenue of $24.86 billion. The company was scheduled to release results and hold a conference call with executives next week, but issued the report early.

Analysts (please see below) believe that FedEx state of business affairs has got more to do with the firm’s business structure, key strategic decisions, and tactical steps taken by the company.

The stock prices over the last 12 months when contrasted with its close competitor UPS vindicated that view as well. Over the last twelve months, UPS shares are down 8.4% compared to a whopping 37.7% drop in FedEx shares.

Thomas Black writes in Bloomberg opinion that the firm’s dire announcements most likely stem from the festering operational issues rather than sudden macro economic downturn.

In his analysis, among others, he opines that the firm has (a) a long history of getting its guidance wrong, before pandemic it set the guidance, raised it and then cut it twice, (b) lasting issues with 6,000 independent contractors at FedEx’s ground unit, (c) shrinking margin in a capital intensive Express unit business which is seemingly on a secular decline, and, (d) structural issues in operating dual network system which appears to be struggling in contrast to UPS’ unified network.

Source: Bloomberg, FT

Adobe shares plummet >20% on news that it plans to acquire Figma for $20B paying 50x current ARR

Shareholders of Adobe punished the firm by selling its shares down by >20% following the company's announcement to acquire Figma in a deal valuing the firm at $20B.

Figma in its last round of funding was valued at $10B and now for Adobe to pay twice as much has left its investors disappointed. Adobe plans to pay 50x Figma's current annual recurring revenue (ARR) in purchase consideration. It seems that Adobe is using 2021 price sentiments to acquire a tech company in 2022.

Figma is a design software firm offering online collaborative platform for designs and brainstorming and is used by firms from Zoom to AirBnB and Coinbase. Adobe intends to expand its portfolio of collaboration-focused platforms geared for the hybrid-work era.

For the quarter through Sep, Adobe's adjusted EPS rose YoY to $3.40 from $3.11 ($3.34 expected). Revenue grew 13% to $4.43B ($4.44B expected). Results were driven by strong net new annual recurring revenue in digital media and robust momentum in Adobe Express.

Analysts expect Figma acquisition to be dilutive to Adobe's adjusted EPS in the first two years, and to become accretive by the end of year three.

Source: MTNewswires, Reuters

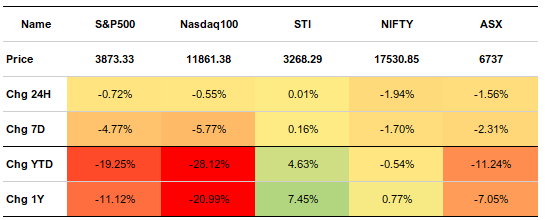

Equity Market Weekly Returns (Others)

Disclaimer

Mint Publications are for informational purposes only and does not constitute financial, investment, risk management, accounting, or tax advice. Nothing stated in this document is to be construed as a recommendation, solicitation, endorsement or offer to buy or to deal in any financial products.

Trading and investment in any financial products are exposed to risk. There are no such thing as risk-free returns. This material has been published for general education purposes only. It does not address specific investment or risk management objectives, financial situation, or needs of any person.

Advice should be sought from a financial advisor regarding the suitability of any investment or risk management product before investing or adopting any investment or hedging strategies. Past performance is not indicative of future performance.

Questions and/or feedback, please write to learnmore@mintfinance.xyz